Behavioural changes and new products

The traditional preference among Indian households for saving via physical products has benefited gold over several decades. It is worth noting that even as investors in urban India become more financially savvy, bars and coins remain a popular investment product. That said, the growing penetration of bank accounts and a broader access to financial products, along with the well-performing equity markets, have meant that physical gold investment has, at times, struggled.

The explosion of the digital economy has created a consumer base that is increasingly comfortable with online use. Among the large, young demographic there is a slow but structural shift in investment behaviour. Notably, while digital may have edged consumer preference away from physical gold investment, it has created opportunities for new gold-backed financial products to be marketed to a wide audience. And while investors have favoured equities over recent years, online trading gives them the ability to invest in whatever products they choose.

Competition from equities

Indian stock markets arguably present the biggest threat to gold investment among urban investors. Equities have performed exceptionally well over the last five years, with the two benchmark indices, Sensex and Nifty, rising by 79% and 72% respectively through to 2022.25 There has been a surge in investment from the middle class, much of which has been channelled through mutual funds where inflows have increased by 120% to US$119bn over the last five years.26

Investment in equities through the direct equity route has also risen significantly. Today, there are 108mn demat accounts in India; shares performed so well last year that about 25% of these accounts were opened in 2022 alone.27 Metals Focus believes that many young tech-savvy investors are looking to trade equities as a secondary income source.

Gold-related products have gained prominence

The pandemic fuelled safe-haven demand into Indian gold ETFs

The first Indian gold ETF was launched by Benchmark Asset Management in March 2007,28 closely followed by offerings from other banks and financial services providers. As the domestic gold price more than tripled – from Rs.9,390/10gm at the end of March 2007 to Rs.30,169/10gm at the end of January 2013 – inflows into these new gold ETFs surged.29 But soon after, investors turned instead to the rising equity markets. Gold ETFs faced further challenges with the launch of the sovereign gold bond (SGB) in October 201530 and the Indian gold ETF market saw continuous outflows from 2013 to 2018.

But in 2019, as the gold price rose more consistently, sentiment in the gold ETFs improved – albeit marginally. It was in 2020 that momentum picked up significantly. The rising gold price, increased volatility in equity markets and economic uncertainty due to COVID fuelled safe-haven demand. Net inflows almost doubled, taking total gold ETF holdings in India to 28.3t by the end of 2020.

This positive momentum carried into 2021. Net inflows increased by 9.3t, taking gold holdings to 37.6t by the end of the year. Inflows into Indian gold ETFs during 2022 were driven more by tactical moves. A higher domestic gold price due to the weak rupee contributed positively to many investors’ portfolios and some viewed these gains as opportunities to book profits. Others increased their holdings amid the volatile equity market and some utilised gold price dips to enter the market. By the end of 2022 there were 11 gold ETFs in the country with a total AUM figure of Rs.214.6bn (US$2.5bn) and gold holdings of 38t (Chart 7).31 The longer-term macroeconomic environment and rural-to-urban migration present future opportunities to further develop the gold ETF market in India (Focus 2).

Chart 7: Total holdings of Indian gold ETFs have increased since the pandemic

Chart 7: Total holdings of Indian gold ETFs have increased since the pandemic

Holdings of Indian gold ETFs on exchanges

Chart 7: Total holdings of Indian gold ETFs have increased since the pandemic

Holdings of Indian gold ETFs on exchanges

Source: Bloomberg, Respective gold ETF providers, World Gold Council

Sources:

Bloomberg,

Respective gold ETF providers,

World Gold Council; Disclaimer

Gold savings funds and multi-asset allocation funds provide additional opportunities to invest in gold ETFs

Gold savings funds are run by mutual fund houses, with the inflows invested in gold ETFs. Unlike direct investment in ETFs, investors use a systematic investment plan (SIP) rather than a demat account. However, some additional costs, such as an exit load (if funds are withdrawn in the first year); an expense ratio (the annual maintenance charge levied by the mutual fund); and fund commission, need to be borne by the investor, which tends to make these funds less competitive. At the end of 2022 there were ten such funds with a combined AUM of approximately Rs.68bn (US$0.8bn).32

Multi-asset allocation funds provide an alternative route into gold ETFs. These funds fall into a hybrid category that allow investment in at least three asset classes. Securities and Exchange Board of India (SEBI) regulations state that a minimum of 10% allocation is required in three asset classes (allocations of less than 10% are permitted for additional asset classes). The inclusion of multi-asset classes increases diversification and may lower overall portfolio risk. Allowed asset classes include stocks, debt, gold, commodities and REITs, among others. Investment in gold can be made through physical gold, gold-backed ETFs, or other gold-related investments such as derivatives or Sovereign Gold Bonds. Ten multi-asset allocation funds were in existence at the end of 2022 – with a combined AUM of Rs.146.5bn (US$1.7bn) – all of which have an allocation to gold in their portfolios (Table 1).

