Summary

- Following the plunge seen in early August, the Shanghai Gold Benchmark Price PM (SHAUPM) (RMB) and the LBMA Gold Price AM (USD) rebounded as investor expectations for the Federal Reserve to taper bond purchases change1

- Driven by a rebound in China’s wholesale physical gold demand, the local gold price spread climbed, averaging US$5.8/oz in August, US$4.1/oz higher m-o-m and on a par with the y-t-d average2

- Amid a resurgence of COVID-19 cases, China’s economic growth slowed in August

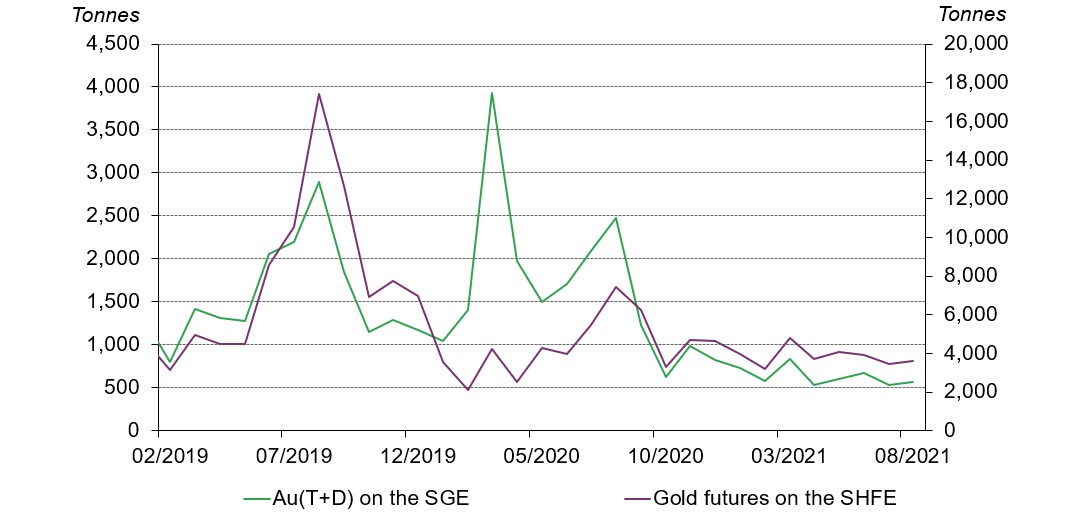

- Trading volumes of Au(T+D) on the Shanghai Gold Exchange (SGE) and gold futures on the Shanghai Futures Exchange (SHFE) amounted to 567t and 3,596t respectively in August, both higher m-o-m3

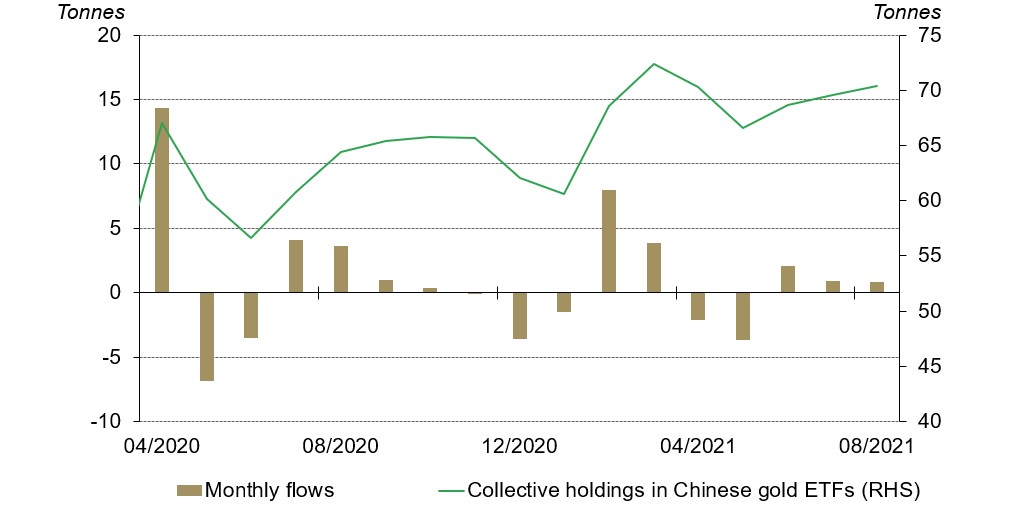

- Chinese gold ETFs continued to see inflows last month, bringing collective holdings to 70.4t (US$4.1bn, RMB25.3bn), an increase of 9.7t y-t-d4

- China’s wholesale physical gold demand rebounded in August as the gold consumption offseason comes to an end

- China’s gold imports in July were stable and above the 2019 level5

- While the approach of the traditional gold consumption peak season will likely be supportive for China’s physical gold demand, the recent spike in locally transmitted COVID-19 cases might pose challenges.

