China gold market update: October's unseasonable strength

18 November, 2025

Highlights

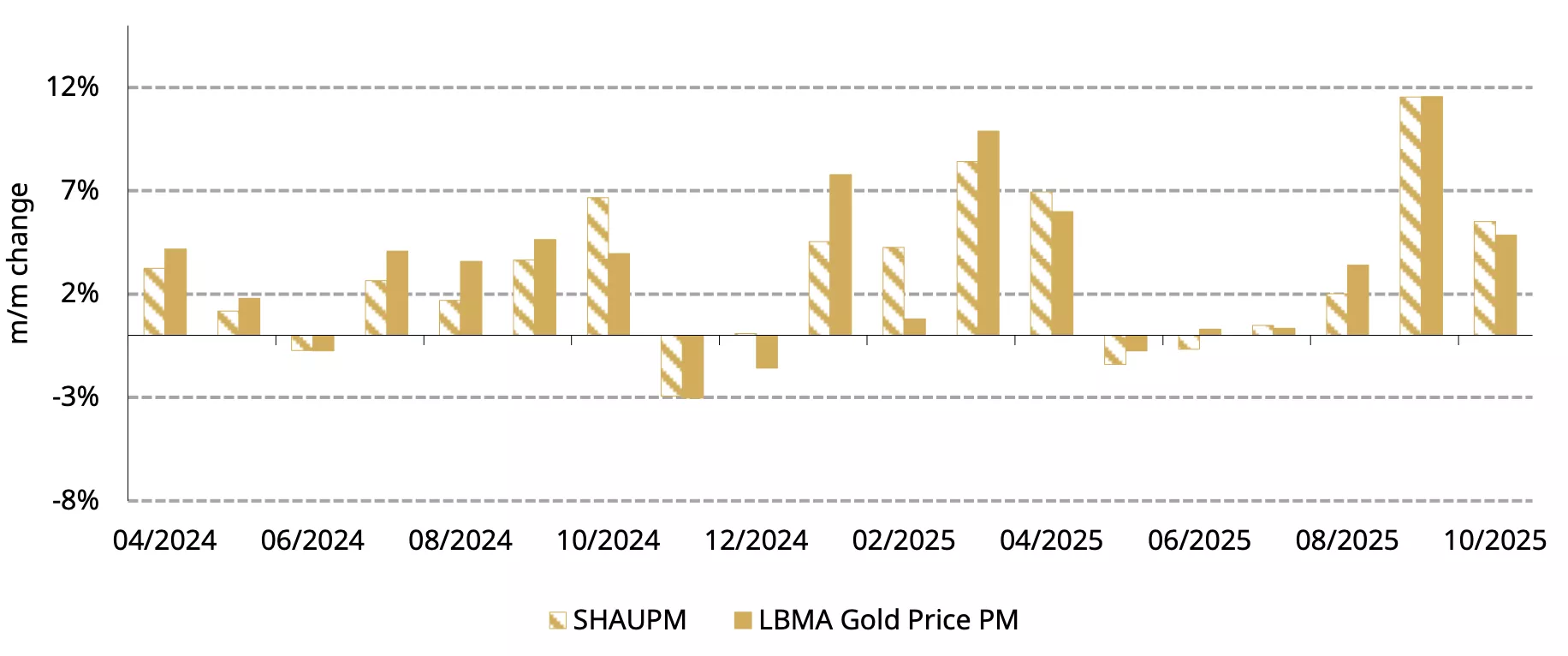

- Gold capped further gains in October. The LBMA Gold Price PM and the Shanghai Benchmark Gold Price PM (SHAUPM) rose 4.9% and 5.5% respectively in the month

- Wholesale gold demand defied seasonal patterns, rising both m/m and y/y to 124t in October

- Chinese gold ETFs added the notable amount of RMB32bn (+US$4.5bn, +34t) last month, and gold futures volumes surged at the Shanghai Futures Exchange (SHFE)

- The People’s Bank of China (PBoC) has reported gold purchases 12 months in a row, adding 0.9t in October, lifting the total to 2,304t, 8% of China’s foreign exchange reserves.

