Summary

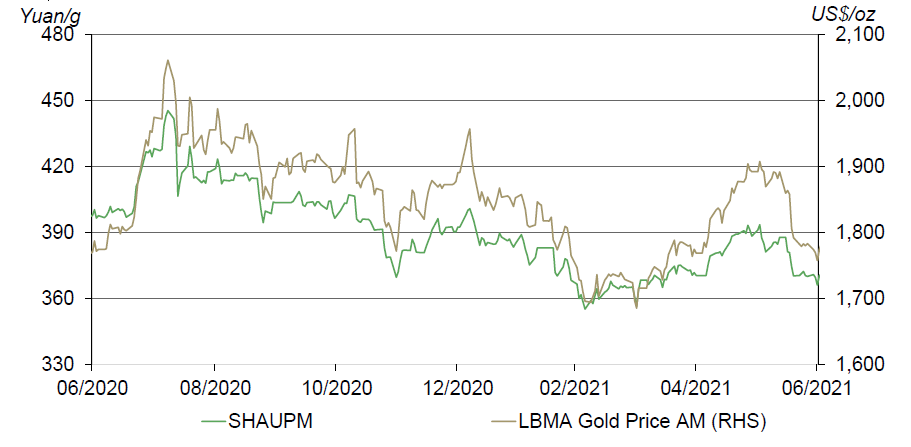

- The Shanghai Gold Benchmark Price PM (SHAUPM) (RMB) and the LBMA Gold Price AM (USD) dropped by 6.4% and 7.1% respectively in June1

- China’s economy remained strong in the second quarter

- Trading volumes of Au(T+D) on the Shanghai Gold Exchange (SGE) and gold futures on the Shanghai Futures Exchange (SHFE) hovered around previous lows

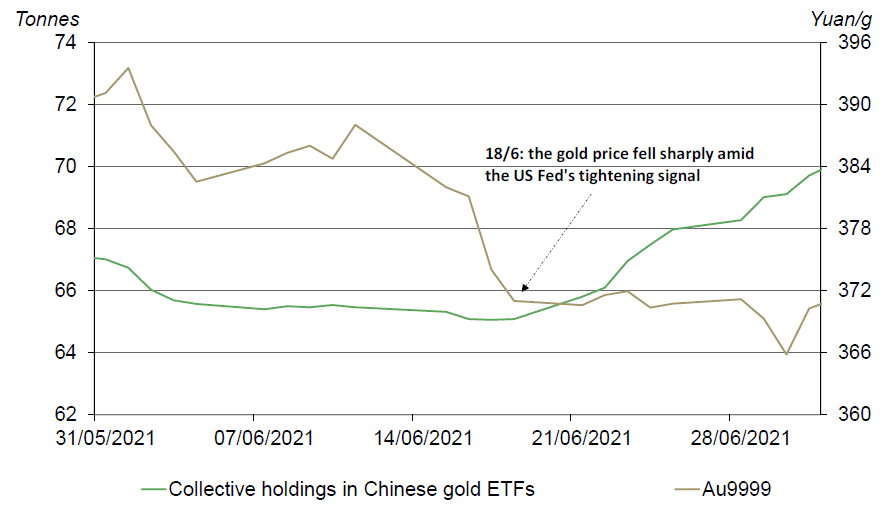

- By contrast, Chinese gold ETFs saw an inflow of 2.1t (US$123mn, RMB795mn) during the month

- Gold withdrawals from the SGE rebounded in June amid a greater replenishing need for manufacturers

- Gold held by the People’s Bank of China (PBoC) remained at 1,948t at the end of June, accounting for 3.3% of total reserves – unchanged since September 2019

- Chinese gold imports in May – totalling 67.6t – were close to pre-pandemic levels2

- The local gold price was at an average discount of US$4/oz against the international market gold price3

- As China enters the hottest days of the year in July, retail gold consumption could face challenges amid consumers’ rising preference of lighter-weight gold jewellery products and fewer outdoor activities in summer.4

