India gold market update: Mixed demand signals

17 July, 2026

- International and domestic gold prices1 fell sharply in June, and have broadly stabilised in July; ample domestic supply has kept the local market at a discount

- Overall consumer demand remained subdued in June, although jewellery buying reportedly picked up after the steep price fall. Major listed jewellers separately reported strong April-June revenue growth

- Investment demand diverged by channel: - gold ETF inflows and digital gold purchases strengthened in June, while bar and coin demand cooled

- Gold imports fell further in June, reflecting soft demand and sufficient domestic supply.

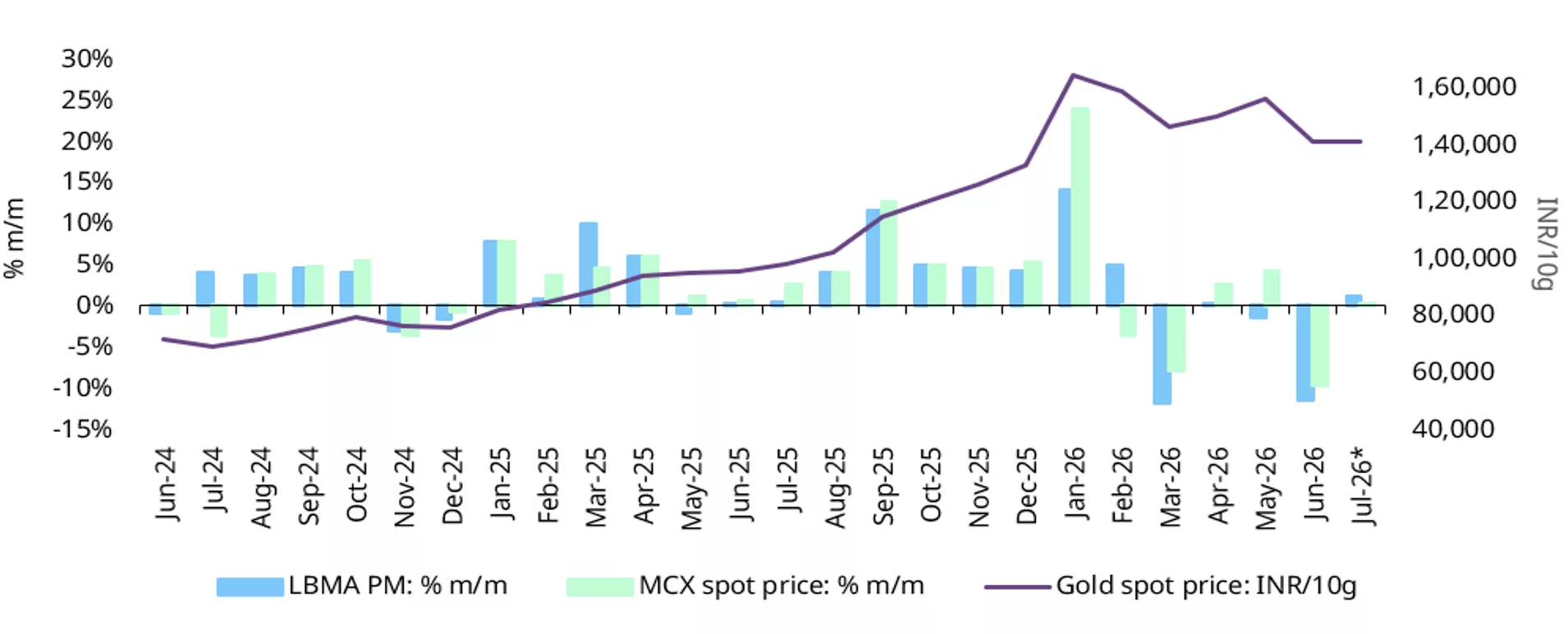

Gold comes under pressure

International and domestic gold prices recorded a sharp decline in June. The international price2 fell by more than 11% to around US$4,000/oz, its lowest level since October, while domestic price3 declined by around 10% to near INR141,000/10g, a six-month low. Although prices have recovered marginally since then, international gold price remains nearly 7% lower on a year-to-date basis. In contrast, domestic price is up around 6% y-t-d, supported by the 9% import duty hike in May and the INR depreciation against the US dollar.