Looking ahead

- The recent Chinese gold market value-added tax (VAT) change is likely to put pressure on local gold jewellery demand as the sector is impacted by additional tax. But consumer sensitivity to price may also be lessening as the gold price has been rising steadily for more than three years now

- The VAT change does not apply to gold bars sold by SGE members, gold ETFs or gold accumulation plans (GAPs)1. And there may be further room for growth in gold bar sales, as consumers may purchase them for jewellery making purposes.

A divided but positive month for gold

For gold, October was a tale of two halves. The metal initially soared, setting successive records on various risks and strong ETF buying, before cooling later in the month as geopolitical concerns eased and profit-taking emerged. Ultimately, both the LBMA Gold Price PM and SHAUPM finished the month positive (Chart 1), extending their stellar y-t-d gains to 44% and 42%, respectively.

Chart 1: Global gold prices ended October with further gains

Monthly returns of the SHAUPM in RMB and LBMA Gold Price PM in USD*

*Data to 31 October 2025.

Source: Shanghai Gold Exchange, World Gold Council

And gold bounced higher in the first half of November, supported by rising risks and improving gold ETF inflows. The LBMA Gold Price PM in USD and the SHAUPM in RMB rose by 1.5% and 3.3% respectively during the first two weeks of November.

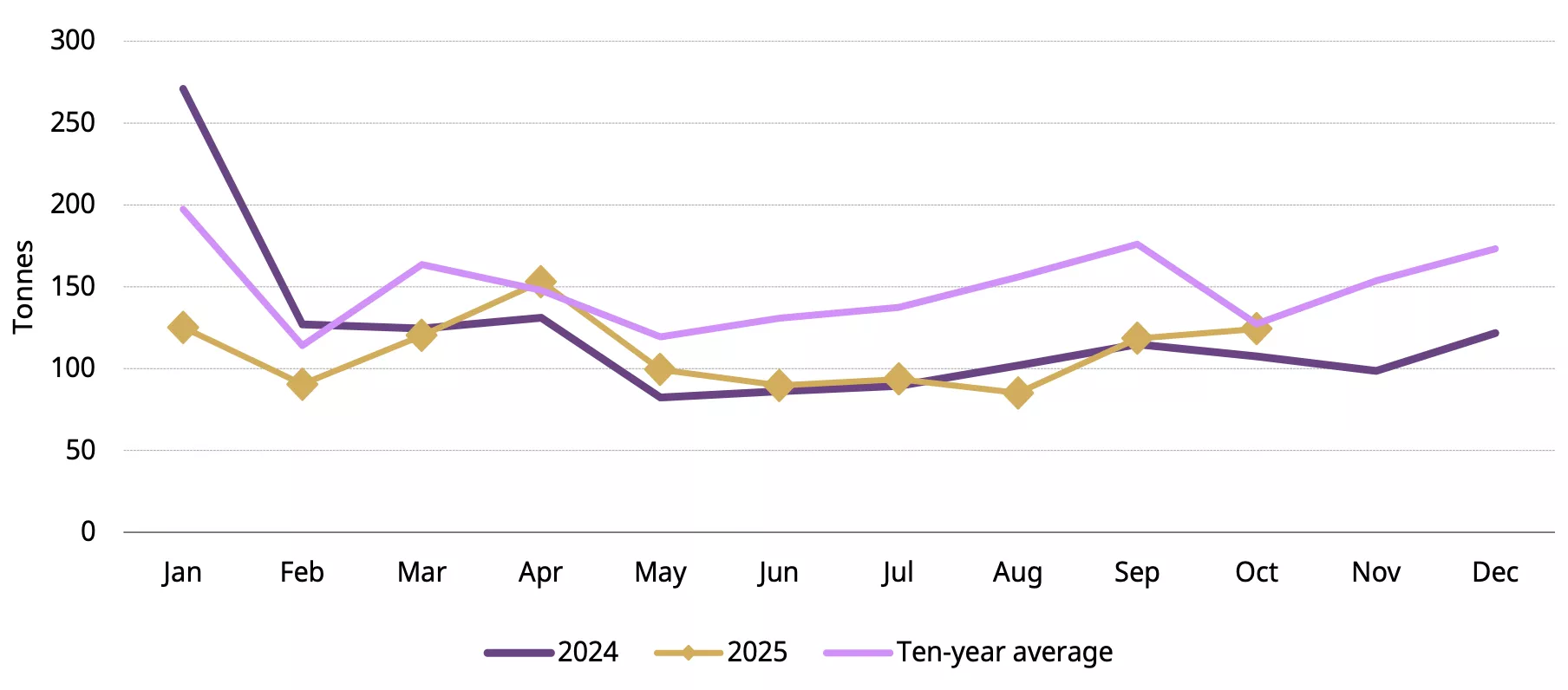

Wholesale gold demand defied seasonal weakness

Gold withdrawals from the SGE totalled 124t in October, 6t higher m/m and 17t higher y/y (Chart 2). This is almost on a par with the ten-year average of 127t. Investment demand improved further, especially in the first half of October when US-China trade tensions flared up, momentum in local equities cooled and the gold price surged, and this supported wholesale gold demand. Although gold jewellery consumption was robust during the early October nine-day National Day + Mid-Autumn Day holiday,2 retailers remained cautious in restocking amid the amplified gold price volatility earlier in the month.

Chart 2: Against seasonality, wholesale gold demand rose further in October

Monthly gold withdrawals from the SGE*

*The 10-year average is based on data between 2015 and 2024.

