04 - A proposition for the industry

4.1 What is Gold as a Service?

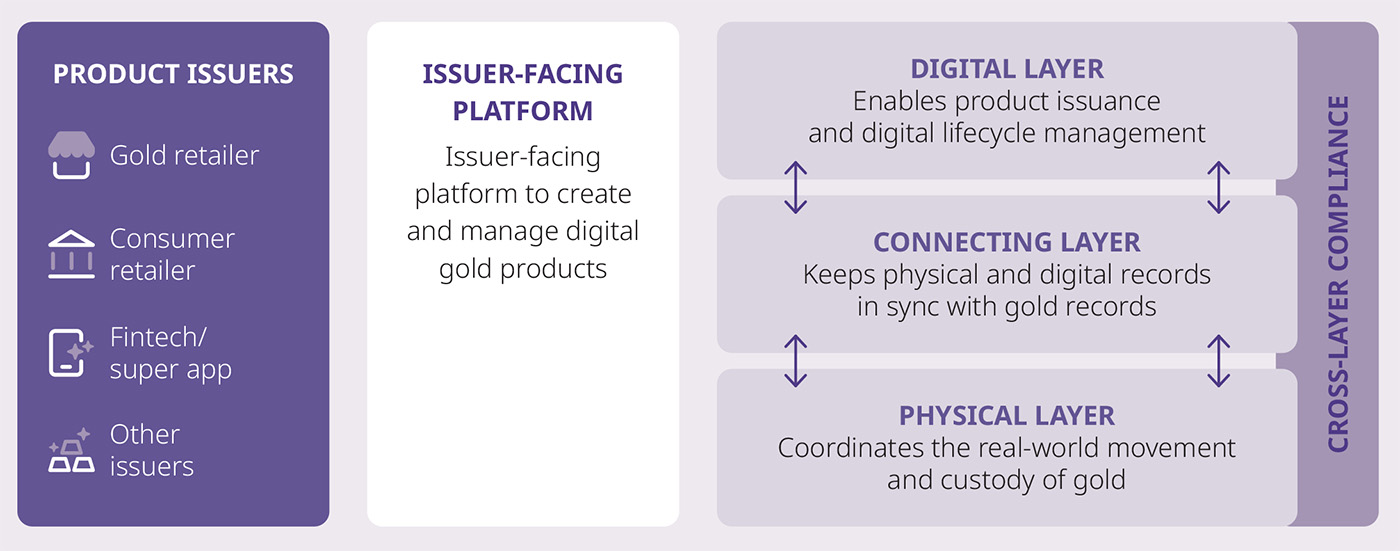

Gold as a Service is proposed as a shared infrastructure platform that would allow issuers to build and operate digital gold products without independently assembling the entire physical and digital stack.

The issuer would remain responsible for the customer proposition (commercial terms, distribution, brand, and customer experience). Gold as a Service would provide the underlying infrastructure to connect the physical gold ecosystem (sourcing, custody, vaulting, inventory management, assurance, liquidity, and redemption pathways) with the digital product layer (issuance, transfers, and lifecycle management). To deliver this reliably, the platform would be structured around three integrated layers (Exhibit F):

A simple way to think about Gold as a Service

The issuer (e.g., a bank or fintech) remains the product owner, meaning it designs the customer proposition, sets pricing, controls branding, and manages distribution. Gold as a Service operates the underlying plumbing: the custody and movement of gold, the issuance and lifecycle management of the digital representation, the reconciliation between physical and digital records, and the embedded compliance and controls.

Physical layer

This layer would coordinate the physical movement and custody of gold, working with approved vaulting, liquidity, logistics, insurance, and audit partners. It would be responsible for the operational reality that underpins trust: how gold is sourced, transported, where it sits, how it is safeguarded, and what happens when gold needs to be allocated, moved, or redeemed.