A stronger US dollar, intensifying expectations of US rate hikes, and a rotation towards equities in Western markets have weighed on gold prices. At the same time, the pullback in prices has provided a buying opportunity to those waiting to enter the market, cushioning the decline in prices.

Chart 1: Gold weakens

Month-end LBMA Price PM and MCX spot gold price changes and movement*

*As of 14 July 2026. Source: Bloomberg, World Gold Council

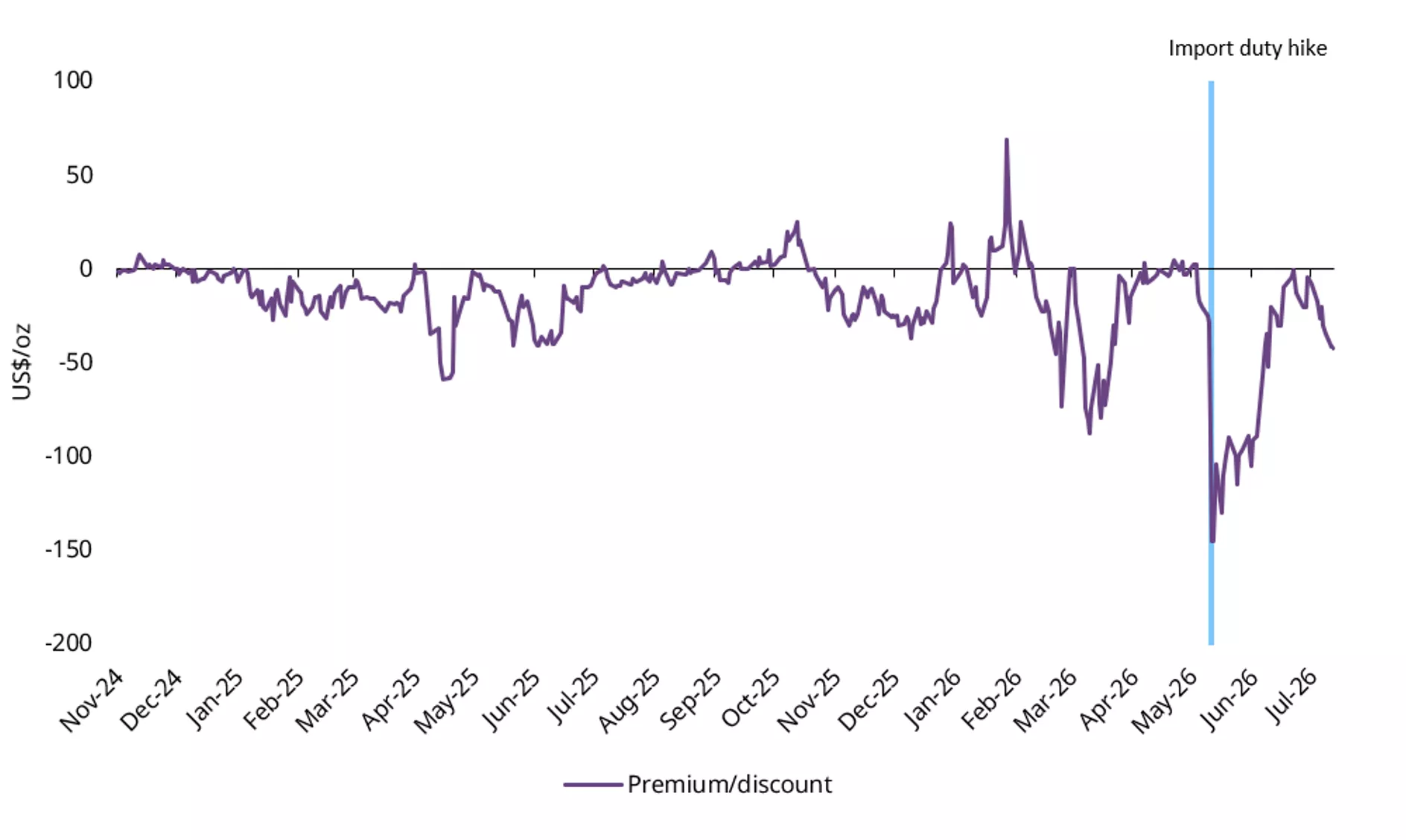

Ample supply keeps domestic prices at a discount

Gold price discounts in the domestic market have narrowed considerably from the elevated levels following the import duty hike in May and early June, indicating a gradual normalisation of market conditions. Discounts averaged around US$20/oz to the landed price4 during the first two weeks of July, significantly lower than the peak discount of nearly US$150/oz recorded in May. Domestic prices briefly traded close to parity with the landed price in late June and early July, indicating an improving market balance. Discounts have widened since to US$40/oz as of mid-July. The prevailing level of discount reflects the availability of ample domestic supply relative to demand. Industry interactions indicate that the rise in old gold exchange for new jewellery has increased the supply of gold in the market.

Chart 2: Discounts recede

NCDEX gold premium/discount relative to the official domestic price*

*As of 14 July 2026.

Source: NCDEX, World Gold Council

Jewellery buying gains traction

Following a month-long lull from mid-May to mid-June, driven by seasonally softer demand, an inauspicious period,5 policy measures and the Prime Minister’s appeal to limit gold purchases, consumer demand has reportedly begun to recover. Industry feedback suggests that while overall demand remains subdued, consumer buying has picked up in recent weeks, led primarily by jewellery. In contrast, bar and coin demand appears to have cooled.

