Quiet summer for central bank buying

Central banks bought 28.4t of gold in August, 9% less than in July. Leaving aside January’s 11.2t net sale, this is the lowest level of monthly net purchases so far this year.

Central banks bought 28.4t of gold in August, 9% less than in July. Leaving aside January’s 11.2t net sale, this is the lowest level of monthly net purchases so far this year.

Following a higher level of monthly net purchases in March and April, our latest data published today shows that this trend continued into May.

We have written before about how, after a more inconsistent picture for central bank demand in the second half of 2020, our expectation was for continued net purchases in 2021 but at a more moderate pace than in previous record-setting years. So, how is that expectation holding up?

In February, central banks bought a net 36 tonnes (t) of gold, almost a third higher than January’s net purchases, but 52% lower y-o-y. This brings y-t-d net purchases to 64.5t, 44% lower than the 116.1t of net purchases over the first two months of 2019.

Wishful thinking. That’s how Angel Gurría, secretary general of the Organisation for Economic Co-operation and Development (OECD), responded to any prospect of a swift economic recovery from the coronavirus pandemic. But the scale of the impact on the global economy – as well as our daily lives – has been matched by the scale of the financial response.

At the end of January, the new head of the European Central Bank (ECB), Christine Lagarde, announced the launch of a year-long strategic review of the bank’s monetary policy strategy. Stemming from this, there has been much discussion recently about the ECB’s existing “below but close to 2%” inflation target, and whether this needs to be made more specific, both in aim and measurement.

In November, central banks reported adding 27.9 tonnes – on a net basis – to global official gold reserves, 43% lower than October’s increase. On a year-to-date basis, this brings cumulative net purchases to 570.2t, 11% higher the same period in 2018 (515.2t).

Twenty Years of the Central Bank Gold Agreement comes to an end today.

(short thread) https://t.co/qmscGo1wSa

Over the past 18 months, central banks have had a voracious appetite for gold. Alongside the impressive AUM growth in gold-backed ETFs, this has been one of the most prominent stories in the gold market. As we noted in the most recent edition of Gold Demand Trends, in H1 2019 central bank demand hit the highest level since becoming net buyers in 2010.

Intro: Central banks bought more gold in 2018 than at any time since the early 1970s – and the trend has continued this year. Isabelle Strauss-Kahn, Member of the Advisory Board of the World Gold Council, former Director of Market Operations at the Banque de France and former Lead Financial Officer at the World Bank, explains why.

Our Central Banks and Public Policy team have just published the results of the 2019 Central Bank Gold Reserves Survey. The survey gives a fascinating insight into the minds of central bankers and is especially timely since central banks continue to post record-breaking levs of net gold purchases in recent quarters.

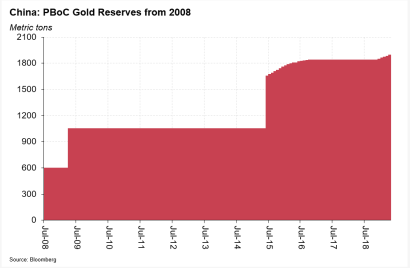

Gold: More on China's announcement that it bought #gold in April for the fifth successive month.

First, showing this data graphically. #Goldhub #blog https://t.co/ejBYDLFKn3

In March the amount of gold that left Shanghai Gold Exchange vaults - also known as the SGE loadouts - hit 218t. This is a chunky number. It is the highest March on record, almost 30% higher than the average monthly loadout since the start of 2016 and a 13% increase on March 2018.