After plummeting in early August, gold prices rebounded. The LBMA Gold Price AM in USD and the SHAUPM in CNY dropped by 0.8% and 0.7% respectively in August. And changes in investor expectations for the US Federal Reserve’s monetary tightening have been the major factor driving the gold price lately. For more information, please read our Gold Market Commentary.

Gold prices saw declines in August

Source: Shanghai Gold Exchange, ICE Benchmark Administration, World Gold Council

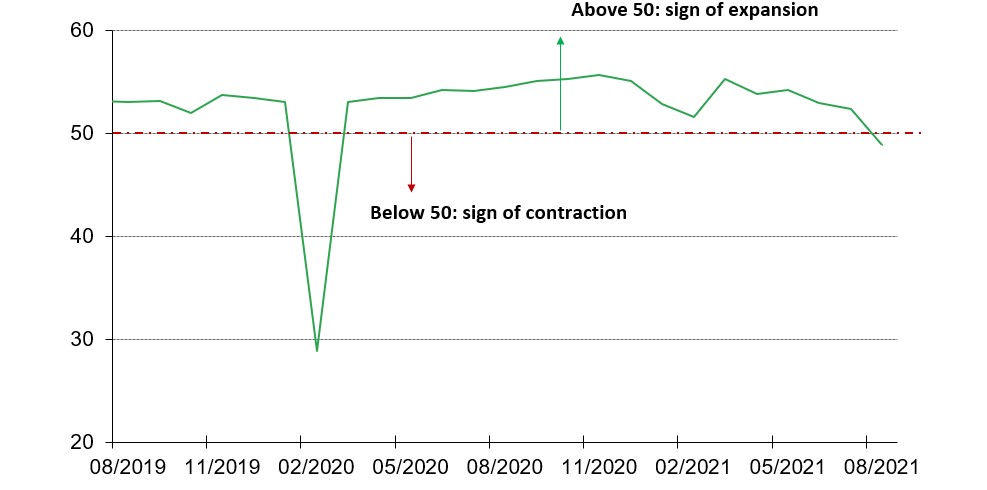

China’s economic growth weakened further in August amid the COVID-19 resurgence. According to the National Bureau of Statistics, China’s official composite Purchasing Managers’ Index (PMI) in August dropped below 50 – the threshold between expansion and contraction – for the first time since February 2020 when the COVID-19 outbreak was at its peak. Once again, China’s economic growth fell victim to the pandemic as strict social and travelling restrictions were reintroduced in multiple cities where cases of the Delta variant had been identified, including Nanjing and Yangzhou, among others.6

