China’s gold jewellery demand, in tonnage terms, has been weakening in recent years (Chart 1). While the surging gold price and slowing economic growth have been key drivers, structural factors have also had a profound impact on the sector.

When looking at this in value terms, we found that consumers are raising their budgets on gold jewellery, even more so in recent years amid the surging gold price. It is clear that consumers are still willing to buy gold jewellery products, even if they cost more.

The two demand perspectives raise two key questions:

will gold’s tonnage demand continue to decline?

will consumers continue to spend on gold jewellery?

To answer the first question, we cast our eye over gold jewellery’s macro drivers and those industry trends that impact demand. But to address the second question we delved deeper, gaining in-depth insights, particularly from consumers.

To do this we partnered with a global research agency in 2024 to conduct a large-scale consumer research project in major gold markets, including China. The resulting valuable insights from Chinese gold jewellery consumers have helped us to identify key trends and opportunities in the market.

Chart 1: China’s gold jewellery demand has slowed after peaking in 2013*

Chart 1: China’s gold jewellery demand has slowed after peaking in 2013*

Chart 1: China’s gold jewellery demand has slowed after peaking in 2013*

*Gold *Jewellery value based on annual averages of Au9999 in RMB.

Source: Metals Focus, World Gold Council

Sources:

Metals Focus,

World Gold Council; Disclaimer

*Jewellery value based on annual averages of Au9999 in RMB.

Cyclical and structural factors behind China’s gold jewellery demand trends

China’s gold jewellery demand has experienced a roller-coaster ride in past decades (Chart 1). Demand surged by 362% between 2001 – when the unified purchase and distribution model was suspended – and 2013 – when demand peaked amid the bargain-hunting buying frenzy. During this period, factors such as market liberalisation, growing consumer wealth, and urbanisation fuelled growth.

But consumption, in terms of quantity, entered a sustained decline after 2013, and by 2024 had fell 49%, despite periodic rebounds. This downward trend was driven by multiple factors: slowing economic growth, younger consumers’ weakening attachment to gold, and a higher gold price, especially after 2022. And we believe such weakness is driven by both cyclical forces and structural factors.

Cyclical forces in play

The changes in China’s gold jewellery demand, as in other consumer goods, exhibit cyclical trends (Chart 2). Our modelling analysis reveals that economic growth and interest rate levels are key in determining gold jewellery consumption in the country. Such macroeconomic drivers are inherently cyclical in nature; and gold jewellery consumption also reflects observable cyclical patterns.

As illustrated below, China’s gold jewellery demand closely tracks the 3 ~ 4-year inventory cycle (commonly referred to as the Kitchin cycle).1

Currently, the economy appears to be in a protracted transition between passive destocking – the early phase of recovery based on the Kitchin cycle – and active restocking, where the economy booms. We have been stuck in this transitioning period, which began in H2 2023, longer than has been seen in previous cycles. This is mainly due to a weak consumer spending appetite after the COVID-19 pandemic, the property sector downturn, and external pressures, such as the ongoing US trade tensions.

Chart 2: China’s gold jewellery demand exhibits some cyclical signs

Quarterly y/y changes in finished industrial goods inventory and gold jewellery demand*

Chart 2: China’s gold jewellery demand exhibits some cyclical signs

Chart 2: China’s gold jewellery demand exhibits some cyclical signs

Quarterly y/y changes in finished industrial goods inventory and gold jewellery demand*

*Both data to Q1 2025.

Source: National Bureau of Statistics, Metals Focus, World Gold Council

Sources:

National Bureau of Statistics,

Metals Focus,

World Gold Council; Disclaimer

*Both data to Q1 2025.

M1 money supply trends, a leading indicator of finished goods inventory, further suggests this limbo period may persist (Chart 3).

Chart 3: M1 trends imply that the current passive destocking phase may persist for a while

Monthly y/y changes in industrial finished goods inventories and M1 money supply*

Chart 3: M1 trends imply that the current passive destocking phase may persist for a while

Chart 3: M1 trends imply that the current passive destocking phase may persist for a while

Monthly y/y changes in industrial finished goods inventories and M1 money supply*

Chart 3: M1 trends imply that the current passive destocking phase may persist for a while

Monthly y/y changes in industrial finished goods inventories and M1 money supply*

*M1 data to June 2025. Inventory data to May 2025.

Source: National Bureau of Statistics, World Gold Council

Sources:

National Bureau of Statistics,

World Gold Council; Disclaimer

*M1 data to June 2025. Inventory data to May 2025.

