02 - Why digital gold matters now and what’s holding the market back

2.1 Opportunities for the digital gold market

Last year (2025) was a breakout year for gold ETFs and other digital gold products. After three years of gold ETF net selling, meaning more ETF shares were sold than bought, causing the underlying gold holdings to shrink, and a largely flat 2024, gold ETFs turned sharply positive in 2025 (Exhibit D). They contributed 16% of annual gold demand and drew US$89 billion of inflows, lifting total assets under management to US$559 billion and holdings to 4,025 tonnes.1 The jump was mainly driven by the wider macroeconomic environment, including (i) safe haven demand amid trade disputes, (ii) geopolitical tensions and market volatility; momentum as the gold price rose; and (iii) lower opportunity costs as US yields fell and the dollar weakened.

16% of annual gold demand attributed to gold ETFs in 2025

Importantly, demand for digital gold has not been limited to gold ETFs. Gold tokens have also grown sharply, with their market cap topping US$4 billion in 2025.2 And digital gold accounts are becoming a real retail habit in some markets. For example, BullionVault, one of the leading marketplaces for digital gold accounts, holds around 43 tonnes of gold for its customers.3 Tokenised gold and digital gold accounts are emerging as credible adjacencies: they are gaining traction and have clear adoption potential, driven by frictionless access and the prospect of everyday utility.

Retail investors are becoming more digital each year, especially younger investors who are entering the market earlier and predominantly through digital platforms. These younger users often use mobile investment apps that are easy to access and require only small initial contributions to get started.

US$4 bn Tokenised gold market cap in 2025

Across 13 economies, WEF finds 30% of Gen Z start investing in early adulthood, versus 9% of Gen X and 6% of Baby Boomers. Notably, 86% of Gen Z have learned about personal investing by the time they enter the workforce.4 Beyond simple digital access, trust and clarity are important in capturing retail investors. In the UK, the FCA finds 66% of 18–40 year old investors decide on an investment in under 24 hours and 14% decide in under an hour.5

86% of Gen Z have learnt about investing before they enter the workforce

Digital formats can overcome gold’s traditional barriers of larger minimums, offline buying, exchange fees, and storage. Issuers of digital gold products can do this by:

- Making it easy to start and keep investing (e.g., small minimums, recurring buys, simple portfolio placement).

- Offering the right format for different needs (e.g., ETF-like exposure, vaulted accounts, tokenised products).

- Building confidence with clear pricing, clear custody and audit information, and simple rules for selling or taking delivery.

With the right digital products, issuers can capture investors during risk events and broaden gold's role in everyday portfolios, particularly for younger investors.

66% of 18–40 year old investors decide on an investment in under 24 hours

2.2 Challenges for the digital gold market

Despite growing interest and a widening range of formats, the market for digital gold remains small relative to the overall physical gold market. This reflects a combination of challenges in product development and market.

The proof-of-backing challenge

“For the tokenisation of precious metals, the hurdles come in bridging the physical world and the digital world together in terms of processes. It is not enough to just claim that a digital asset is backed, you must prove the backing, and this involves using streamlined processes to ensure the underlying physical asset is always safely secured.”

Zac McKenna, Head of Digital Assets, Brinks6

Challenges in product development

Today’s gold market is mostly organised around the handling, storage, and movement of physical gold. This creates four recurring challenges for issuers seeking to launch and operate digital gold products:

- Fragmented vendor landscape and lengthy setup

Launching a digital gold product typically requires coordination of a large number of specialist providers across physical gold operations, technology, compliance, and distribution. As illustrated in the deep dive below, even a basic digital gold product requires engagement with dozens of specialist providers. Licensing and regulatory engagement, often across multiple jurisdictions, further extend timelines. The result is long setup periods and high coordination risk, with no single party accountable for end-to-end integrity.

- Ongoing operational complexity

The operational burden continues well beyond the launch and scale of a product. Issuers must continuously reconcile digital and physical gold balances, monitor KYC and AML, maintain liquidity and redemption arrangements, and commission regular audits, all requiring dedicated systems and oversight that cannot be meaningfully reduced once live. Core obligations around custody, compliance, and assurance remain largely fixed and are material, slowing decision-making and limiting the ability to invest in product improvement or expansion.

- Challenging economics

Upfront development costs for digital gold products can reach tens of millions of dollars before generating any revenue, making entry prohibitive for new players and unattractive even for established entities. Operating costs remain high, resulting in fragile unit economics that only improve at very large scale. This limits pricing flexibility, constrains reinvestment, and increases vulnerability during periods of low volumes or market stress.

- Legal fragmentation across jurisdictions

Issuers must navigate a complex and evolving regulatory landscape, often without clear precedents for digital gold structures. Questions around asset classification, custody models, redemption rights, insolvency protection, and cross-border distribution require bespoke legal analysis and regulatory classification in each jurisdiction. The lack of unified legal frameworks once again increases time to market, legal costs, and regulatory risk.