Table 1: List of multi-asset allocation funds with investment in gold

Total AUM and % of portfolio allocated to gold

* As of 31 December 2022. Allocation to gold refers to allocation in Gold ETFs, Gold futures and Sovereign Gold Bonds.

Source: Source: Factsheet of individual mutual funds, World Gold Council

Sovereign gold bonds (SGBs) have gained popularity due to additional fixed interest

SGBs are government securities denominated in grams of gold and issued by the RBI. These bonds were introduced to provide an alternative to holding physical gold and so reduce the impact on the country’s import bill. Investors pay the bond’s issue price in cash, which is then redeemed, also in cash, on maturity. Each unit is equivalent to the price of 1g of gold. Importantly, investors receive the market value of the gold at the point of maturity, plus 2.5% interest per annum (Table 2).

The RBI started to issue these bonds through commercial and state banks from November 2015, since when some 62 tranches have been released at broadly regular intervals. These have accounted for a combined total of 98t of gold.33

Focus 2: Indian gold ETF market: history and outlook

Gold ETFs are one of the greatest inventions of this century in the financial sector. Not only do they allow investors to take direct exposure to physical gold in a convenient, efficient and safe way, but the liquidity of the gold ETFs is also superior to the underlying physical markets at the retail level.

Gold ETFs are a relatively new investment product. The world’s first mutual fund was launched almost 100 years ago and the first ETFs almost 30 years ago, whereas the world’s first gold ETF saw the light of the day less than two decades ago. Moreover, gold is often considered a pariah in capital markets dominated by mainstream equity and debt markets. Add cryptocurrencies to that – the new competitor or pretender – and only time will tell.

In India, gold ETFs were permitted in 2007. The initial response was lukewarm as they were not considered a viable alternative to physical gold. However, gradually, as investors across the globe recognised the efficiency of investing through ETFs, assets under management in gold skyrocketed.

The credentials of gold ETFs were cemented as a bonafide portfolio hedge during the great financial crises of 2008 when gold’s safe-haven attributes were at their best. There was a significant hiccup from 2011 to 2013 as the so-called ‘taper tantrum’ prompted tactical investors to pull out money from gold ETFs much to the detriment of gold prices and sentiment.

Inflows resumed in 2016 as heightened volatility in risk assets, geopolitics, low real rates, negative sentiment on the US dollar and high private and public indebtedness made gold an effective hedge against the associated risks. Four years later, global gold ETF assets under management had doubled and so had the gold price. 2021 and 2022 witnessed outflows from gold ETFs due to rate hikes by central banks.

What is heartening to note is that Indian investors have reaffirmed their faith in gold ETFs and, despite volatility in gold prices we have witnessed inflows in 2021 and 2022.

In 2022 central bank net purchases of gold totalled 1,136t, the highest level of annual central bank demand since 1950. Also, the People’s Bank of China (PBoC) reported the first increase in its gold reserves since September 2019, purchasing 62t in 2022 and taking its total gold reserves over 200t for the first time. If other central banks resume buying we may witness a dramatic shift in sentiment towards gold.

Gold ETFs are now widely accepted investment products in capital markets across the world. However, retail participation in emerging economies like India and China remains abysmally low compared to retail physical demand, and makes up only a minuscule part of the mutual fund universe. There is a pressing need for investor education and media campaigns extolling the three virtues of gold ETFs – ease, efficiency, and safety.

Gold ETFs have lost some flows to cryptocurrencies, especially Bitcoin. Despite the hype, cryptocurrencies remain a tiny fraction of the bullion market. But then it would be unwise to dismiss them as a passing fad because even if the ‘tulip mania’ in Bitcoin fades, the blockchain technology is here to stay. If it continues to evolve it may provide solutions in various fields, possibly finance and investment. If Robinhood, Reddit and the likes are here to stay, then it is only matter of time before they are wooed by Wall Street and its peers across the world.

While gold cannot match the wild ride that Bitcoin offers its patrons, gold ETFs need to harness the blockchain machinery to its advantage, whether that means diversifying into gold-backed cryptocurrencies or using blockchain technology to democratise flows or other innovations that appeal to millennials.

For now, asset-backed cryptocurrencies haven’t really taken off by comparison to the indeterminate Bitcoin. Is having a quantifiable intrinsic value a disqualification in the crypto universe? If so, then it is good news for gold that remains the king.