Digital layer

This layer would enable the issuance and management of digital gold products such as gold tokens, digital gold accounts, or similar products (as discussed in "The emergence of digital gold"). It would also provide the operational tools required for the product to run at scale, including monitoring, reporting, and routine day-to-day management.

Connecting layer

This layer would keep the physical and digital records synchronised. It would link the digital gold lifecycle (issuance, transfers, redemption) to gold records defined by the issuer’s product structure, providing a consistent basis for reconciliation, control, and assurance. Issuers would create and manage their products on an issuer-facing platform, which would act as the user interface that ties these layers together.

Physical layer partners and market foundations

The physical layer would be delivered in partnership with bullion banks, vaulting providers, logistics firms, insurers, and auditors, which would ensure the integrity, custody, liquidity, and redeemability of gold. Bullion banks and wholesale liquidity providers would anchor physical supply and support settlement, while vaulting and logistics partners secure storage and global delivery. This layer would provide the operations that underpin trust in all digital gold products.

Product issuance and management partners

The digital layer would be delivered with partners that provide the capabilities to issue and operate digital gold products at scale. This would include tokenisation and digital asset infrastructure providers, wallet and custody technology firms, and compliance and monitoring providers. These partners would support issuance, transfers, and lifecycle management, allowing issuers to focus on product design, distribution, and customer relationships rather than maintaining bespoke digital infrastructure.

At scale, Gold as a Service requires more than technology.

It is built on an ecosystem of partners across the physical and digital layers of the gold market who support trusted and liquid digital gold.