The pullback in gold prices and the relative price stability are said to be stimulating jewellery purchases. The promotional campaign by retailers, including discounts, exchange offers, flexible payment terms, etc., have also been supporting sales. Notably, demand has not been limited to wedding-related purchases. Manufacturers too have been receiving order bookings from retailers in preparation for the festive season from August.

At the same time, softer prices have tempered demand for bars and coins, which are typically bought for investment purposes and tend to attract stronger interest during periods of rising prices.

Meanwhile, the exchange of old gold jewellery has gained further traction following the import duty hike in mid-May. Retailers report that exchange volumes have risen by a further 10–20%, with some indicating that old gold exchanges now account for as much as 70% of jewellery sales.

Healthy performance of listed jewellers in April–June quarter

Major listed jewellery retailers6 reported a strong April–June quarter despite an inauspicious period that typically tempers purchases. Revenue growth was broadly in the high 30–60% y/y range, supported by regional festivals, the summer wedding season and Akshay Tritiya7 during the early part of the quarter.

Demand was broad, with plain gold and studded jewellery registering double-digit sales growth. Retailers also reported growth both in customer additions and average ticket sizes.

Old gold exchange for new jewellery continued to rise on average accounting for somewhere between 43–55% of sales during the quarter, aided in part by promotional and marketing campaigns. These retailers continued with their store expansions, adding between 8 and 33 stores across the country during the quarter. The continued pace of store openings can be seen as reflecting industry confidence in the medium-term outlook for jewellery demand.

