A recent FT article highlighted research from Moody’s which has estimated that global households have saved an extra US$5.4tn since this start of the COVID pandemic. This, the article goes onto say, could pave the way for a strong rebound in consumer spending, boosting the economic recovery.

Since the start of the year, economic optimism has generally been on the rise. Stock markets have continued to rally, and yields have risen as investors have switched their attention to potential inflationary pressures that come with economic expansion. Much of this is thanks to the unprecedented levels of monetary and fiscal stimulus from governments across the globe. Against this backdrop, gold has struggled. And some might think that a wave of consumer spending, propelling economic growth higher can only be negative for an asset considered a hedge against financial turmoil.

But, while risk and uncertainty may be lower, the potential impact on gold is a little more nuanced than some investors might realise. So, how might this increased stock of savings impact gold then? Well, for this we can look to gold’s dual nature, both as an investment and a consumer good. Gold’s different sources of demand, and how they impact gold’s behaviour, are key to understanding its diversification benefits.

Gold has a dual nature

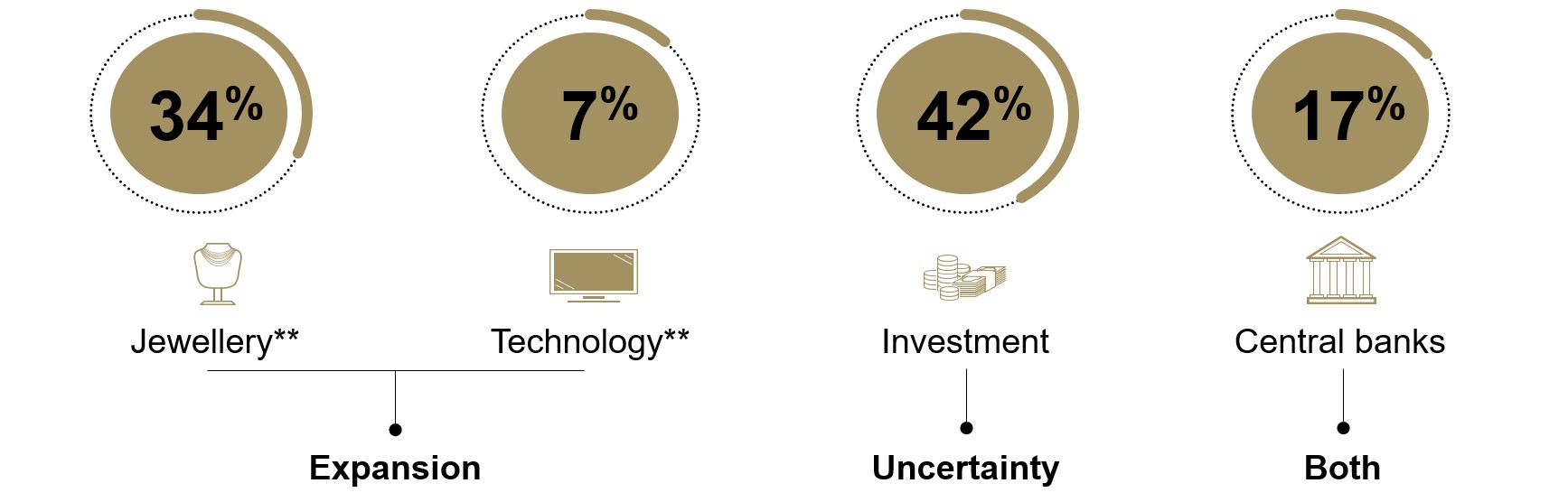

Average annual net demand ≈ 3,100 tonnes* (approx. US$177bn)

Source: Metals Focus, Refinitiv GFMS, World Gold Council

*Based on 10-year average annual net demand estimates ending in 2020. Includes: jewellery and technology net of recycling, in addition to bars & coins, ETFs and central bank demand which are historically reported on a net basis. It excludes over-the-counter demand. Figures may not add to 100% due to rounding. US dollar value computed using the 2020 annual average LBMA Gold Price PM USD.

** Net jewellery and technology demand computed assuming 90% of annual recycling comes from jewellery and 10% from technology. For more details, see: https://www.gold.org/goldhub/research/market-primer/recycling

Jewellery and technology demand can benefit from higher discretionary spending. Far from being negative, economic expansion is a positive force on certain elements of gold demand. Those consumers who are benefitting from bolstered budgets may seek to spend some of this on gold. Jewellery and technology demand, which combined account for around an average of 40% of annual net gold demand, are both pro-cyclical, meaning they are strongly linked to income growth and economic expansion. Higher discretionary spending could lead to higher demand for both. In fact, we are already starting to see signs of that with robust jewellery demand in both China and India, the two largest gold markets, in Q1.

Investment demand might also be supported despite lower uncertainty. While the counter-cyclical portion of investment demand – that linked to risk and uncertainty – may decline due to the more positive economic outlook, an element of investment might benefit from this higher level of savings. Consumers, aware that they are facing ultra-low or negative interest rates on their savings and the prospect of inflation, may opt to convert some of this into gold as it is a proven store of value. Again, there has already been evidence of this during Q1, with record levels of demand for gold coins from both the US and Perth Mint.

The conversion of the estimated US$5.4tn of savings into consumption has the potential to catalyse a rapid global economic recovery. But this positive development is not necessarily bad for gold. There has already been evidence of this so far in 2021, something we will continue to watch with interest for the rest of the year.

The full picture of gold demand in Q1 2021 will be covered in the forthcoming issue of Gold Demand Trends, published on 29 April.