4.2 Who can benefit from Gold as a Service and how?

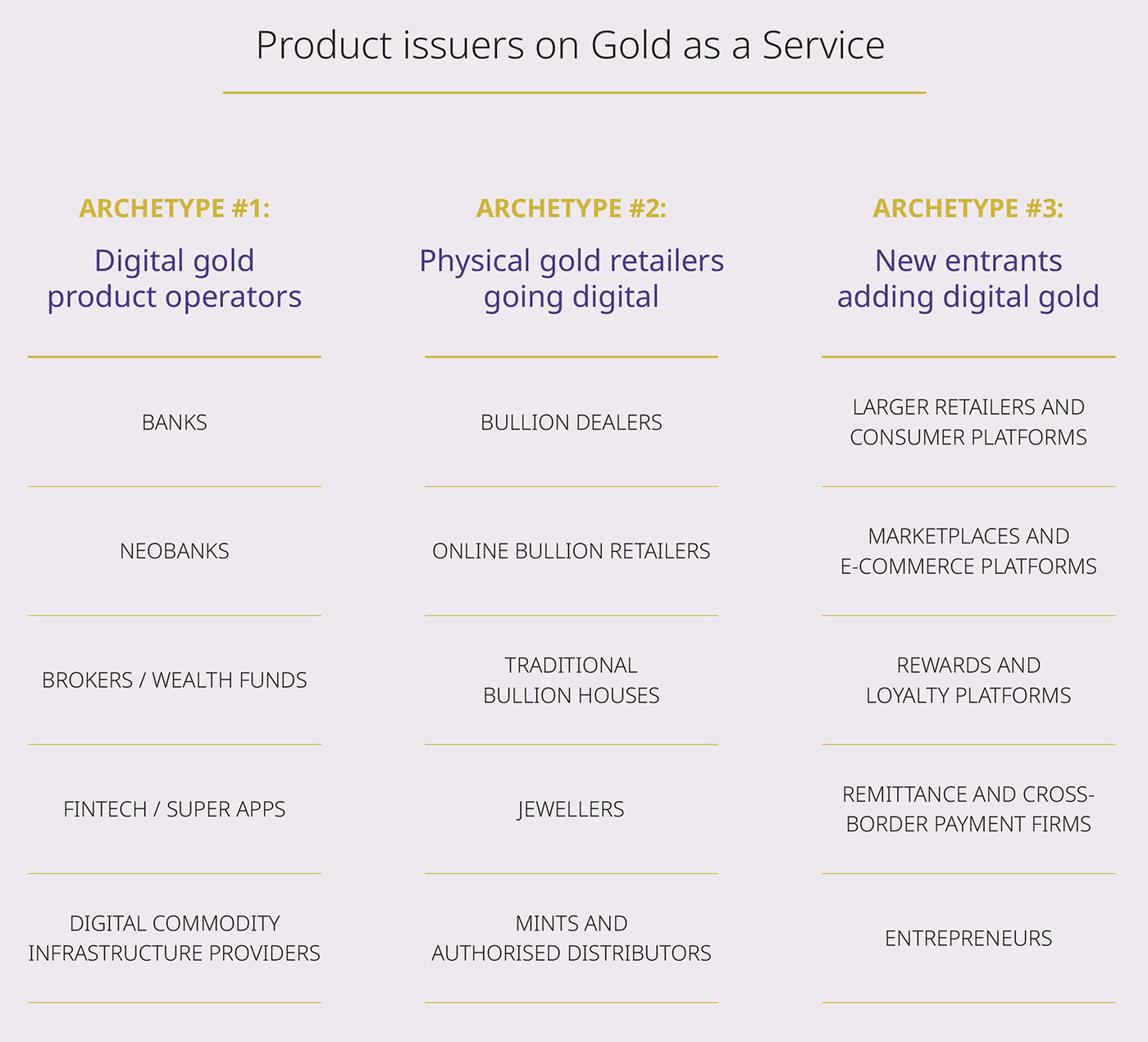

Gold as a Service could benefit any issuer that wants to offer digital gold products without building complex digital infrastructure themselves or coordinating multiple vendors across sourcing, custody or vaulting, insurance, audits or assurance, liquidity, logistics, and redemption (Exhibit G).

In practice, this would serve three broad issuer archetypes:

ARCHETYPE #1

Digital gold product operators

Issuers that already run a live digital gold product with active customers, meaningful volumes, and day-to-day operations. Examples of digital gold product operators:

- BANKS

- NEOBANKS

- BROKERS / WEALTH FUNDS

- FINTECH / SUPER APPS

- DIGITAL COMMODITY INFRASTRUCTURE PROVIDERS

|

Needs

|

Challenges

|

|

These issuers need to run digital gold reliably at scale with competitive pricing. They need to align physical inventory and digital units, support cash-out and redemption, and expand to new markets or channels without increasing operational complexity.

|

Most work with multiple providers for custody or vaulting, liquidity, insurance, audits or assurance, and logistics or redemption. This creates ongoing friction including reconciliation breaks, exception handling, reporting overhead, and repeated requests to prove their products are fully backed. Expansion often means adding more vendors and more points of failure.

|

How Gold as a Service would help

- Decrease vendor dependencies by creating a single, integrated operating layer across custody, liquidity, assurance, logistics, and redemption.

- Standardise and scale operations with consistent workflows for allocation, movement, redemption, and partner handoffs.

- Improve redemption pathways by defining clear rules on minimums, platform fees, timelines, and supported pickup and delivery pathways.

- Limit slippage and spread by pooling liquidity and limit price dispersion across apps arising from existing infrastructure inefficiencies.

- Strengthen trust signals by standard audits and attestations, shared bar lists, control frameworks, and access to common insurance coverage.

- Increase utility by allowing customers to move gold holdings between front ends without forced sell-and rebuy, reducing double spreads and timing risk.