Vikram Dhawan

Head Commodities & Fund Manager

Nippon India Mutual Fund

Young tech-savvy investors are driving growth for digital gold

Even though online jewellery portals such as CaratLane, Candere, Flipkart and Amazon have existed for over a decade, the Indian online gold market remains at a nascent stage, accounting for less than 2% of total jewellery sales.34

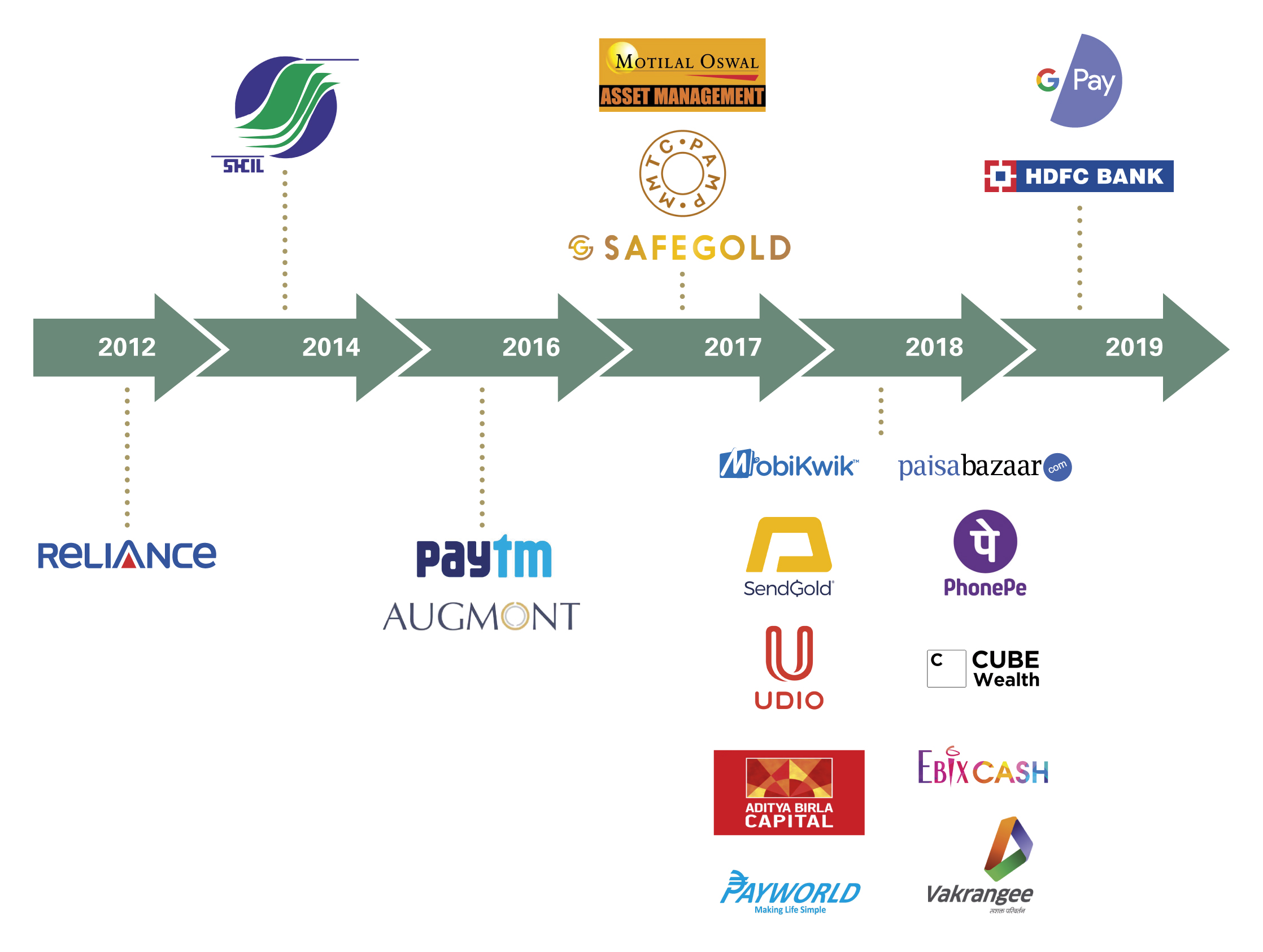

In comparison, the digital gold investment market has picked up quite strongly over the last five years. While the first digital gold product was introduced in 2012 by Reliance, the advent of fintech companies in 2016 has fostered a quicker pace of gold investment in this segment (Figure 1). Today, some 16 companies offer digital gold products with an estimated trading volume in 2022 of around 4-5t compared to less than 0.5t in 2016.35 The growth, albeit trivial in absolute terms, has been driven by young tech-savvy investors, typically between 18 and 35 years of age.36 It is estimated that there are already some 5-6m active digital gold accounts across various platforms.37 Sales tend to peak during Dhanteras (Diwali) and Akshaya Tritiya due to the auspicious nature of these festivals; assets bought during these periods are thought to bring prosperity.