Source: Shanghai Gold Exchange, World Gold Council

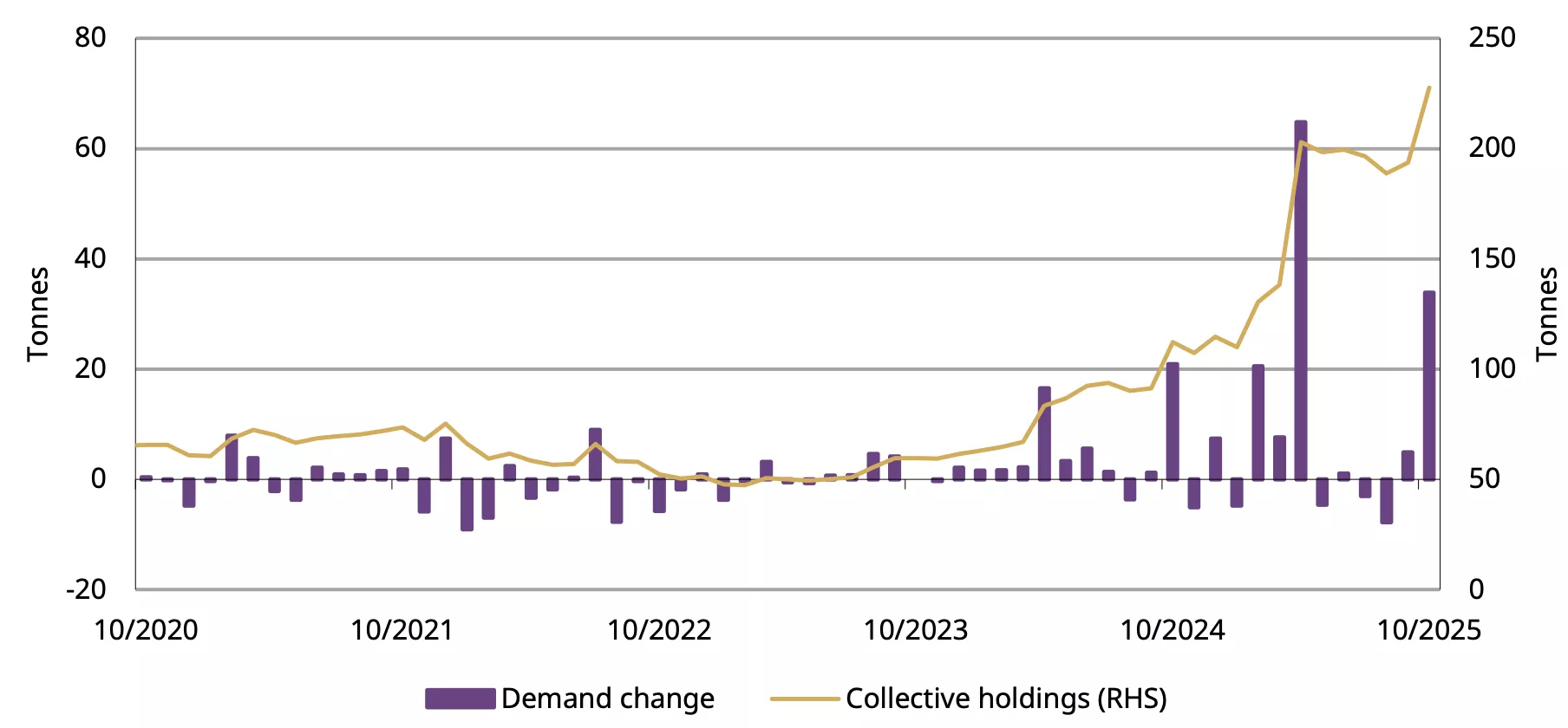

Gold ETF flows tracked the gold price

Chinese gold ETFs saw notable inflows in October, adding RMB32bn (US$4.5bn) in the month, the strongest since April. Their total AUM, supported by the hefty inflow and a higher gold price, jumped 24% to RMB210bn (US$29bn) whilst holdings surged 33t to 227t – both at their month-end peaks (Chart 3).

Earlier in the month geopolitical risks and equity market weaknesses drove Chinese investors toward the safe-haven of gold ETFs. But trade risks lessened after President Trump met President Xi in Korea, and the Fed’s hawkish cut tempered further bets of easing. And in response to lower safe-haven demand and a weakening gold price, local investor interest in gold ETF faded.

Investor interest in gold ETFs revived in early November, supported by local equity pullbacks, a rebounding gold price and rising geopolitical tensions.

Chart 3: Chinese gold ETFs saw notable demand in October

Monthly Chinese gold ETF demand and month-end holdings*

*Data to 31 October 2025.