The composite PMI in China fell below 50 for the first time since February 2020

Source: National Bureau of Statistics, World Gold Council

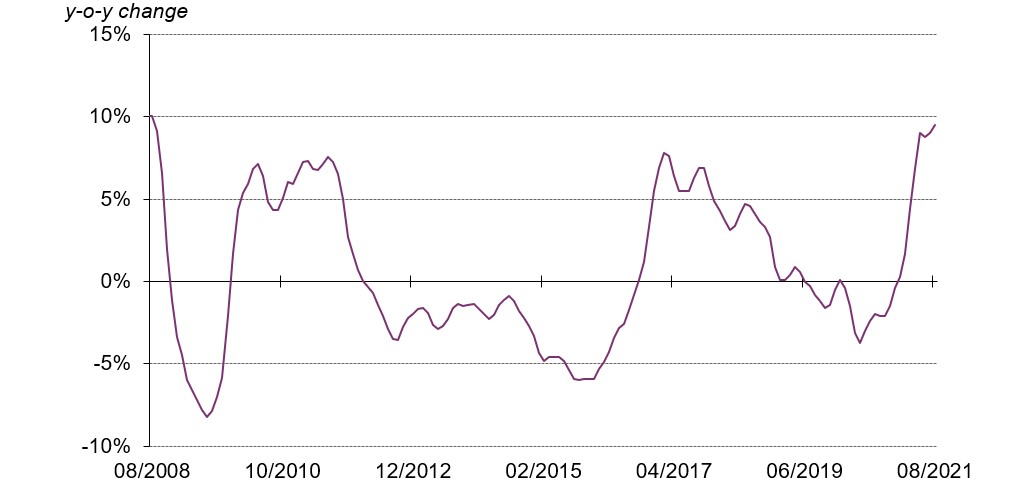

In the meantime, the August Producer Price Index (PPI) rose 9.5% y-o-y, the largest increase since August 2008. With industrial metals, coal and other major commodities in China surging for months, China’s PPI continued to rocket, accumulating inflationary pressure for consumers.

China's PPI continued to surge in August

Source: National Bureau of Statistics, World Gold Council

Trading volumes of Au(T+D) on the SGE and gold futures on the SHFE rose 6.5% and 3.9% m-o-m respectively. Higher gold price volatility in August than in July might have increased short-term trader interest in these contracts, leading to the m-o-m rise in trading volumes.

However, the trading volumes were significantly lower y-o-y. This is perhaps not surprising considering the context: in August 2020 the local gold price in China recorded its historical high, headlining local news and attracting tremendous attentions from investors.

Trading volumes of Au(T+D) and gold futures rebounded mildly

Monthly trading volumes of the most liquid margin-traded gold contract on the SGE and gold futures on the SHFE*

Source: Shanghai Gold Exchange, Shanghai Futures Exchange, World Gold Council

*Trading volumes of the SGE and SHFE gold contracts count both sides.

Chinese gold ETF holdings totalled 70.4t (US$4.1bn, RMB25.3bn) as of the end of August, a 0.8t (US$38.6mn, RMB298.3mn) increase m-o-m, witnessing net inflows for the third consecutive month. The CSI300 stock index remained volatile and weak, following its worst month since October 2018, and this weighed on risk appetite. Also, many investors took advantage of gold’s early August price plunge to enter the market or increase their gold ETF holdings.

Inflows into Chinese gold ETF holdings continued

Source: ETF providers, World Gold Council

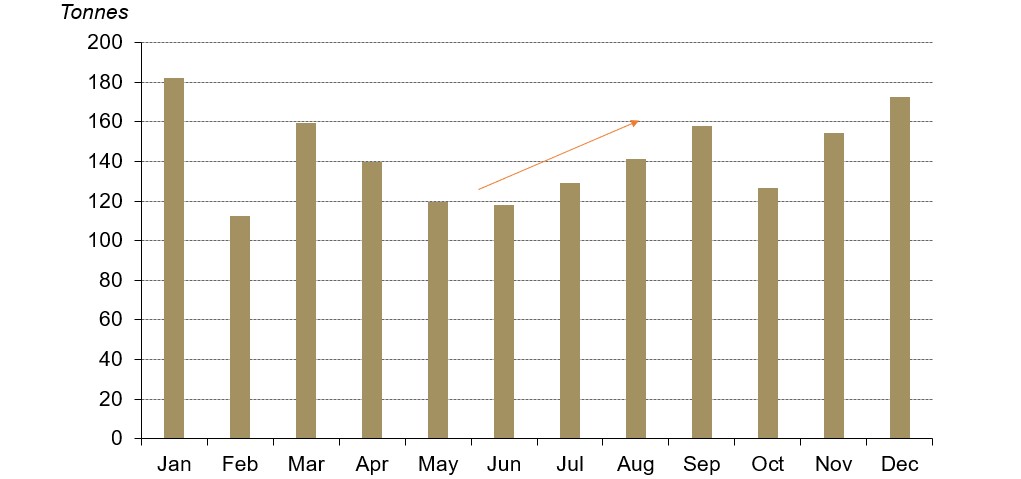

Gold withdrawals from the SGE totalled 150t in August, 39.3t higher m-o-m and 38.6t higher y-o-y. Historical data analysis shows that China’s wholesale physical gold demand tends to rise after the offseason for gold consumption in Q2 and early Q3. Manufacturers usually promote their products through the annual Shenzhen Jewellery Fair in early September or they reach retailers via their own trade shows, both of which necessitate an increase in replenishing activities during August.