To understand the digital gold category it is essential to study its structure. Of the 16 companies that operate here, three – MMTC-PAMP, Augmont and Safe Gold – provide back-end support and supply gold. The remainder, who are focused on front-end digital platforms, are financial service distributors, stock and commodities brokers and digital wallet companies.

In the coming years Metals Focus expects the market to expand considerably. Key factors that will underpin this growth are increased financial awareness in urban centres and a greater penetration of smartphones.38

Table 2: Certain relevant features of physical gold, gold-backed ETFs, Sovereign Gold Bond and Digital Gold

* Digital gold allows investors to buy physical gold online, have it stored in professional vaults and take possession of it should the need arise. See Internet Investment Gold on gold.org.

Important: The information above has been sourced from publicly available sources as indicated. The above is not a recommendation to invest/disinvest in any product listed above and should not be considered as investment or tax advice. If as a recipient of this document you are in any doubt about products highlighted above, please consult a person authorised under law who specialises in advising on investing in securities. Summaries of laws and regulation set out above are solely to provide the readers with general information and understanding of relevant Indian law. These do not constitute specific legal advice.

Source: Reserve Bank of India, respective ETF gold providers and digital gold providers

COVID’s impact on investment demand

The pandemic had a profound impact on investment behaviour.

In March 2020, the Indian government imposed a strict lockdown, severely restricting the movement of people and business activities and making it extremely challenging to buy physical gold (as well as other precious metals). As a result, many investors switched to financial gold products, including digital gold, ETFs and SGBs, all of which were aggressively marketed by service providers. Rising gold prices also helped promote the financialisation of the metal, attracting young investors towards gold-backed financial products.39

Although these products have existed for some time, the ease of investment – effectively at the click of a button – boosted their popularity during the pandemic. In particular, SGBs can be bought online through a bank's website or an app, with investors receiving a discount of Rs.50/g for online purchases.

According to a report published by VIVO and CMR in December 2020, Indians spent 25% more time on smartphones post-COVID in 2020.40 This development, along with relatively easy access to inexpensive internet services and reasonably priced smartphones, helped higher number of people to access online investment products.

The wider acceptance of these products was evidenced by the surge in inflows. For instance, in 2020 a record 28t inflow was seen in SGBs, with 50% alone occurring in Q3 of that year, the highest since they were first issued by the RBI in 2015. Also in 2020, ETFs witnessed inflows of ~14t, their highest since 2011. And finally, the market for digital gold expanded to 4-5t in 2020 from 2-3t the year before.

Retail investment demand outlook

Retail gold investment demand will continue to face headwinds from the popularity of equities and, in general, the availability of other savings instruments. That said, gold’s price performance amid the COVID crisis reinforced its role as a safe-haven asset for Indian investors, and this further underpins its importance domestically as an investment asset. The proliferation of financial gold products and their greater transparency, together with improved ease of investment, will attract the younger generation towards gold. Steps already taken, including the introduction of bullion banking and the creation of a domestic spot exchange, will go a long way to attracting new gold investors. In particular, these help improve transparency across much of the gold ecosystem and ultimately lead to the introduction of new gold products, including savings, investments, and lending against digital gold holdings. The inclusion of gold in the financial system in India will therefore be vital in helping to maintain and improve gold’s attractiveness as an investment.

Footnotes

Price returns from 31 Dec 2017 – 31 Dec 2022. Source: Bloomberg

SEBI

SEBI

The gold ETF launched by Benchmark is currently owned by Nippon Life India Asset Management Company.

The benchmark for Indian gold ETFs is the domestic price of gold based on landed cost of gold in India.

These eight-year bonds offer an interest of 2.5% per year, which is payable every six months. If investors hold these bonds until the end of the eight-year maturity period, they are exempt from long-term capital gains tax.

Goldhub, Association of Mutual Funds in India (AMFI)

AMFI

RBI data as of 8 February 2023.

Metals Focus

Metals Focus

Metals Focus

Online gold market in India

India: smartphone penetration rate 2040 | Statista

Metals Focus

Economic Times