Challenges in market adoption

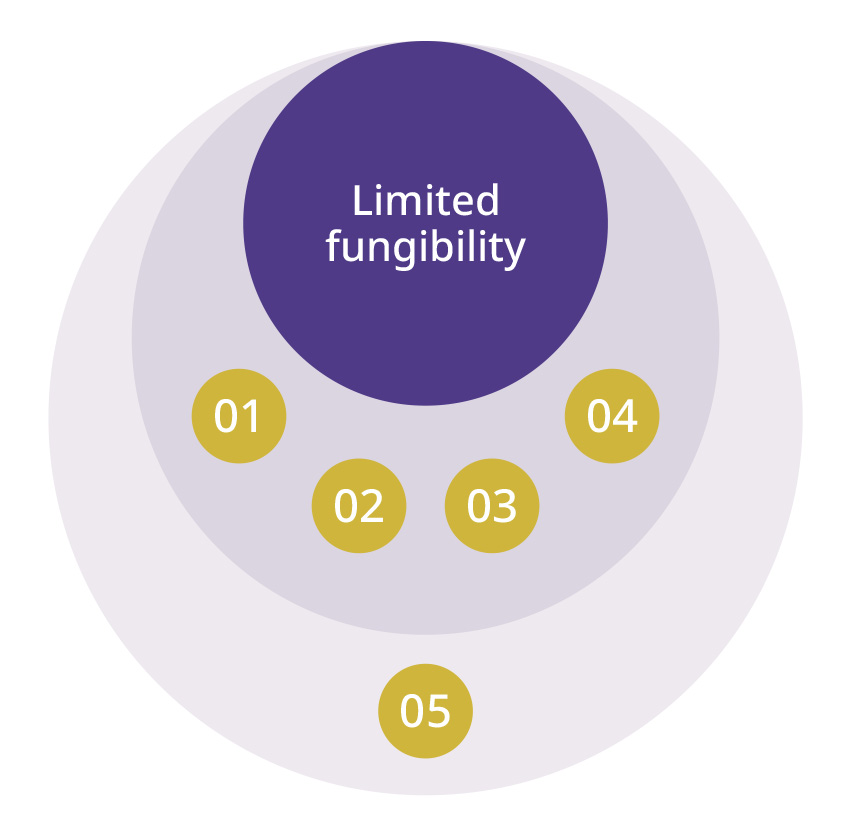

Even where digital gold products are successfully launched, five product‑level limitations constrain adoption and scale. These limitations are a result of a lack of fungibility, driven by structural shortcomings in how today’s digital gold products can be designed, governed, and integrated into digital financial markets, resulting in a lack of market interest.

00. Limited fungibility

Digital gold products operate in closed ecosystems, with limited interoperability across platforms, wallets, and venues. This stands in contrast to physical gold, which benefits from a long‑standing principle of reasonable fungibility: that gold is gold, regardless of owner, venue, or form. In the digital realm, this principle breaks down. Products referencing the same underlying asset can differ meaningfully in custody models, governance, audit standards, and legal rights, making them hard to compare and difficult to aggregate into deep, shared liquidity pools.

01. Limited utility

Most digital gold today is held passively, primarily as a hedge against inflation. At the same time, the breadth of digital financial asset use cases has shifted markedly in recent years, driven by the rise of decentralised finance (DeFi). DeFi protocols collectively hold over US$125 billion in total value locked (TVL), a broad measure of assets actively used for collateralised lending, liquidity provision, payments, and related financial activity. Outside of a small number of crypto-native use cases, digital gold has not been integrated into these systems.

02. Varying cost

The cost of accessing digital gold can vary and be opaque across formats and distribution channels. Retail customers can face several charges, including spreads, platform margins, expense ratios, and brokerage fees. For example, tokenised gold can carry some of the highest all-in costs once spreads, exchange/on‑off‑ramp fees, and blockchain network fees are included, especially for small transactions.

03. Limited trust

Retail users face varying standards of proof of backing, audit frequency, insurance coverage, and governance across issuers. Between different products and issuers, it can be difficult to know how and where gold is held, who controls the bars, and what happens in insolvency scenarios. This lack of clarity can undermine confidence, especially for investors seeking gold as a safe and credible asset.

04. Inconsistent redemption

Redemption terms vary widely by product, including minimum sizes, locations, timelines, and costs. Physical redemption is often restricted, weakening trust and reducing the perceived benefit of digital gold.

05. Limited awareness

Awareness remains low across digital gold products. World Gold Council research shows that the key leading reason retail investors have not invested in gold tokens is lack of awareness (38% in the US; 34% in the UK), indicating that adoption is constrained as much by visibility and understanding as by product design.7