Chinese wholesale gold demand tends to rise in August and September

Average monthly gold withdrawals from the SGE between 2010 and 2019

Source: Shanghai Gold Exchange, World Gold Council

As the offseason for gold jewellery consumption comes to an end, jewellers also start to prepare for festival and holiday promotions, such as the mid-Autumn Festival in September and the National Day Holiday in early October, thus lifting wholesale demand in August and September.7

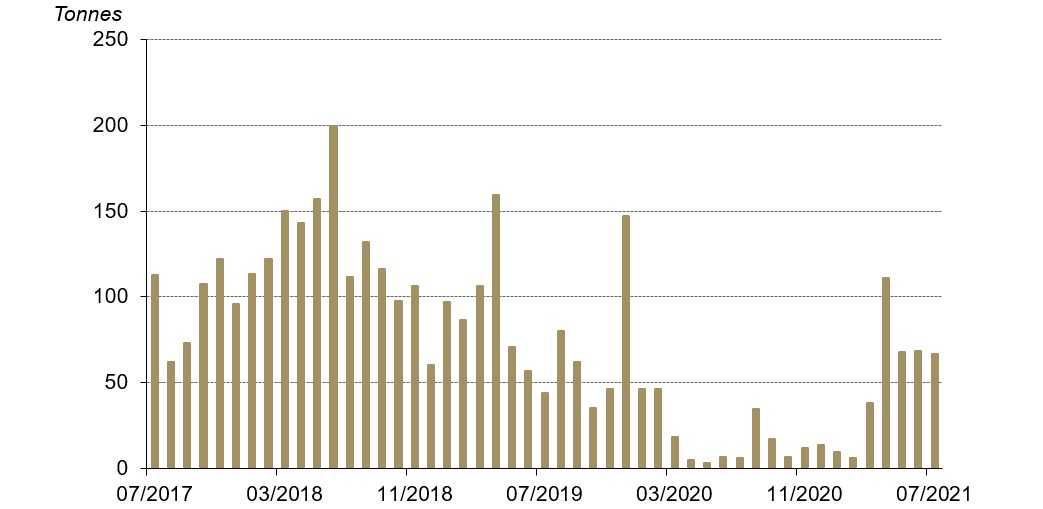

China imported 66.6t gold in July, 2t lower m-o-m and 22.9t higher than July 2019. As mentioned in our recent blog, regional floods and outbreaks of the Delta variant negatively impacted China’s physical gold demand in July, marginally reducing the appetite for gold imports compared to June. Nonetheless, imports have remained stable over recent months.

Gold imports remained stable in July

China's gold imports under HS code 7108

Source: China Customs, World Gold Council

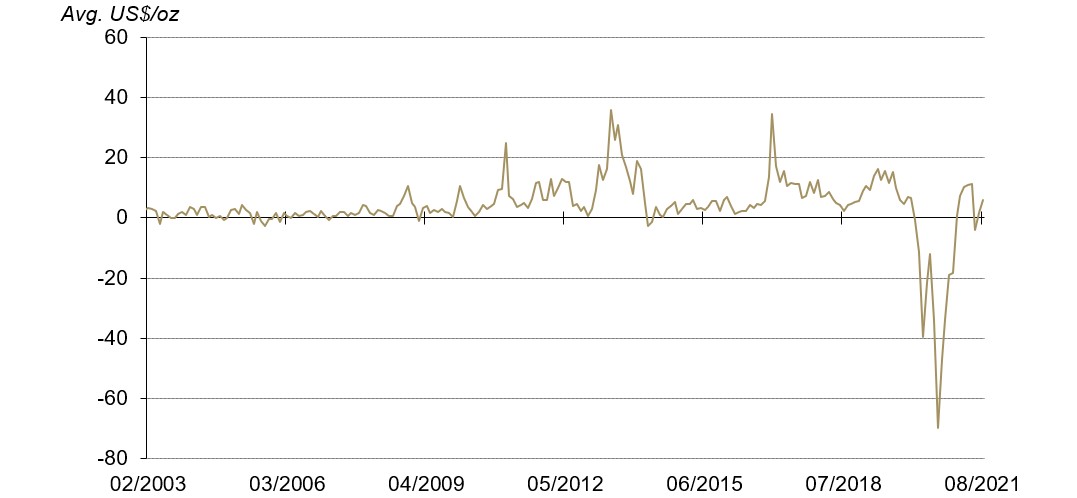

As China’s wholesale physical gold demand strengthened, the average local gold price spread rose to US$5.8/oz in August, US$4.1/oz higher m-o-m.

