Summary

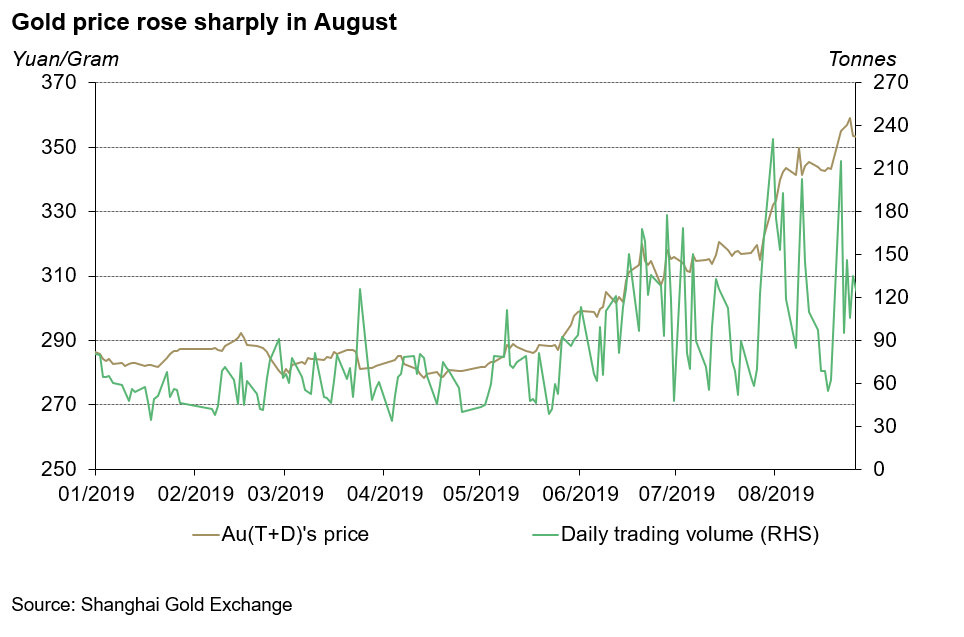

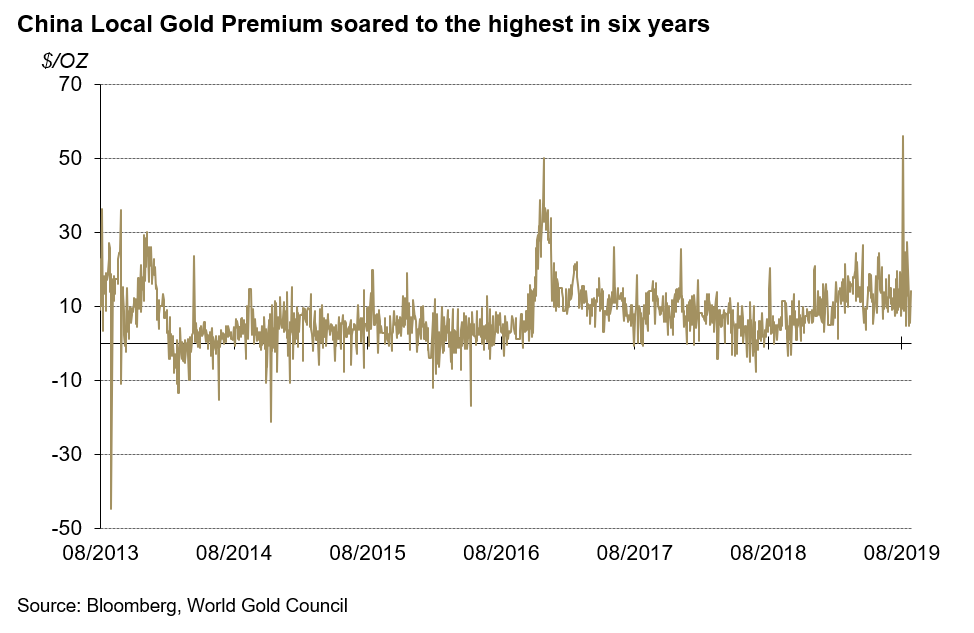

- In August, Shanghai Gold Benchmark (PM) rose 11% to 355 yuan/gram and the local gold premium peaked at a six-year high.