International gold prices fell steeply in June. The weakness in the gold price can be largely attributed to the more-hawkish-than-expected monetary-tightening signals from the US Federal Reserve’s meeting on 18 June.5 But the decline in the RMB gold price was narrower than that of the USD gold price, thanks to a 1.6% depreciation in the CNY against the dollar last month.6

Gold prices fell in June

Source: Shanghai Gold Exchange, ICE Benchmark Administration, World Gold Council

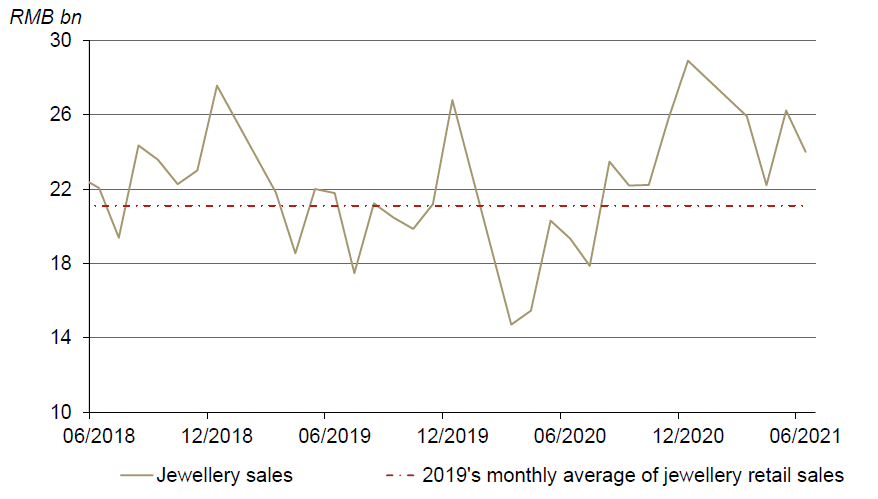

China’s economy remained strong. According to the National Bureau of Statistics, China’s GDP in Q2 rose 7.9% y-o-y, representing an average two-year growth of 5.5%, faster than Q1’s 5%. Also, household disposable income in the first half of the year rose by 12.6% y-o-y and is 15.4% higher than H1 2019. Primarily supported by the healthy economic growth and various consumption stimuli, the local retail sales of gold, silver, jade and gem jewellery in June remained above their pre-pandemic average.

Jewellery retail sales so far in 2021 have remained above their 2019 average

Source: National Bureau of Statistics, World Gold Council

To further strengthen economic growth and relieve pressure on the downstream industry’s margin amid rising commodity prices, the PBoC announced a cut in local banks’ required reserve ratios (RRR) on 9 July. The RRR cut – effective from 15 July – will lower the borrowing cost in the economy, thereby stimulating domestic demand and potentially supporting China’s gold consumption over the coming months.