The local gold price premium rose further in August

Source: Bloomberg, Shanghai Gold Exchange, World Gold Council

*SHAUPM vs LBMA Gold Price AM after April 2014; before that, Au9999 vs LBMA Gold Price AM is used. Click here for more.

China’s physical gold demand in the coming months may benefit from seasonal purchases. As previously mentioned, with holidays approaching in September and October, consumers generally spend more on discretionary items such as gold jewellery, potentially creating higher wholesale physical gold demand.

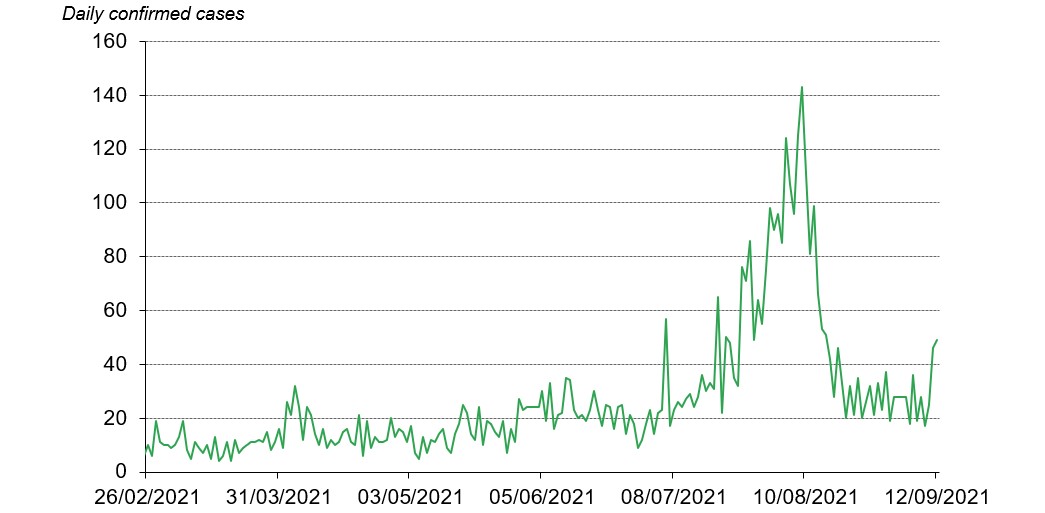

But the recent spike in locally confirmed COVID-19 cases might pose challenges. On 12 September, Putian, a major city in Fujian province, reported 32 locally transmitted confirmed COVID-19 cases and 32 local asymptomatic carriers.8 Following the announcement, strict social activity restrictions were implemented in the city.

In view of seasonal patterns, but bearing in mind the uncertainties of the pandemic, we are cautiously optimistic for China’s physical gold demand in the near future.

Locally confirmed COVID-19 cases in China started to rise again in September

Source: National Health Commission of China, World Gold Council

Footnotes

We compare the LBMA Gold Price AM to SHAUPM because the trading windows used to determine them are closer to each other than those for the LBMA Gold Price PM. For more information about Shanghai Gold Benchmark Prices, please visit Shanghai Gold Exchange.

For more information about premium calculation, please visit our local gold price premium/discount page. The y-t-d average refers to the average daily local gold price spread between January and July.

Volumes count both sides.

Please note that the inflow/outflow value term calculation is based on the end of period Au9999 prices in RMB and the USD/CNY rate.

There is a lag in gold import data due to China’s customs data release schedule.

For more information, please visit: https://covid19.who.int/table

The mid-Autumn Festival holiday will run from 19 September to 21 September 2021. The National Day Holiday will occur between 1 October and 7 October 2021.

For more information, please visit: Putian reports 32 COVID-19 cases; Delta variant likely - Chinadaily.com.cn