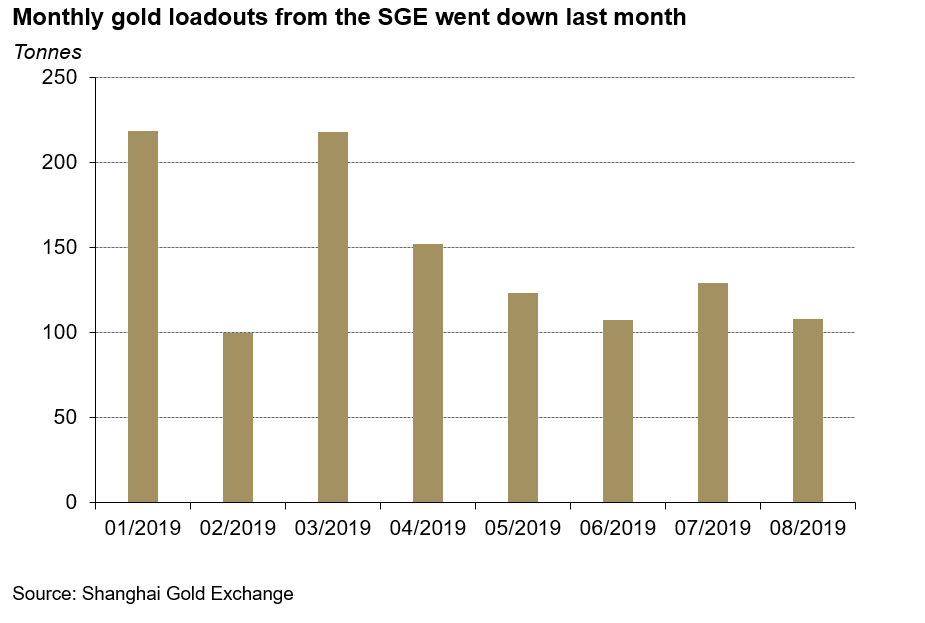

- While Au(T+D)’s trading volume in August surged to a new all-time high, gold withdrawals from the Shanghai Gold Exchange (SGE) declined again last month.

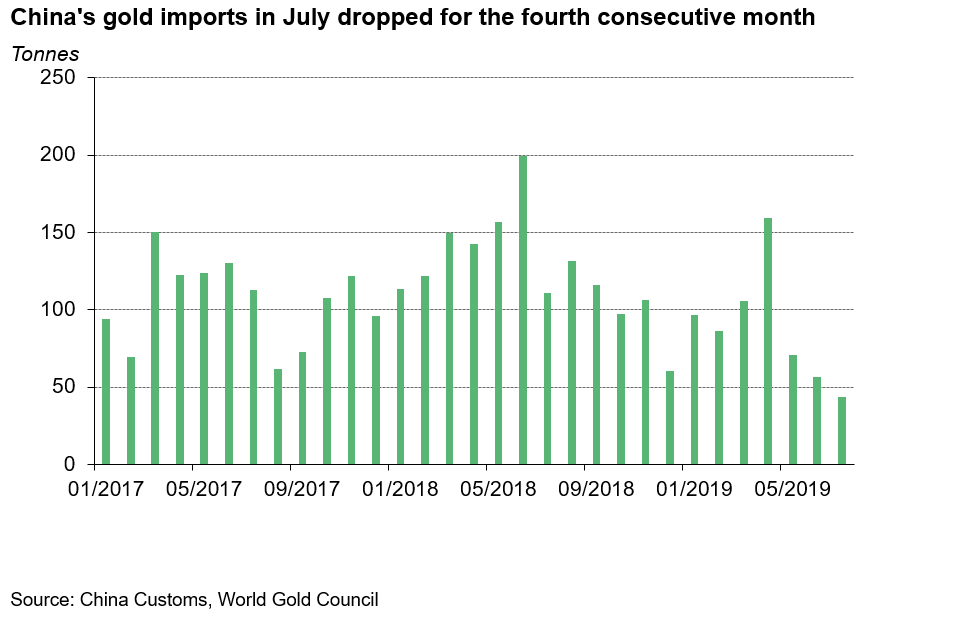

- Gold imports dropped to 44t in July, the lowest since 2017.