Structural factors matter too

Structural factors have played a pivotal role in shaping China's gold jewellery demand over the past two decades. A prime example is the 2001 liberalisation of China's gold market, which served as a transformative structural change that dramatically boosted gold jewellery consumption.

China's shifting demographics have also impacted long-term gold jewellery demand relating to newborn gifting and wedding purchases (Chart 4). With both birth rates and the number of marriages declining, gold jewellery demand in recent years has come under pressure.

Chart 4: Both marriages and new births witnessed sustained and notable declines after 2013*

Chart 4: Both marriages and new births witnessed sustained and notable declines after 2013*

Chart 4: Both marriages and new births witnessed sustained and notable declines after 2013*

*Annual data to 2024.

Source: National Bureau of Statistics, World Gold Council

Sources:

National Bureau of Statistics,

World Gold Council; Disclaimer

*Annual data to 2024.

From a cyclical perspective, the gold jewellery industry may face a prolonged period of tepid demand, in tonnage terms. Structural factors, including a reduction in the number of births and marriages, also indicate longer-term consolidation. Other factors, such as the reducing number of jewellers’ points of sales, which was a result of declining demand, may reinforce the weakness.

Rising spending on gold jewellery: a consumer perspective

In contrast to tonnage demand, which paints a gloomy picture, gold jewellery consumption in value terms is generally rising. Our latest data shows that Chinese consumers spent RMB84bn on gold jewellery in Q1 2025, 29% higher q/q. While this is lower than the very high base of Q1 2024, it was the third highest quarter on record. This paints a very different picture from the tonnage demand change, suggesting that Chinese consumers remain willing to buy gold jewellery, despite costs never seen before.

Why are consumers spending more on gold jewellery? The above analysis of tonnage demand weakness mainly views gold jewellery as a consumer good, neglecting its financial value. While some consumers buy gold jewellery for its aesthetic quality and for daily wear, many also regard it as a value-preserving investment – one that has yielded attractive returns over recent years.

Meanwhile, as the industry constantly innovates, new product designs are attracting younger consumers, responding to their emotional needs. And cultural elements continue to be a key driver of consumers’ gold jewellery purchase decisions.

But we wanted a deeper understanding. Why do consumers buy gold jewellery and why don’t they? How can communications with consumers be enhanced to unlock opportunities…if there are any?

To answer these questions and gather clues to potential opportunities, our large-scale global consumer research project was carried out in H2 2024. The project questioned over 3,000 female consumers, of various ages, from different tiers of Chinese cities, to ensure a comprehensive picture of jewellery consumer insights. For more on the methodology, see the Appendix

Key consumer insights

Gold jewellery ownership is high among Chinese consumers

Gold jewellery ownership in China reflects both entrenched cultural habits and emerging generational shifts. Our research reveals three related themes:

Widespread adoption

81% of our sample currently owns fine gold jewellery (Chart 5). This is in line with results from our annual gold jewellery retailer research, which show that gold enjoys an increasing market share relative to other products. When we conducted a similar consumer gold jewellery research project in 2019, ownership of fine gold jewellery was only 62%. While these two results are not directly comparable due to differences in sampling and methodology, they nevertheless reflect certain trends.

Chart 5: Gold jewellery ownership in China is high

Q: Which, if any, of the items below do you currently personally own?*

Chart 5: Gold jewellery ownership in China is high

Chart 5: Gold jewellery ownership in China is high

Q: Which, if any, of the items below do you currently personally own?*

*Base: All respondents (n=3,025).

Source: World Gold Council

Similarly, our research revealed that fine gold jewellery remains top of the list of products consumers have ever purchased or recently purchased.2

Young consumer ownership is also high

Although we found that gold jewellery ownership increases with age, 62% of consumers between 18 and 24 own gold jewellery, higher than other types of jewellery (Chart 6). This represents a significant increase compared to 2019 when, in a similar survey, 37% of this group owned gold jewellery.

The past five years have seen a rapidly expanding product range, more creative designs, and the rising popularity of “Guochao” – which reflects the interest of young consumers in products that embed traditional Chinese culture. These factors have helped to drive young consumers to gold jewellery; a finding we have discussed in our previous reports.3

Chart 6: Over 60% of young consumers own gold

Q: Which, if any, of the items below do you currently personally own?*

Chart 6: Over 60% of young consumers own gold

Chart 6: Over 60% of young consumers own gold

Q: Which, if any, of the items below do you currently personally own?*

*Base: All respondents (n=3,025).