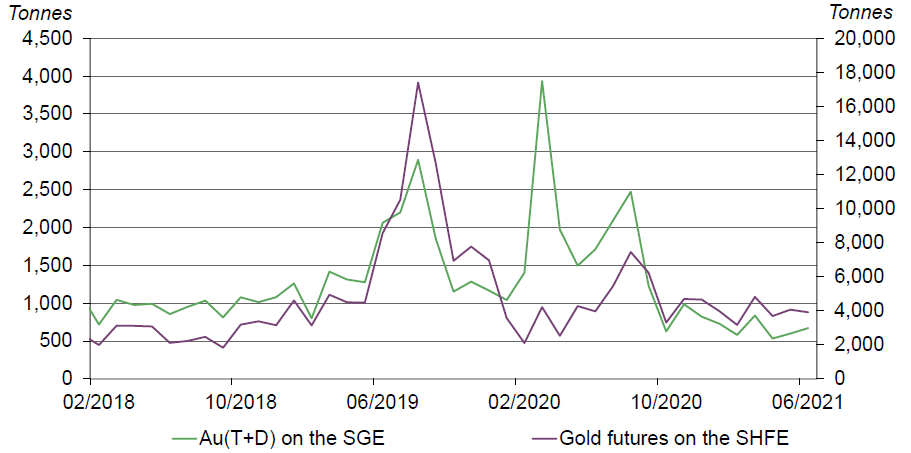

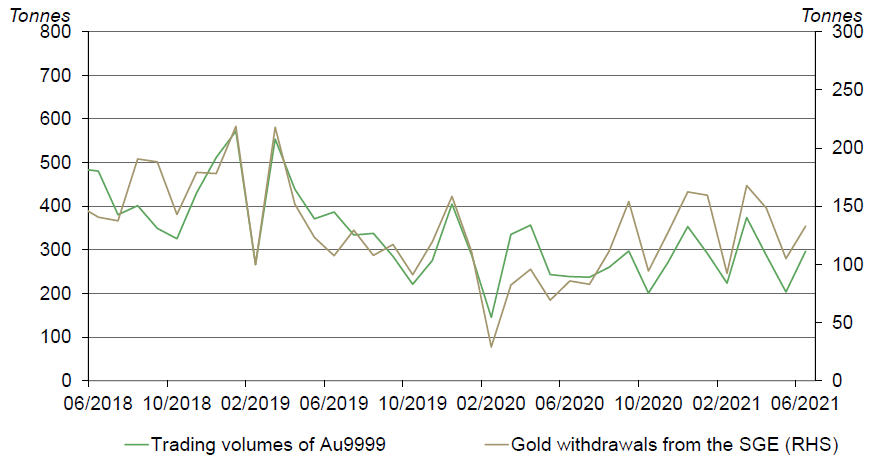

Trading volumes of Au(T+D) and gold futures remained tepid. Despite a 12% m-o-m rebound in Au(T+D)’s accumulative trading volumes last month, they remain 59% below their 2020 average of 1,649t. And trading volumes of gold futures on the SHFE in June totalled 3,908t in June, representing a 3.7% m-o-m decline.

Au(T+D) and gold futures trading volumes were stable in June

Monthly trading volumes of the most liquid margin-traded gold contract on the SGE and gold futures on the SHFE*

Source: Shanghai Gold Exchange, Shanghai Futures Exchange, World Gold Council

*Trading volumes of the SGE and SHFE gold contracts count both sides.

Chinese gold ETF holdings added 2.1t (US$123mn, RMB795mn) in June, totalling 68.7t (US$4bn, RMB26bn). In the first half of the month Chinese investors lost interest in gold ETFs as the gold price weakened, and this led to a 1.7t decline in the collective holdings of Chinese gold ETFs.

However, with the gold price decline accelerating, Chinese gold ETF holdings increased by 3.8t in the second half of the month. This could have been driven by local investors taking advantage of a lower gold price in order to build long-gold exposure or enter the market.

Investors' allocation to gold ETFs increased markedly late June

Source: Shanghai Gold Exchange, ETF providers, World Gold Council

Gold withdrawals from the SGE rose 27.7t m-o-m, totalling 132.8t in June. The combination of lower gold withdrawals and a relatively strong consumption during April and May – as indicated by our conversations with industry participants – may have led to a greater need for local gold manufacturers to replenish stocks. Consequently, their gold withdrawals from the SGE saw a m-o-m rebound in June on the heels of the previous two-month decline.

