- Gold has reached continuous highs in March and is trading close to US$2,200/oz

- Gold’s price increase of 6.5% m-t-d1 can, in part, be explained by a weaker USD, as well as higher risk and momentum...

- ...but other factors such as ‘technicals’ and over-the-counter (OTC) activity likely accelerated the move

- Looking forward, a sustained rally could trigger further investment flows but gold remains sensitive towards bond yield volatility in the short term.

A market searching for the trigger

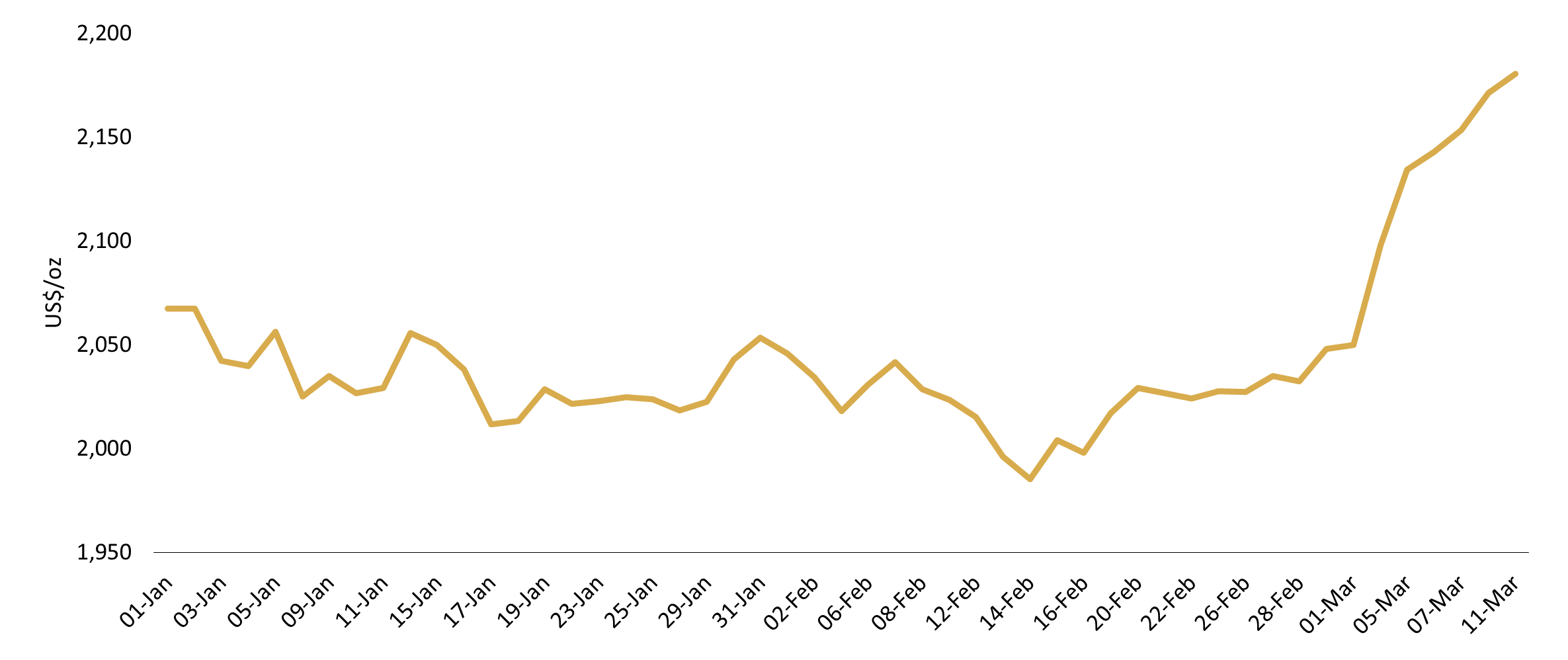

The gold price has shot up since the end of February, with the LBMA Gold Price PM trading at US$2,180.45/oz as of 11 March – a 6.5% increase m-t-d. Gold has reached consecutive record highs six days in a row and flirted with US$2,200/oz last Friday (8 March) in intra-day trading.

Chart 1: Gold reaches new highs in early March

LBMA Gold Price PM in USD per ounce*

Gold’s sharp increase has since caught the attention of market participants. The initial trigger was linked to a weak ISM print in the US on 1 March,2 pushing bond yields and the US dollar down.