Source: World Gold Council

Most consumers buy gold jewellery for themselves. Our research showed that 79% of consumers buy gold jewellery for themselves while 41% purchase for someone else (Chart 7). This echoes our retailer survey, which revealed that self-indulgent purchases dominate gold jewellery consumption.

Chart 7: Most consumers buy gold jewellery for themselves

Q: Which, if any, of these items have you ever personally purchased?*

Chart 7: Most consumers buy gold jewellery for themselves

Chart 7: Most consumers buy gold jewellery for themselves

Q: Which, if any, of these items have you ever personally purchased?*

*Base: All respondents (n=3,025).

Source: World Gold Council

We also explored consumer attitudes towards gold jewellery and purchasing moments:

Consumers view gold as a cultural and timeless investment, associated with good luck

Survey results show consumer attitudes towards gold jewellery haven’t changed that much. Whether or not they buy gold jewellery, consumers still treasure its rich, timeless traditional cultural value (Chart 8). This also helps explain the rising the popularity of Heritage gold products in recent years, albeit that weights are lowering to make them more affordable amid the gold price surge.

Consumers view gold jewellery as a store of value too. This resonates with the surging willingness of households to save in an uncertain world, and further supports gold jewellery buying.

Chart 8: Consumers see gold jewellery as a traditional and timeless investment

Q: Now thinking specifically about gold jewellery, how much do you agree or disagree with each of these?*

Chart 8: Consumers see gold jewellery as a traditional and timeless investment

Chart 8: Consumers see gold jewellery as a traditional and timeless investment

Q: Now thinking specifically about gold jewellery, how much do you agree or disagree with each of these?*

*Base: All who ever purchased fine gold jewellery for themselves / for someone else (n=2,456). All who purchased fine gold jewellery in the past 12 months (P12M) for themselves / for someone else (n=2,019). All who never purchased fine gold jewellery for themselves / for someone else (n=569). One answer per statement

Source: World Gold Council

*Base: All who ever purchased fine gold jewellery for themselves / for someone else (n=2,456). All who purchased fine gold jewellery in the past 12 months (P12M) for themselves / for someone else (n=2,019). All who never purchased fine gold jewellery for themselves / for someone else (n=569). One answer per statement.

Consumers demand joy and high quality in their gold jewellery purchases

In general, we found that consumers are looking for products – whether fashion and lifestyle goods in general or gold jewellery – that bring them joy and confidence (Chart 9). And self-rewarding is equally important, similar to the findings from our retailer survey as mentioned above.

But results also show that gold jewellery does not stand out as the best product to deliver any of these emotional needs, implying a clear lack of positioning compared to other jewellery products.

Chart 9: Top purchase needs of women relate to joy and confidence, and gold buyer needs are the same

Q: Which of these do you typically look for from these types of fashion/lifestyle items?*

Chart 9: Top purchase needs of women relate to joy and confidence, and gold buyer needs are the same

Chart 9: Top purchase needs of women relate to joy and confidence, and gold buyer needs are the same

Q: Which of these do you typically look for from these types of fashion/lifestyle items?

*Base: All respondents (n=3,025). Multiple choices up to 5 options.

Source: World Gold Council

*Base: All respondents (n=3,025). Multiple choices up to 5 options.

Meanwhile, products must be of high quality and display superior craftsmanship, with a range of styles that allow women to make personalised choices aligned to their own individuality and aspiration (Chart 10). And results show that consumers’ top functional needs for purchases in general and for gold jewellery products are quite similar.

It is worth mentioning that compared to other jewellery and lifestyle products, gold jewellery stands out as being a timeless item that holds its value. But it loses out to fashion items in “high quality” and “fits my style” – the two most important functional needs.

Chart 10: Overall, women look for quality and well-crafted goods that fit their style

Q: What specific characteristics do you typically want from these types of fashion/lifestyle items?*

Chart 10: Overall, women look for quality and well-crafted goods that fit their style

Chart 10: Overall, women look for quality and well-crafted goods that fit their style

Q: What specific characteristics do you typically want from these types of fashion/lifestyle items?*

*Base: All respondents (n=3,025). Multiple choices up to 5 options.

Source: World Gold Council

*Base: All respondents (n=3,025). Multiple choices up to 5 options.

