I have written here before about how, after a more inconsistent picture for central bank demand in the second half of 2020, our expectation was for continued net purchases in 2021 but at a more moderate pace than in previous record-setting years. So, how is that expectation holding up?

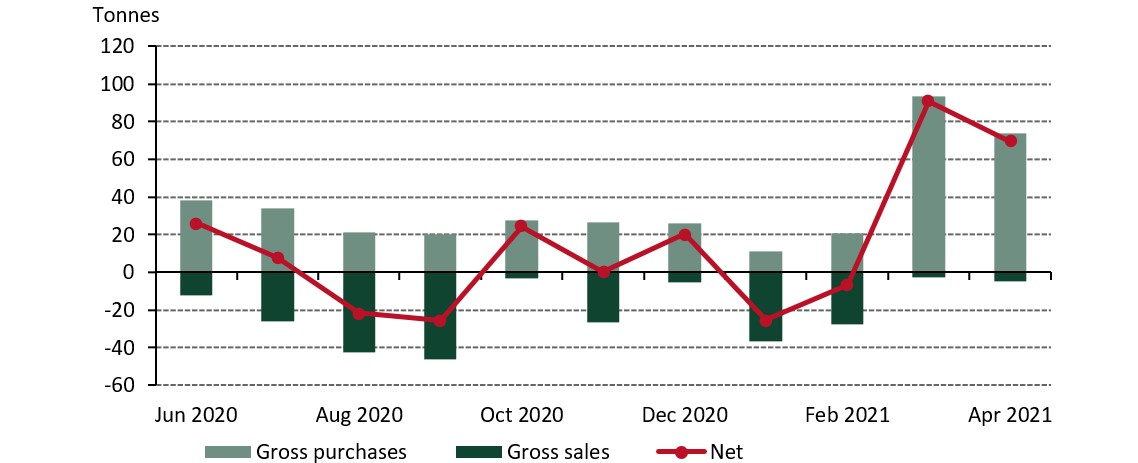

Initial estimates for April suggest that central banks added a net 69.4t to global gold official reserves.1 Year-to-date, we estimate that central banks have collectively bought between 150-200 tonnes of gold on a net basis.2

Chunky purchases have driven pick-up in central bank demand

Monthly gross purchases and sales by central banks

In April, gross purchases of 74.1t were almost entirely accounted for by five central banks. Thailand made the largest gold purchase during the month, adding 43.5t, which lifted gold reserves to 197.5t (4.5% of total reserves). Turkey also increased its gold holdings in April, after five consecutive months of declines. Gold reserves (excluding ROM holdings) rose by 13.4t, with gold reserves now standing at 526t. Uzbekistan (8.4t), Kazakhstan (4.6t), and Kyrgyz Republic (3.8t) were the other two familiar buyers.

The only sellers of note were Russia and Germany. Russian gold reserves declined by 3.1t in May, matching the drop we saw in January. Based on available information, it seems some of this sale may, again, be related to its coin-minting programme. German gold reserves fell by 1.3t, similarly in relation to coin minting.

So, back to our expectation. Estimated total net purchases of 150-200t for the first four months of the year confirm that there is still a healthy level of interest in gold. We should note, however, that the chunky purchases from Hungary (63t) and Thailand (44t) do account for a substantial share of this. This reinforces our expectation for continued healthy buying in 2021. While we cannot discount the possibility of more sales to come, we believe that the interest lies more on the buying side due to factors such as geopolitical risks, the economic impact of the pandemic, negative interest rates, as well as moves away from the US dollar.

More insights on this will be available when we publish our 2021 central bank survey. To see the latest central bank statistics in more detail, please click here.

Footnotes

Our data set is based on IMF data, but is supplemented with data from respective central banks where is it available and not reported through the IMF at the time of publication

This estimate excludes to 80t increase in Japanese gold reserves reported in March. Please see Gold Demand Trends Q1 2021 for more information.