ARCHETYPE #2

Physical gold retailers going digital

Established physical gold sellers that want to add a digital offering alongside their physical business. Examples of physical gold retailers going digital:

- BULLION DEALERS

- ONLINE BULLION RETAILERS

- TRADITIONAL BULLION HOUSES

- JEWELLERS

- MINTS AND AUTHORISED DISTRIBUTORS

|

Needs

|

Challenges

|

|

These retailers want to expand into digital gold by offering products such as digital gold accounts, certificates, gifting etc. to extend their physical gold business into digital offerings, allowing them to generate additional revenue streams and reach a broader audience.

|

They are strong in sourcing and fulfillment, but digital gold requires new capabilities: digital issuance and lifecycle management, customer balances, continuous reconciliation, monitoring, assurance reporting, and scalable customer support. Working with vendors to implement these capabilities can be slow and expensive, and can create brittle operations.

|

How Gold as a Service would help

- Accelerate time to market by launching digital gold without building the full tech and operating stack from scratch.

- Standardise and scale operations using consistent workflows for allocation, movement, redemption, and partner handoffs.

- Improve redemption pathways by defining clear rules on minimums, platform fees, timelines, and supported pickup and delivery pathways.

- Lower integration and build costs by minimising bespoke builds and one‑off operational requests as channels scale.

- Strengthen trust signals by standard audits and attestations, shared bar lists, control frameworks, and access to common insurance coverage.

- Facilitate digital distribution by providing a tech stack that is easily integrated with digital channels, wallets, and marketplaces.

ARCHETYPE #3

New entrants adding digital gold

Potential issuers that do not currently sell gold but are eager to build a gold proposition and/or grow the share of wallet of existing customers. Examples of new entrants adding digital gold:

- LARGER RETAILERS AND CONSUMER PLATFORMS

- MARKETPLACES AND E-COMMERCE PLATFORMS

- REWARDS AND LOYALTY PLATFORMS

- REMITTANCE AND CROSS-BORDER PAYMENT FIRMS

- ENTREPRENEURS

|

Needs

|

Challenges

|

|

These issuers need to introduce gold as a feature or product line, such as micro-savings, gifting, rewards, remittance-linked savings, or holding gold as a balance-sheet asset, without becoming gold infrastructure experts.

|

Gold requires operational plumbing that most new entrants do not have, including in custody or vaulting, insurance, assurance, liquidity, logistics, and redemption, increasing lead times, compliance efforts, operating burdens, and inconsistency across markets and customer journeys.

|

How Gold as a Service would help

- Lower barriers to launch by replacing a fragmented, multi-vendor gold stack with a single integrated platform.

- Embed controls and governance from day one through permissions, limits, approvals, monitoring, and clear operating processes.

- Improve redemption pathways by defining clear rules on minimums, platform fees, timelines, and supported pickup and delivery pathways.

- Enable mass market accessibility by supporting smaller minimums, more payment methods, and broader country coverage economically.

- Strengthen trust signals by standard audits and attestations, shared bar lists, control frameworks, and access to common insurance coverage.

- Access liquidity by connecting to an established network of liquidity providers from day one, without requiring independent sourcing arrangements.

4.3 Which gold products could Gold as a Service support and how?

Gold as a Service could be designed to fully support digital gold accounts and tokenised gold products, providing comprehensive infrastructure from product setup to custody, settlement, and reconciliation.

Digital gold accounts

Digital gold accounts allow a customer to hold gold as a balance of pool-allocated gold in grams or ounces in an app or digital space. Gold as a Service can support digital gold accounts to:

- Set up product processes in relation to platform fees, minimums, limits, eligibility, allocation and redemption options.

- Assist buy/ sell execution through the agreed liquidity model and settlement process, supporting counterparty relationships.

- Orchestrate custody and vault operations, including allocation and inventory updates where applicable.

- Keep customer balances aligned to underlying gold records using reconciliation and monitoring.

Gold tokens

Gold tokens are digital units mapped to a defined amount of gold, often designed to be transferable depending on the product and jurisdiction. Gold as a Service can support gold tokens to:

- Control the issuance and redemption of tokens, according to physical allocation and de-allocation rules.

- Apply transfer controls where needed, including limits, restrictions, whitelists, monitoring, and pausing.

- Keep token supply aligned to physical inventory records with continuous reconciliation and evidence outputs.