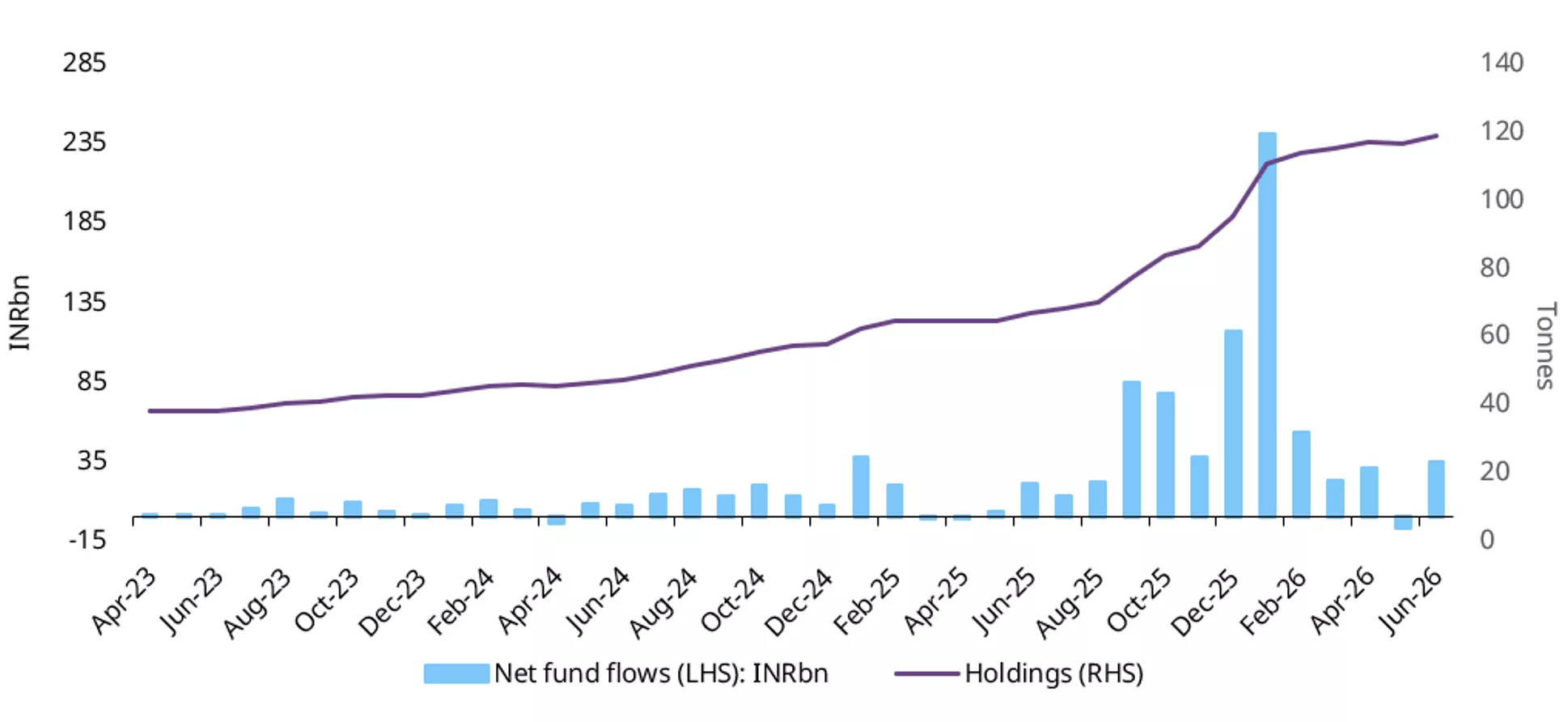

Price pullback drives ETF inflows

Indian gold ETFs recorded a rebound in June, in contrast to the global trend of outflows, as investors bought into the price dips. Net inflows during the month were INR34.4bn (US$356mn), the highest since February. Holdings increased by 2.2t to 119t, in line with our estimates, while the cumulative AUM fell 8% m/m, reflecting the decline in gold prices during the month.

The price pullback appears to have been viewed as a buying opportunity by investors, with inflows remaining healthy in early July. During 1–10 July, net inflows are estimated at INR12.1bn (US$127mn). Investor participation also broadened, with 135k new folios (accounts) being added during the month, taking the total number of accounts to 12.5mn.

Chart 3: Gold ETF flows rebound

Gold ETF flows in INRbn, and total holdings in tonnes*

*As of end June 2026.