China's wholesale physical gold demand rebounded in June

Source: Shanghai Gold Exchange, World Gold Council

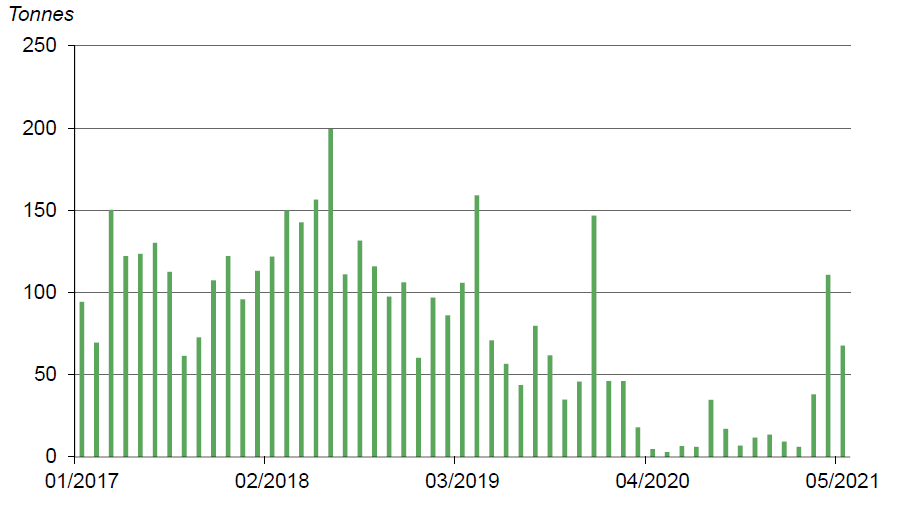

China’s gold imports were 67.6t in May, 65t higher y-o-y and only 3t lower than May 2019. China’s gold imports were muted in 2020 amid the pandemic-led plunge in local gold demand and strict border controls. But with the global COVID-19 pandemic easing and local demand improving, China’s appetite for gold imports has been recovering since early 2021, and is gradually normalising to its pre-pandemic level.

China's gold imports are approaching their pre-pandemic levels

Source: China Customs, World Gold Council

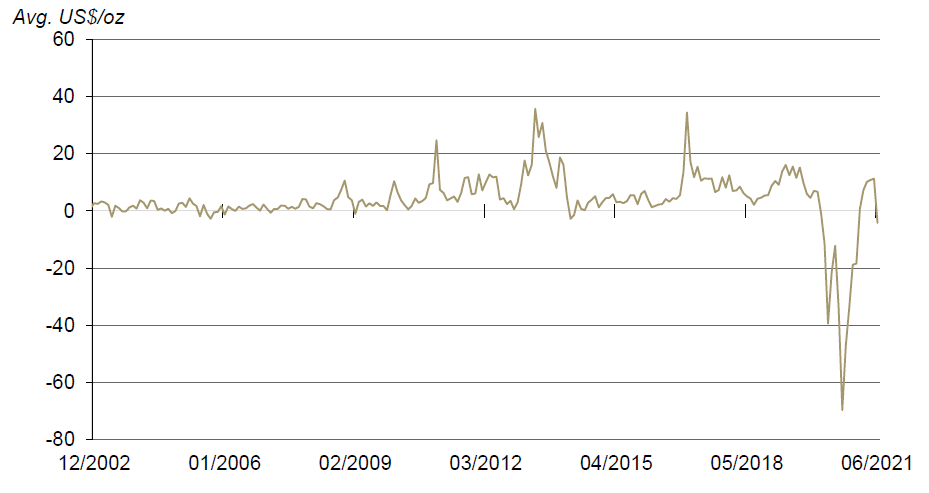

The Shanghai-London gold price spread averaged -US$4/oz in June, the lowest since December 2020. As mentioned in my previous blog, the higher risk appetite of Chinese investors in comparison to their Western peers, the expectation of tighter regulations in China’s gold market, and the recent surge in China’s gold imports, were principal drivers of the first negative Shanghai-London gold price spread in 2021, on a monthly average basis.

The local gold price spread has returned to premium so far in July. As our analysis indicates, with gold demand and demand expectation remaining healthy, drivers of the local gold price discount that we saw during June could prove to be short term.

The Shanghai-London gold price spread turned negative in June

Source: Bloomberg, Shanghai Gold Exchange, World Gold Council

*SHAUPM vs LBMA Gold Price AM after April 2014; before that, Au9999 vs LBMA Gold Price AM is used. Click here for more.

Footnotes

We compare the LBMA Gold Price AM to SHAUPM because the trading windows used to determine them are closer to each other than those for the LBMA Gold Price PM. For more information about Shanghai Gold Benchmark Prices, please visit Shanghai Gold Exchange.

There is a lag in gold import data due to China’s customs data release schedule.

For more information about premium calculation, please visit our local gold price premium/discount page.

Please visit China’s gold market in May: holiday-related sales drove retail gold consumption for more information.

For more information, please visit: Sharp gold selloff, but bullish activity could suggest a bottom | Post by Adam Perlaky | Gold Focus blog | World Gold Council.

Comparison made between the SHAUPM in RMB and LBMA Gold Price AM in USD.