Source: Company filings, World Gold Council

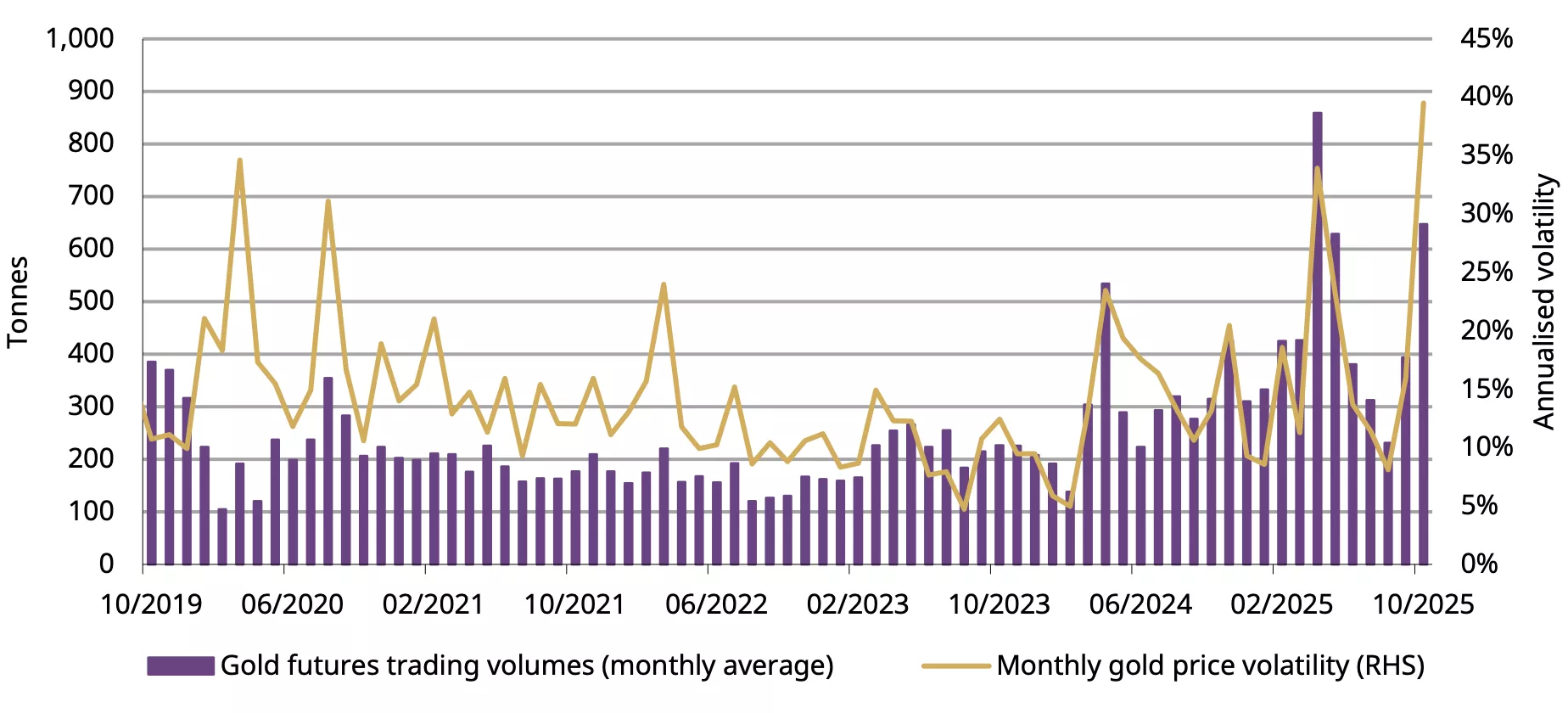

As gold price volatility surges, gold futures trading activity soars at the SHFE, averaging 647t per day in October, 64% higher m/m (Chart 4). And with the gold price volatility rising further, gold futures’ volumes in Shanghai stayed elevated in early November.

Chart 4: Gold futures trading activity surged in October

Daily average trading volumes of SHFE gold futures and monthly gold price volatility*

*As of 31 October 2025. The monthly gold price volatility is based on the daily gold price change in the active SHFE gold futures.