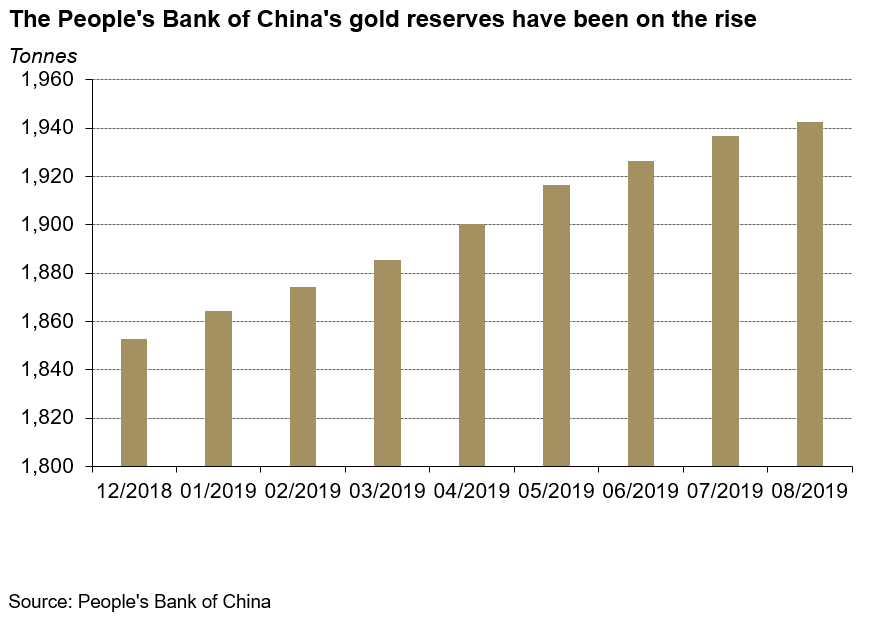

- The People’s Bank of China (PBoC) added another 6t to its gold reserves in August.

August was a good month for Chinese gold prices. The Shanghai Gold Benchmark price (PM) and Au(T+D) both ended August with a 11% increase in price while the LBMA Gold Price (AM) rose 7%. Globally, falling interest rates and uncertainties continued to drive international gold prices up. Locally, USD/CNY depreciation to above 7 – an important psychological threshold – boosted yuan-denominated gold prices.

The weak CNY was the result of the decelerating Chinese economy and the escalating China-US trade dispute. Slower growth in key Chinese economic indicators such as social retail sales, official manufacturing PMI and industrial-added value were witnessed again while inflation remained at an 18-month high of 2.8% in August. The PBoC announced a cut in banks’ required reserve ratio early September, aiming to prevent further slowdown in economic growth.

And the volatile trade relationship between China and US exerted more pressure on CNY in August. Affected by both internal and external factors, USD/CNY finally breached CNY7 on 26th August for the first time in 11 years.

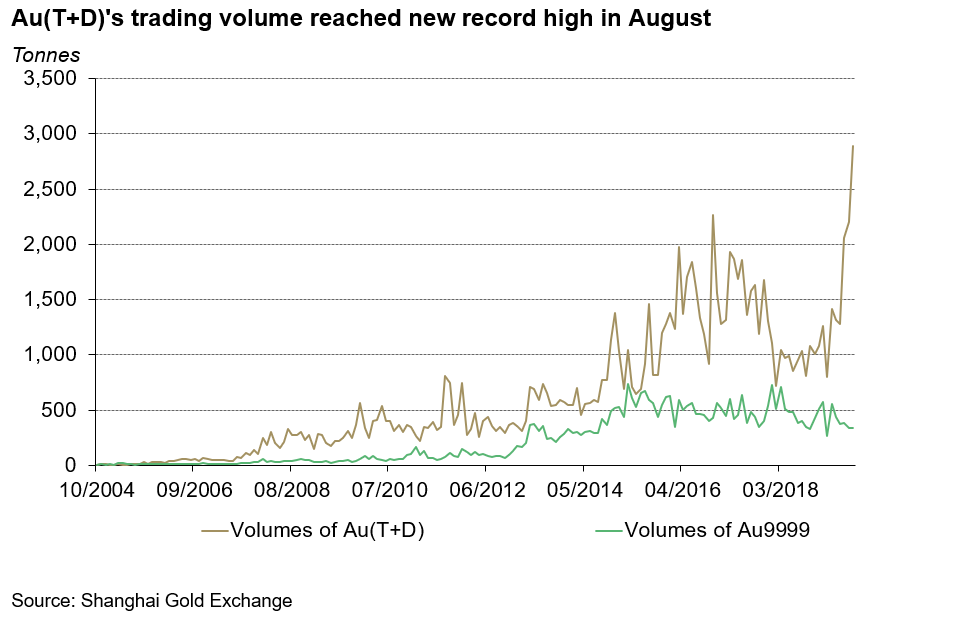

Au(T+D)’s trading volume reached 2,894t in August, a new record high. As the gold price rally continued, speculators’ enthusiasm pushed the contract’s trading volume up. And its trading volume has been above 2,000t for three consecutive months.

In contrast, the physical contract was less popular as Au9999’s trading volume leveled off to 337t in August, barely moving from the five-month low made in July.1 As our most recent Gold Demand Trends explained, China’s physical demand was soft partly due to the rapid increase in gold price.

The average local gold premium went up by over 31% m-o-m in August. The depreciating currency and declining gold imports led to a jump in the local gold premium, reaching a six-year high of US $55/oz on 26th August.

Another key driver could be the tightening gold supply in China due to declining gold imports. According to China Customs’ data, China imported 619t during the first seven months in 2019, 40% lower than the same period last year.2

China’s gold imports under the HS code 7108 saw another decline in July.3 Only 44t of gold was imported to China in July, 67t lower y-o-y and 13t lower m-o-m. This is the fourth consecutive drop this year and the lowest since 2017.

