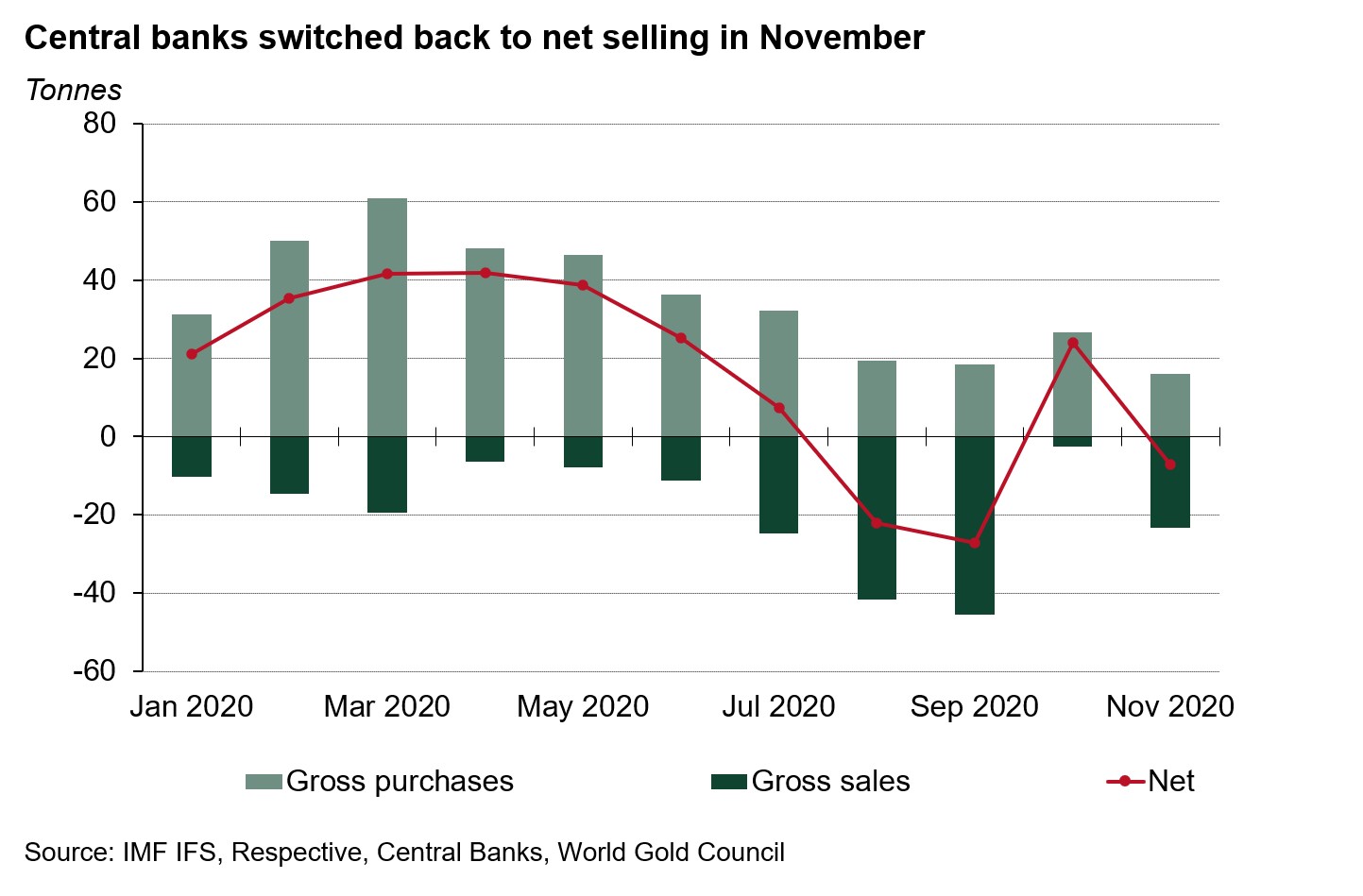

Following net purchases in October, central banks returned to net selling in November. Global official reserves declined by 6.5t during the month. Like August and September, when central banks were also net sellers, this was the result of continued moderate buying being offset by a few sizeable sales.

Central banks return to net sales in November

7 January, 2021

At a country-level, we can see that gross purchases amounted to 16t in November, broadly consistent with the levels of gold accumulation in August and September. Uzbekistan added another 8.4t to their gold reserves, while Qatar (3.1t), India (2.8t), and Kazakhstan (1.7t) were the other countries to increase official gold reserves in November. But this buying was more than offset by gross sales of 23.3t. In Turkey, higher local demand led to increased trading between domestic commercial banks and the central bank resulting in a 20.9t reduction in its reserves. This was not a strategic decision to lower gold reserves by the central bank. Mongolia was the other notable seller, reducing official gold reserves by 2.4t.

Overall, central bank demand has become more variable in recent months, oscillating between net purchases and net sales. This marks a change from the consistent buying we have become used to from this sector of the market. It therefore poses a couple of important questions.

Firstly, does this mean that the existing trend in net buying is now making way for a new trend? Or no trend at all? Since 2010, when central banks became consistent quarterly net buyers, there have nevertheless been several instances of monthly net sales, although not quite as concentrated as in H2 2020. And, with the exception of Turkey, these recent larger sales may be a consequence of the heightened uncertainty and fiscal pressure generated by the COVID-19 pandemic. Gold outperformed many other traditional reserve assets in 2020, giving central banks additional firepower to stabilise markets and currencies. But it may be too soon to confidently conclude whether the previous trend of consistent net buying will continue, or if it has ended and a new trend has emerged. The data for December and early 2021 will be crucial to help build a bigger picture.

Secondly, does this signal a longer-term change in attitude towards gold from central banks? We do not believe that central banks have shifted their mindset towards gold. As noted above, gold’s performance in 2020 (+25%) boosted reserve portfolios when it was needed. Our central bank survey conducted last year showed that gold’s role as a risk-mitigation asset is highly valued. While some uncertainty has eased in recent months (e.g., the US election and Brexit), the economic impact of the pandemic still poses significant risks which need to be managed.

Despite recent net selling, central banks remain on course to finish 2020 as net purchasers, making it 11 consecutive years since they were last net sellers on an annual basis. We will cover central bank demand for 2020 in more detail in the next edition of Gold Demand Trends, which will be published at the end of January.

Our central bank data for November 2020 is now available on Goldhub.