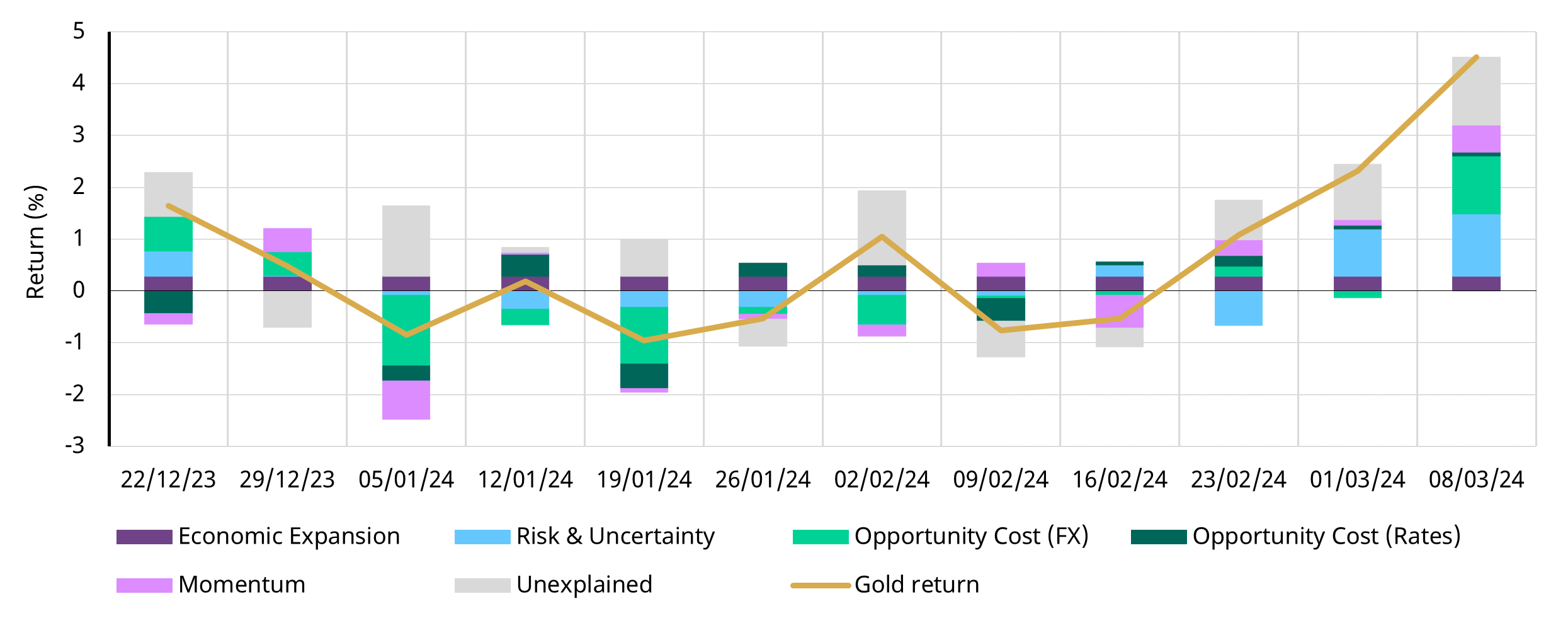

But that can only explain so much, so what’s behind gold’s move since? Our analysis, using a weekly version of our Gold Return Attribution Model (GRAM), indicates that gold’s performance can partly be explained by a few factors:

- US dollar weakness against both developed and emerging market currencies3

- An increase in market volatility

- More bullish COMEX investor positioning

- A drop in 10-year US Treasury yields.

Chart 2: Gold’s recent move can be partly explained by the USD, risk and momentum

Key drivers of gold’s return by week*

There is, however, a good portion of gold’s recent performance that can’t be explained by GRAM which - as with any other model - depends on the strength of historical relationships. As such, there are a few other factors that may explain the additional increase.

Firstly, gold’s rapid increase and its surge above a series of technical resistance and psychological levels from US$2,050 to US$2,100/oz likely served as a catalyst to cover short option strategies and drove further tactical investor interest. COMEX net long positioning – used by GRAM - comes with a lag and may not yet capture this data, although it could be inferred by more timely information on Open Interest.

Secondly, there’s also activity in the OTC market that may not be reflected in COMEX positioning or gold ETF flows but that likely provided further fuel to the market.

What’s next?

The key question now is how sustainable gold’s rally is.

On the plus side, gold started March aided by strong Chinese demand during the Spring Festival. And central banks have continued with their buying spree in 2024. In fact, we have highlighted in previous reports that gold’s strong performance over the past few years can be partly explained by geopolitical risk as well as robust central bank purchases – which are often reported with a lag. Finally, upcoming expiries in options markets may bring additional investment flows if the gold price remains above key psychological levels such as US$2,100/oz, which can be supported by continued US dollar weakness.

On the flip side, the upcoming US Federal Open Market Committee meeting will shed light on the Fed’s appetite to loosen monetary policy amidst downward revisions to previous non-farm payrolls reports and a slight uptick in unemployment.4 And while the market is not currently expecting a rate cut in March, a more hawkish stance by the Fed may create short-term headwinds for gold. In addition, rapid gold price movements typically discourage gold jewellery consumers, who may choose to wait for volatility to subside.

Stay tuned for our March Gold Market Commentary in early April for further insights.

Footnotes

As of 11 March 2024, based on the LBMA Gold Price PM USD.

US manufacturing contracts further, rays of light on the horizon | Reuters.

The US dollar weakness has been supported by additional soft economic releases and expectations of interest rate differentials between the US and other regions.

Feb US payrolls show labor market healthy but not overly tight | Reuters.