Identifying key gold jewellery purchasing moments

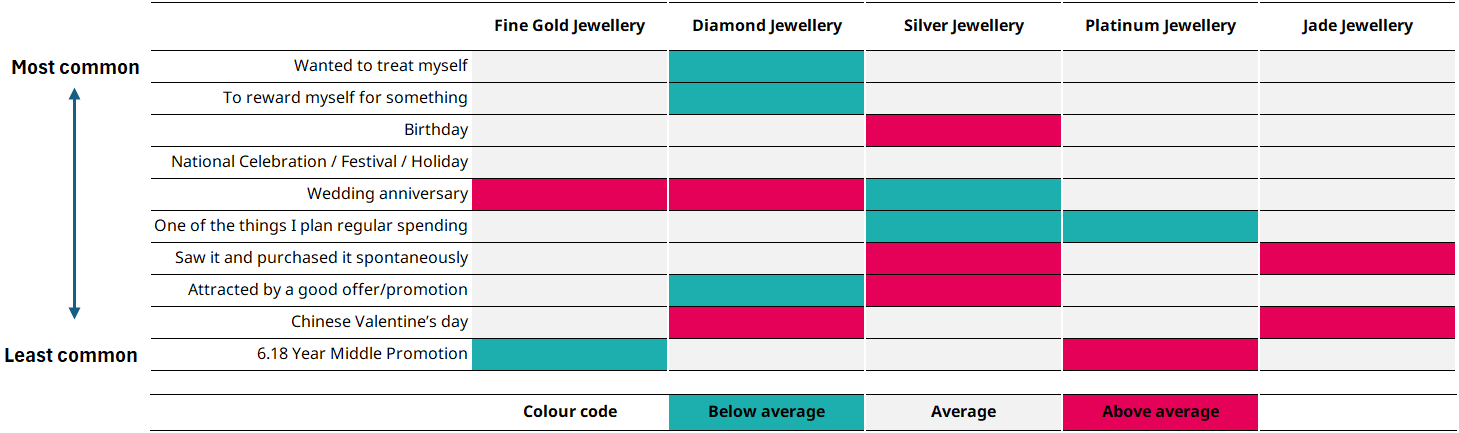

We examined gold’s purchasing moments from two perspectives: purchases for oneself (Figure 1) and those for someone else (Figure 2). A common theme is that wedding-related occasions remain key gold jewellery buying moments. And gold jewellery gifting outperforms during certain other special occasions.

Figure 1: Gold jewellery purchases for oneself stands out during wedding anniversaries

Q: Which, if any, of these prompted you to purchase the following items for yourself in the past 12 months?*

*Base: All who purchased at least one product for themselves in the P12M (n=2,991): fine gold jewellery (n=1,881), diamond jewellery (n=513), silver jewellery (n=564), platinum jewellery (n=466), jade jewellery (n=413). Source: World Gold Council

Figure 2: Gold jewellery gifting outperforms for weddings, Mother’s Day and special occasions

Q: And for which occasions, if any, did you purchase each of the following items as a gift for someone in the past 12 months?*

Base: All who purchased at least one product as a gift for someone else in the P12M: Fine gold jewellery (n=862), Diamond jewellery (n=279), Silver jewellery (n=517), Platinum jewellery (n=302), Jade jewellery (n=314). Source: World Gold Council

But gold loses out to other jewellery types at various other moments. For instance, during Chinese Valentine’s Day consumers would rather buy diamond items for themselves or others. And on Mother’s Day, gold competes with jade, while on wedding anniversaries it once again competes with diamonds.

While the surging gold price in recent years may have become a deterrent for consumers during these occasions, there are other factors behind gold’s relative muteness during these purchasing moments – perhaps the lack of promotional efforts or a weaker emotional connection with romance.

The purchase journey

Who buys gold jewellery?

Our survey results indicate that gold jewellery purchasers more likely to be middle-aged and married, from households with high incomes, and living in Tier 2 or Tier 3 cities. These consumers purchase jewellery products for themselves three times a year on average.

Consumers have become more savvy

It was also apparent in our survey results that consumers tend to do their homework before any fashion or lifestyle purchase – including gold jewellery. This is consistent with trends we have observed over recent years. As the gold price has rocketed to unprecedented levels and the product range has broadened significantly, consumers, especially younger ones, are increasing their efforts to understand the gold price level, the product designs on offer, and the labour charges on the piece they want to buy.