Source: AMFI, ICRA Analytics, CMIE, World Gold Council

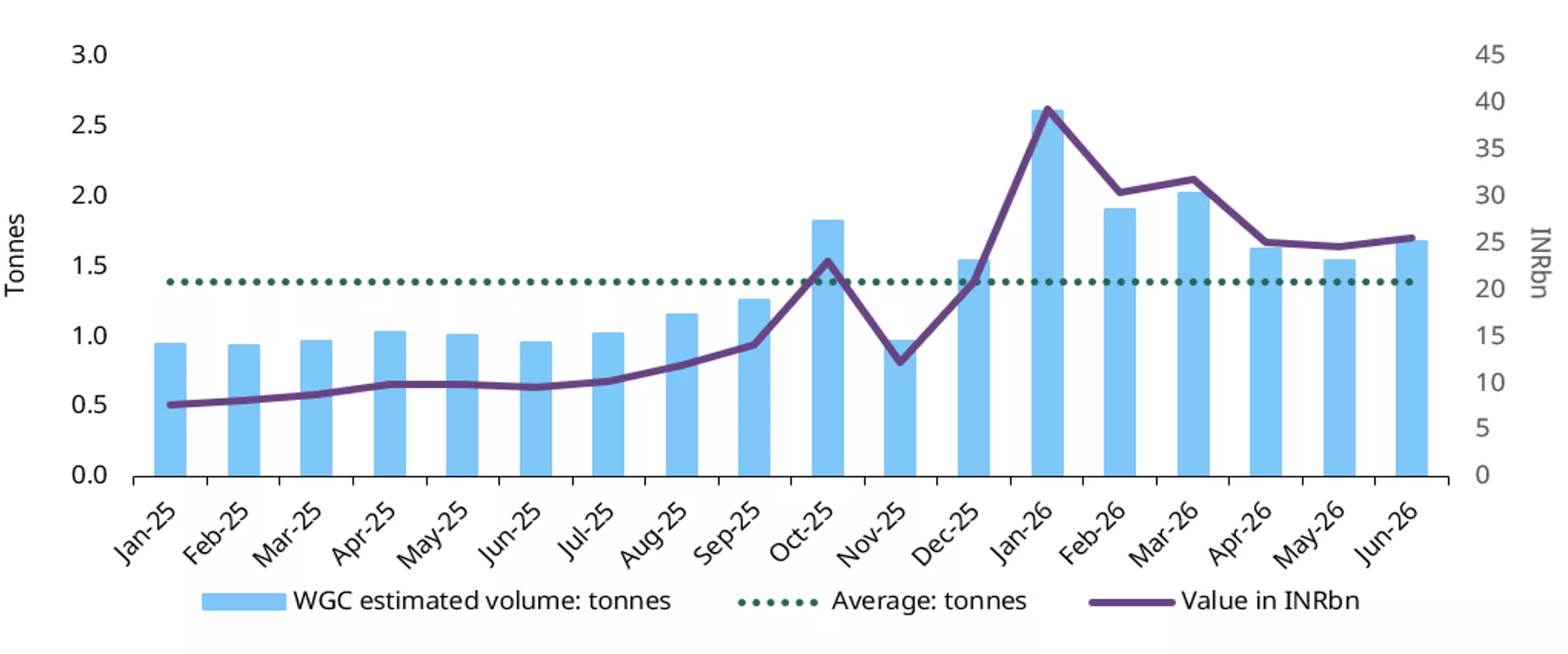

Increased buying of digital gold

Digital gold purchases through the Unified Payment Interface (UPI) rebounded in June after moderation in the previous month. Both transaction value and estimated volumes reached a three-month high, pointing to renewed investor interest. Transaction value rose 4% m/m to INR25.5bn (US$269mn), while volumes are estimated to have increased 9% m/m to 1.7t. Purchases during the month were above the 17-month average of 1.4t and remained within the higher-transacting category of UPI, suggesting that demand in the digital gold segment continues to be resilient.