Source: Shanghai Futures Exchange, World Gold Council

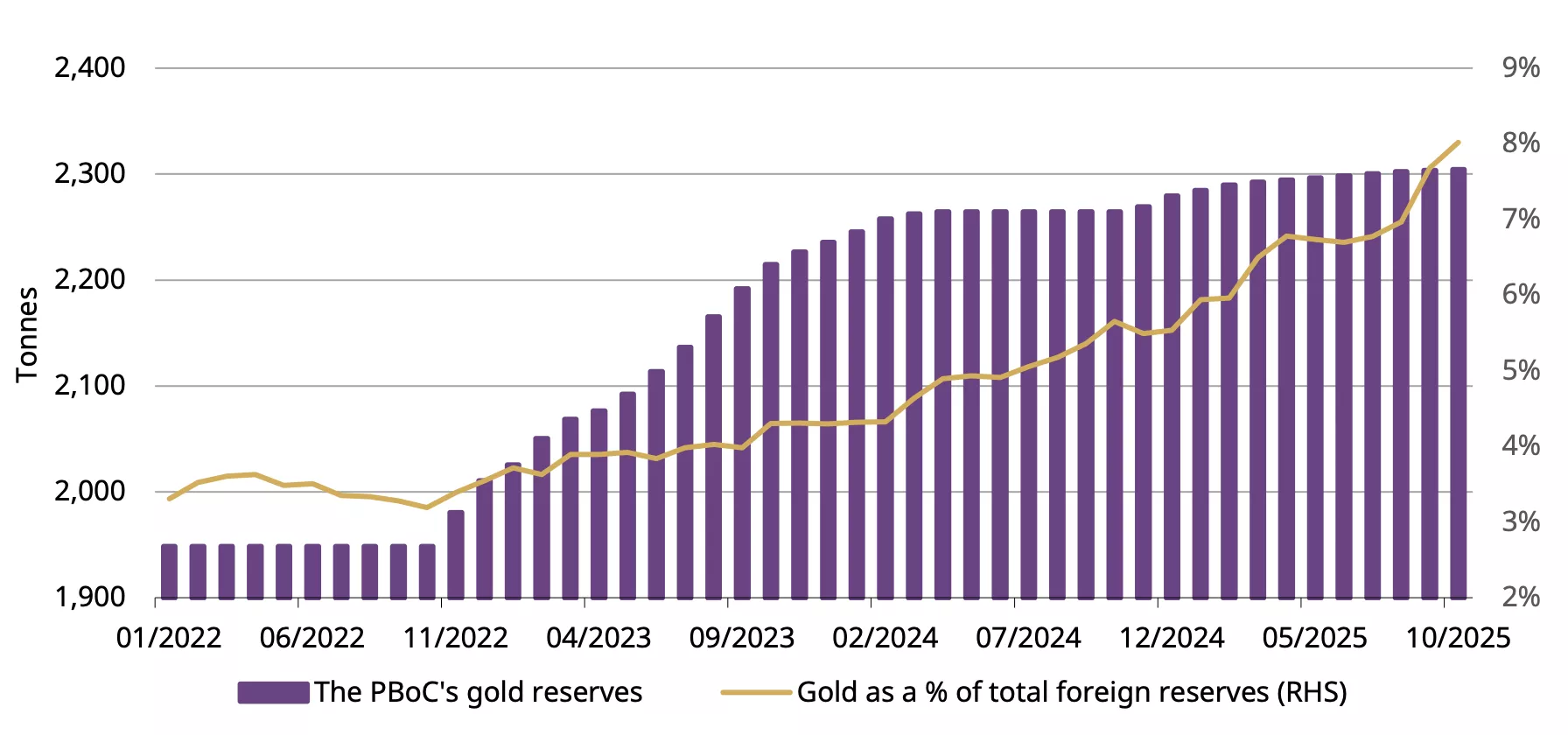

China’s official gold holdings climbed further

The PBoC reported its 12th consecutive monthly gold addition to its reserves in October, adding 0.9t (Chart 5). Continual purchasing so far in 2025 has pushed China’s official gold holdings to 2,304.5t, 24t higher than at the end of 2024. Meanwhile, gold’s share of China’s foreign exchange reserves has increased from 5.5% to 8%.

Chart 5: China’s official gold reserves have risen 12 months in a row

The PBoC’s reported gold holdings and their share of total foreign exchange reserves*

*Data to October 2025.