- Support defined redemption routes, either cash-out or physical delivery, depending on product term.

The current scope of Gold as a Service does not include end-to-end support for products such as gold ETFs which operate within established fund structures. Gold as a Service is primarily designed for digital-native issuance models and does not alter or replace existing ETF custody and structures. The scope is also separate to Pooled Gold Interests (PGI) which is a structure for holding and transferring gold at wholesale level. However, there is potential to extend the capabilities of Gold as a Service to support products such as gold ETFs, and to leverage PGI for holding and transferring gold as Gold as a Service evolves and market needs develop.

DEEP DIVE

Gold as a Service product issuance workflow

4.4 What are the implications of a market powered by Gold as a Service?

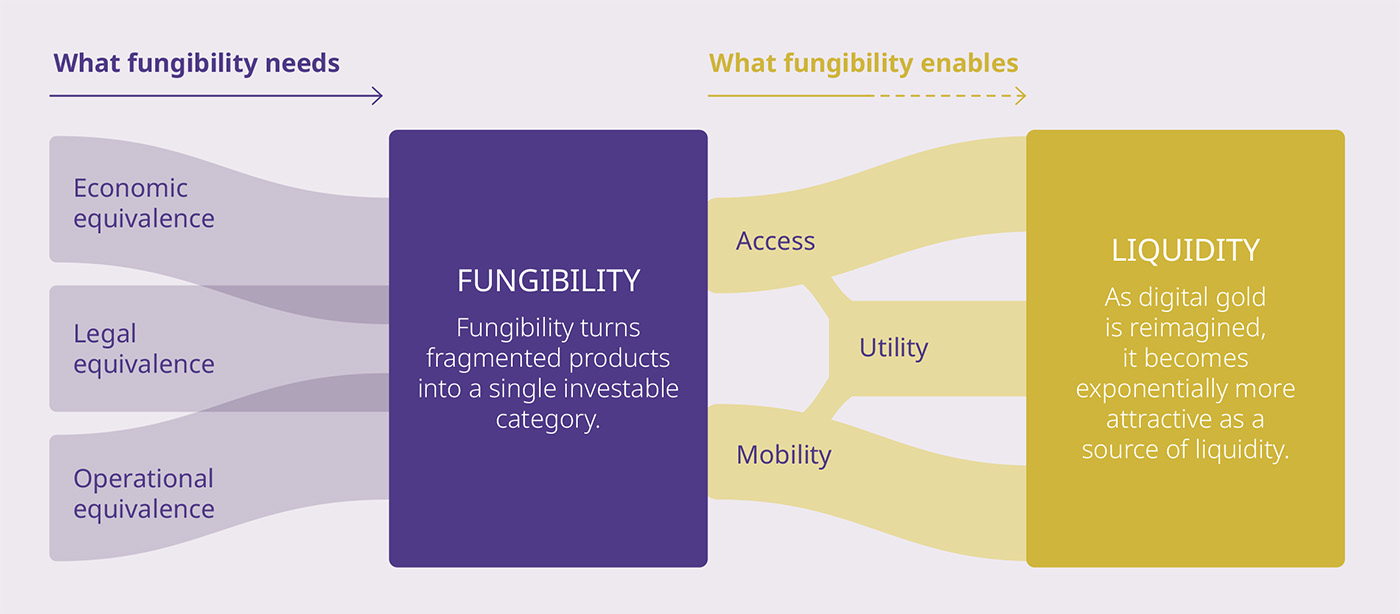

The central implication of a market powered by Gold as a Service is that it could enable market-level fungibility of digital gold. Rather than digital gold existing as a set of separate, issuer‑specific products, Gold as a Service could allow digital gold to function as a single asset with consistent backing, rights, and handling across the ecosystem.