Chart 4: Resilient demand in digital gold

Purchase of digital gold, by value and estimated volume

Source: NPCI, World Gold Council

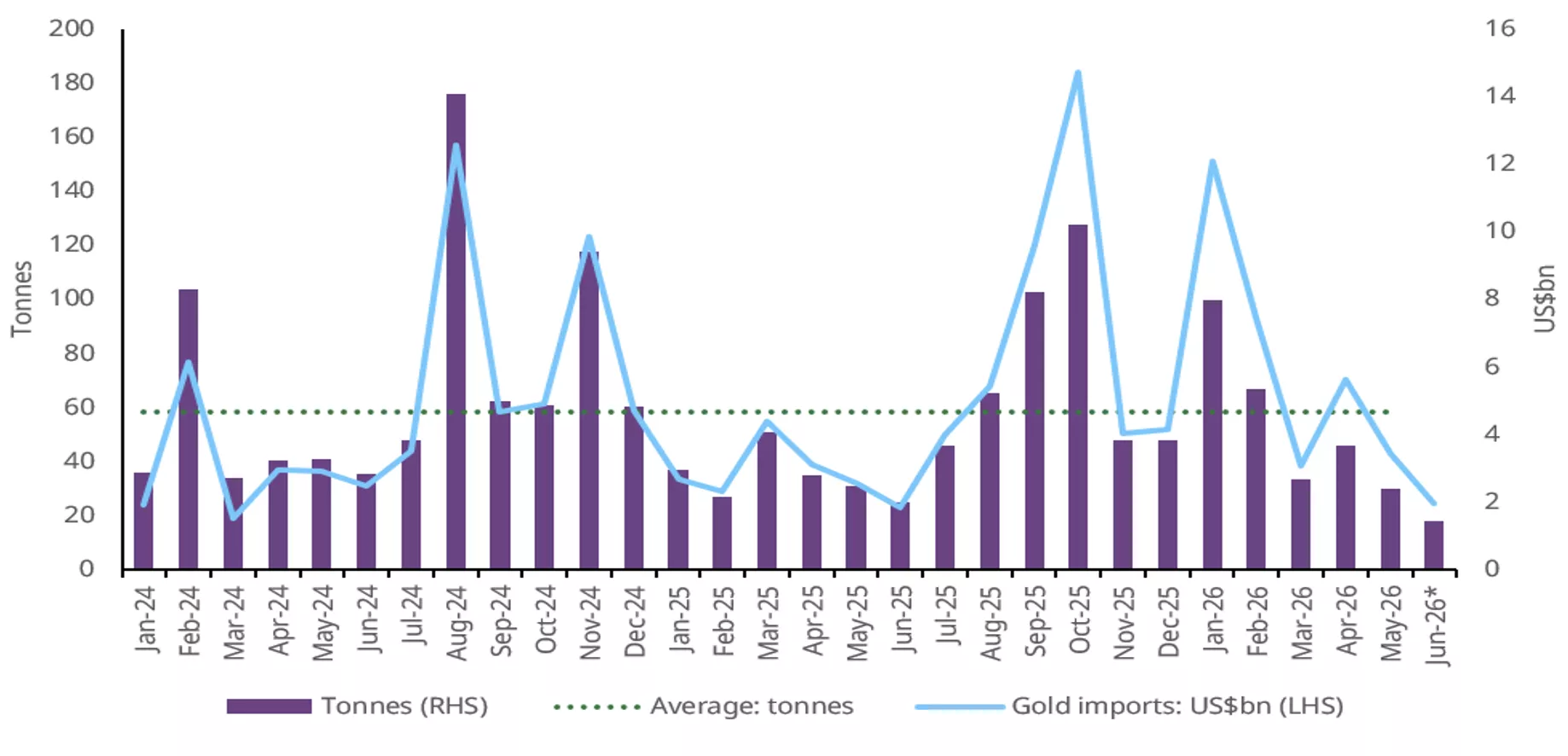

Imports ease amid soft demand and recycled supply

Gold imports weakened further in June, declining for a second consecutive month. At US$1.97bn, imports were down 42% m/m and the lowest since June 2025. However, import value was 7% higher y/y, driven largely by higher gold prices, with the average landed cost of gold rising 38% from a year ago.8 Import volumes in June are estimated at 16–22t, down from 29t in May and 25t in June 2025. The decline in import volumes is reflective of softer demand, elevated inventories in the supply chain, and supply from the exchange and sale of old gold. Old gold supply has risen since the import duty hike, lowering the need for fresh imports. Consequently, gold’s share of total merchandise imports fell to 3% in June, well below the 17% recorded in January.