Source: State Administration of Foreign Exchanges, World Gold Council

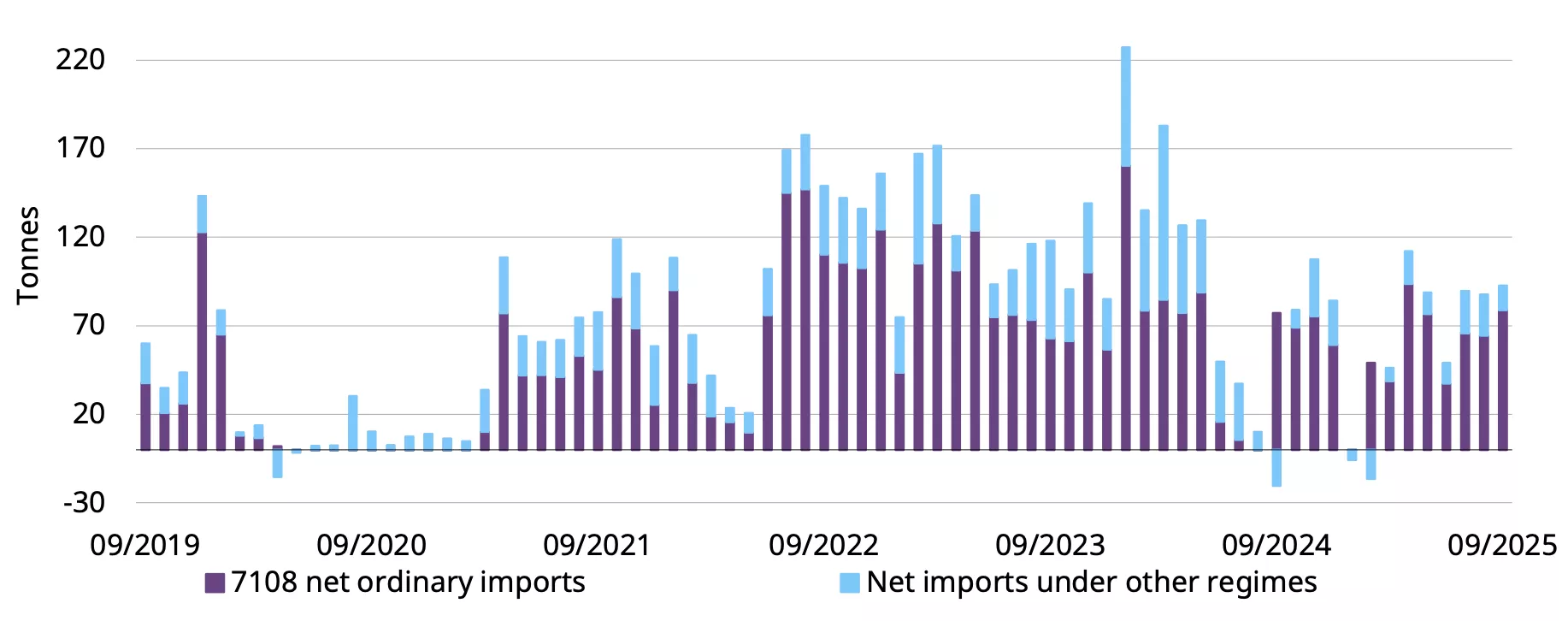

September imports bounced higher

China’s net gold imports amounted to 93t in September; data from China Customs shows that imports were 5t higher m/m and 36t higher y/y (Chart 6). This is consistent with the pattern we saw from September’s wholesale demand – the month’s gold withdrawals rebounded both m/m and y/y.

Chart 6: Gold imports rebounded in September

Net 7108 gold imports under various regimes*

*Based on the latest data available. Data to September 2025.

Source: China Customs, World Gold Council

Footnotes

1While these products are not impacted by the VAT reform, product providers may adjust their specific policies such as threshold of trading.

Disclaimer

Important information and disclaimers

© 2025 World Gold Council. All rights reserved. World Gold Council and the Circle device are trademarks of the World Gold Council or its affiliates.

All references to LBMA Gold Price are used with the permission of ICE Benchmark Administration Limited and have been provided for informational purposes only. ICE Benchmark Administration Limited accepts no liability or responsibility for the accuracy of the prices or the underlying product to which the prices may be referenced. Other content is the intellectual property of the respective third party and all rights are reserved to them.

Reproduction or redistribution of any of this information is expressly prohibited without the prior written consent of World Gold Council or the appropriate copyright owners, except as specifically provided below. Information and statistics are copyright © and/or other intellectual property of the World Gold Council or its affiliates or third-party providers identified herein. All rights of the respective owners are reserved.

The use of the statistics in this information is permitted for the purposes of review and commentary (including media commentary) in line with fair industry practice, subject to the following two pre-conditions: (i) only limited extracts of data or analysis be used; and (ii) any and all use of these statistics is accompanied by a citation to World Gold Council and, where appropriate, to Metals Focus or other identified copyright owners as their source. World Gold Council is affiliated with Metals Focus.