In physical markets, gold is already reasonably fungible. Market participants trade gold based on standardised measures of weight and purity, with location, bar form, and custody handled through established market conventions. The challenge in current digital markets is that this fungibility breaks down. Digital gold units issued as different products often represent the same underlying metal, but differ in economic definition, legal rights, and operational treatment. Defining a common unit of gold value that is independent of bar size, location, or issuer provides a way to restore this principle. For digital gold to be fungible in practice, this economic equivalence must be matched with consistent legal and ownership rights and shared operational practices, including for custody, reconciliation, and assurance purposes.

What Gold as a Service changes

Gold as a Service could address fragmentation by providing shared infrastructure for digital gold products rather than leaving each issuer to build its own solutions. Core functions such as redemption, reconciliation, compliance controls, and assurance would be standardised.

This would allow digital gold units to circulate without being revalidated at every step. The shared infrastructure would also establish an extra layer of assurance for physical gold. Legal due diligence on physical ownership, custody, and backing would be embedded within the platform, rather than delegated to individual products or end users to interpret. Digital interfaces, distribution channels, and token implementation would remain the responsibility of participating issuers.

In practice, using Gold as a Service would signal that the product’s underlying gold is held within a continuously reconciled custody structure, with clearly defined ownership rights and redemption pathways. The assurance would only relate to the physical gold and its legal entitlements.

Enabling the ecosystem

While the platform's core focus would be on product issuance, the World Gold Council acknowledges the importance of product distribution and utility to the ultimate success of the digital gold ecosystem.

Accordingly, the platform is intended to encourage and enable third parties to build complementary products and services that help issuers maximise adoption and user value, on top of Gold as a Service.

Importantly, a thriving third party ecosystem would further benefit customers and developers by reinforcing Gold as a Service's core proposition, giving users more reasons to hold gold and encouraging more businesses to launch products.

A glimpse into a future enabled by Gold as a Service

A neobank launches its branded gold token in under two months using Gold as a Service. A customer buys 10 grams for long-term savings. When she needs a certain amount of cash in her local currency, she pledges 5 grams as collateral with one click to a participating lending institution. The gold is digitally locked in shared custody and a loan is issued instantly. Her remaining 5 grams stay fully usable. Once repaid with interest, the collateral unlocks automatically, without selling, re-custody, or re-documentation. She never sold her gold, never paid a spread, and never lost price upside, and her gold has become usable liquidity, not just a passive store of value.

Market results of fungibility

Once fungibility is in place, several practical outcomes follow. Redemption becomes simpler and more predictable. Instead of slow, opaque, issuer‑specific processes, digital gold can be converted into physical gold or cash through standardised flows connected to a global network of vaults, logistics providers, and liquidity partners. This would shorten redemption timelines and improves transparency around pricing and fees.

Fungibility also improves mobility and interoperability (Exhibit H). Digital gold would be able to move across products, platforms, and systems without the need for users to actively sell or repurchase - thus preserving economic exposure and reducing friction. A gold unit becomes transferable between custodians, platforms, and potentially chains without losing its recognised backing or requiring revalidation at each step.

Most importantly, fungibility expands practical utility. Digital gold could be pledged as collateral, allowing holders to borrow against it and unlock fiat without liquidating their gold exposures. It could be integrated into on-chain credit markets or liquidity pools, where predictable backing and redemption frameworks reduce counterparty uncertainty. It could also support programmable payments, enabling gold to move within digital transaction environments without requiring prior conversion into fiat. In traditional financial contexts, fungible digital gold could be incorporated more efficiently into funds, structured products, and collateral frameworks, as a result of simplified operational, legal, and valuation processes. Gold could remain a store of value, but also become deployable capital.

As digital gold begins to circulate across these workflows, liquidity will deepen. This supports tighter spreads and less slippage, more efficient collateral valuation, and greater resilience under stress. Taken together, these moves would represent a structural change in how digital gold would operate. Gold as a Service would not introduce a new product. It would enable the conditions under which digital gold can function as an interoperable and liquid financial asset.