China-US trade dispute and the economic slowdown might have led to authorities to tighten import quotas, which we have seen during most of 2019, in order to prevent capital outflows. Weaker consumer demand - as reported in our most recent Gold Demand Trends - could also be a reason for the falling gold imports.

Gold withdrawals from the SGE fell to 108t in August, 22t down from July. While speculative demand for gold remained elevated, physical demand stayed weak. Talks with industry indicate that physical gold demand might have suffered from the high gold price in China last month, with consumers preferring to wait on the side-lines to see if the rally continues or corrects.

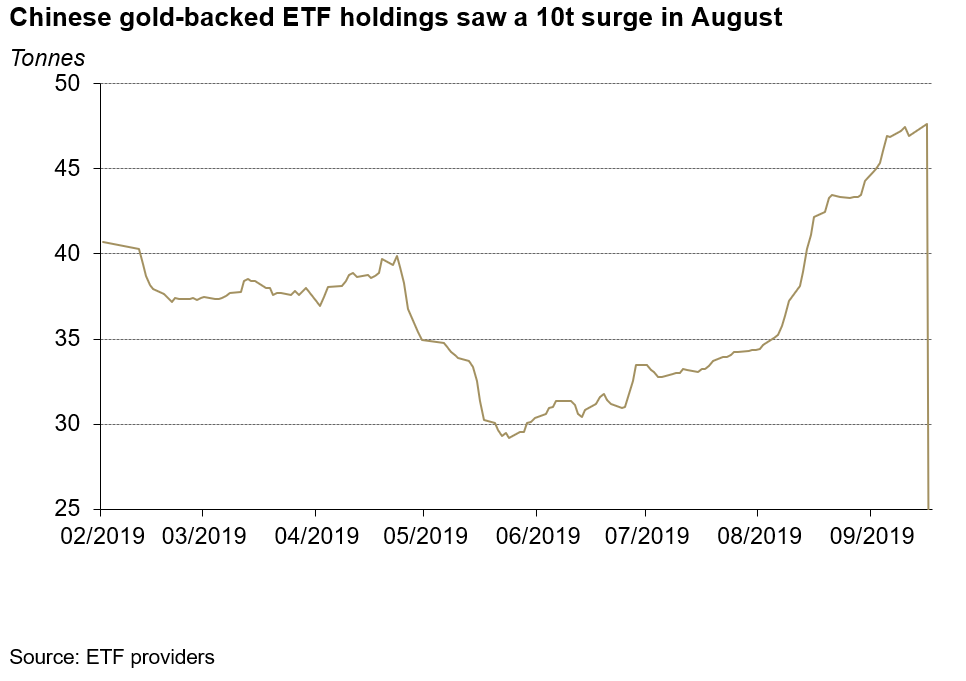

Chinese gold ETFs holdings witnessed significant growth in August, continuing the rising trend from mid-May. As of 30th August, holdings of the four major Chinese gold-backed ETFs’ totalled 44t, a 10t increase from July. To hedge against the weakened currency and uncertainties from the trade dispute, Chinese investors continued to add gold ETFs to their portfolios. The rising gold price was also a contributor attracting new investors as well as innovations.

The PBoC added another 6t to its gold reserves in August. After the nine-month gold purchasing streak, the PBoC’s gold reserve now stands at 1,942t as of August.

As discussed in our most recent blog on central banks’ gold purchasing activities, sluggish economic growth and uncertainties have led to over 400t of global central bank gold net purchases as of July. And this is the fastest pace of accumulation since central banks became net purchasers since 2010 on an annual basis.

Outlook

Gold prices have fallen back slightly in September following positive signs around the China-US trade dispute, helping to alleviate investors’ concerns. However, lower interest rates and rising inflation in China might support gold investment demand in the coming months.

And the momentum – the increasingly popular speculative demand and the expanding AUM in gold ETFs – could still remain. As the gold price dips, it might be the ideal bargain in the eyes of Chinese investors.

Moreover, recent talks with the industry suggest that after a seasonally quiet Q2 for jewellery demand, jewellers have put in more efforts into product innovations and marketing. And the price dip might just be what the jewellers needed to improve their sales.

Footnotes

1 For the differences in the demand the two contracts represent, please visit: https://www.gold.org/goldhub/gold-focus/2019/06/tale-two-contracts-speculative-investment-physical-demand-down

2 Gold imports data published by China Customs has a one-month lag, i.e. July’s figure was only available towards the end of August.

3 HS code 7108 includes gold (Including Gold Plated with Platinum), unwrought or In semi-manufactured forms, or In powder form