The World Gold Council and its affiliates do not guarantee the accuracy or completeness of any information nor accept responsibility for any losses or damages arising directly or indirectly from the use of this information.

This information is for educational purposes only and by receiving this information, you agree with its intended purpose. Nothing contained herein is intended to constitute a recommendation, investment advice, or offer for the purchase or sale of gold, any gold-related products or services or any other products, services, securities or financial instruments (collectively, “Services”). This information does not take into account any investment objectives, financial situation or particular needs of any particular person.

Diversification does not guarantee any investment returns and does not eliminate the risk of loss. Past performance is not necessarily indicative of future results. The resulting performance of any investment outcomes that can be generated through allocation to gold are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. The World Gold Council and its affiliates do not guarantee or warranty any calculations and models used in any hypothetical portfolios or any outcomes resulting from any such use. Investors should discuss their individual circumstances with their appropriate investment professionals before making any decision regarding any Services or investments.

This information may contain forward-looking statements, such as statements which use the words “believes”, “expects”, “may”, or “suggests”, or similar terminology, which are based on current expectations and are subject to change. Forward-looking statements involve a number of risks and uncertainties. There can be no assurance that any forward-looking statements will be achieved. World Gold Council and its affiliates assume no responsibility for updating any forward-looking statements.

Information regarding QaurumSM and the Gold Valuation Framework

Note that the resulting performance of various investment outcomes that can be generated through use of Qaurum, the Gold Valuation Framework and other information are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. Neither World Gold Council (including its affiliates) nor Oxford Economics provides any warranty or guarantee regarding the functionality of the tool, including without limitation any projections, estimates or calculations.