Chart 5: Gold imports hit one-year low

Monthly gold imports in tonnes and US$bn*

*Includes World Gold Council estimates.

Source: Ministry of Commerce and Industry, CMIE, World Gold Council

Footnotes

1LBMA Gold Price and MCX Spot Gold Price as of 14 July 2026.

2LBMA Gold Price PM.

3MCX Spot Gold Price.

4Landed price is the international price (LBMA Gold Price AM) adjusted for import tax.

5Adhik Maas from 17 May to 15 June 2026.

6Titan Company Ltd, Kalyan Jewellers India Ltd, Senco Gold Ltd, PN Gadgil Jewellers Limited

7Akshay Tritiya (19-20 April) is traditionally regarded as an auspicious and key demand period for gold.

8Landed cost is the international price (LBMA Gold Price AM) adjusted for import taxes.

Disclaimer

Important information and disclaimers

© 2026 World Gold Council. All rights reserved. World Gold Council and the Circle device are trademarks of the World Gold Council or its affiliates.

All references to LBMA Gold Price are used with the permission of ICE Benchmark Administration Limited and have been provided for informational purposes only. ICE Benchmark Administration Limited accepts no liability or responsibility for the accuracy of the prices or the underlying product to which the prices may be referenced. Other content is the intellectual property of the respective third party and all rights are reserved to them.

Reproduction or redistribution of any of this information is expressly prohibited without the prior written consent of World Gold Council or the appropriate copyright owners, except as specifically provided below. Information and statistics are copyright © and/or other intellectual property of the World Gold Council or its affiliates or third-party providers identified herein. All rights of the respective owners are reserved.

The use of the statistics in this information is permitted for the purposes of review and commentary (including media commentary) in line with fair industry practice, subject to the following two pre-conditions: (i) only limited extracts of data or analysis be used; and (ii) any and all use of these statistics is accompanied by a citation to World Gold Council and, where appropriate, to Metals Focus or other identified copyright owners as their source. World Gold Council is affiliated with Metals Focus.

The World Gold Council and its affiliates do not guarantee the accuracy or completeness of any information nor accept responsibility for any losses or damages arising directly or indirectly from the use of this information.

This information is for educational purposes only and by receiving this information, you agree with its intended purpose. Nothing contained herein is intended to constitute a recommendation, investment advice, or offer for the purchase or sale of gold, any gold-related products or services or any other products, services, securities or financial instruments (collectively, “Services”). This information does not take into account any investment objectives, financial situation or particular needs of any particular person.

Diversification does not guarantee any investment returns and does not eliminate the risk of loss. Past performance is not necessarily indicative of future results. The resulting performance of any investment outcomes that can be generated through allocation to gold are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. The World Gold Council and its affiliates do not guarantee or warranty any calculations and models used in any hypothetical portfolios or any outcomes resulting from any such use. Investors should discuss their individual circumstances with their appropriate investment professionals before making any decision regarding any Services or investments.

This information may contain forward-looking statements, such as statements which use the words “believes”, “expects”, “may”, or “suggests”, or similar terminology, which are based on current expectations and are subject to change. Forward-looking statements involve a number of risks and uncertainties. There can be no assurance that any forward-looking statements will be achieved. World Gold Council and its affiliates assume no responsibility for updating any forward-looking statements.

Information regarding the LBMA Gold Price

The LBMA Gold Price is used by the World Gold Council with permission under license by ICE Benchmark Administration Limited and is subject to the restrictions set forth here (www.gold.org/terms-and-conditions).

Information regarding QaurumSM and the Gold Valuation Framework

Note that the resulting performance of various investment outcomes that can be generated through use of Qaurum, the Gold Valuation Framework and other information are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. Neither World Gold Council (including its affiliates) nor Oxford Economics provides any warranty or guarantee regarding the functionality of the tool, including without limitation any projections, estimates or calculations.

Information from ICRA Analytics Limited

All information obtained from ICRA Analytics Limited contained in this document is subject to the disclaimer set forth here (www.icraanalytics.com/terms-of-use/disclaimer).