Most consumers source information for their jewellery purchases from in-store interactions (61%) and online forums or social media (58%). We have previously noted that retailers are focusing their marketing efforts towards private traffic, social media and in-store interactions. And their efforts have made an impact in how consumers look for information. Social media apps, such as Douyin and Little Red Book, are clearly influencing their users’ purchase decisions, and the rising time consumers spend on these platforms place them in a prominent position when jewellers are considering where to focus their marketing efforts.

It is probably not surprising to see that in store remains the dominant location for gold jewellery purchases (81%) – higher than the average level for all jewellery (78%). The need to “feel and touch” has always been part of jewellery buying, particularly gold products amid their monetary/investment value.

Nonetheless, we have witnessed an increasing effort from jewellery retailers to promote their products via online channels and this has yielded great results. Major jewellers have reported continued growth in online sales, both in value and units.4 And growth in units clearly outpaces that in value – highlighting the fact that sales via online platforms concentrate on products with low per-unit prices.

Figure 3: Gold jewellery consideration is high among previous buyers*

Q6. Which, if any, of these items would you consider personally purchasing in the next 12 months? Please select all that apply. Q7. And which, if any, of these items would you never consider purchasing? Please select all that apply.

*Base: All respondents (n=3025), Ever purchased gold jewellery (n=2456), Never purchased gold jewellery (n=569). Please also note that these are multiple choices questions so all the percentage for Q6 & 7 do not add up to 100%.. Source: World Gold Council

Looking ahead, opportunities remain

There is room for growth

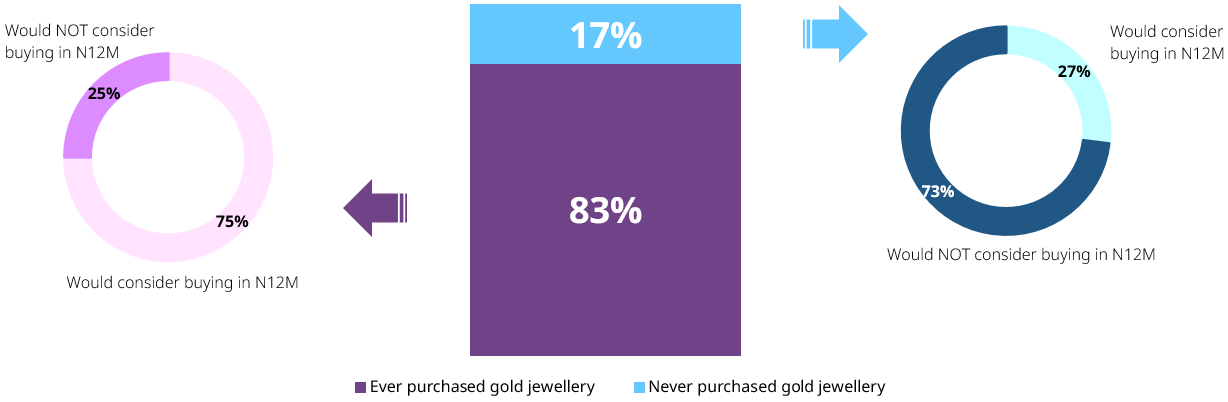

Market saturation is a growing concern for retailers. It is true that over 80% of consumers own gold jewellery and ownership among young consumers has also increased significantly. But it is also true that 67% of our total sample – whether or not they have ever bought gold jewellery before – would consider buying it in the next 12 months (from the date of the field research). And the majority would purchase for themselves. To be more specific (Figure 3):

75% of consumers who have ever purchased gold jewellery would consider purchasing again in the next 12 months

27% of consumers who have never purchased gold jewellery before would consider a purchase in the next 12 months.

Overcoming barriers

Although a clear majority of consumers would consider buying gold jewellery in the near future, it is vital to identify the barriers preventing those who say they would not buy (Chart 11). One of these is affordability. The gold price has soared in recent years, outpacing income growth, and it is obvious that, for some, this is a deterrent to gold jewellery purchase.

Aside from affordability, we observed two other important barriers to gold jewellery purchases:

Lack of occasion/motives to buy

Designs that don’t match consumer desires.

Chart 11: Other than price, lack of occasions and design are key barriers

Q: You mentioned that you have not purchased gold jewellery in the past 12 months. What, if anything, stopped you from buying gold jewellery?*

Chart 11: Other than price, lack of occasions and design are key barriers

Chart 11: Other than price, lack of occasions and design are key barriers

Q: You mentioned that you have not purchased gold jewellery in the past 12 months. What, if anything, stopped you from buying gold jewellery?*

*Base: All who did not purchase fine gold jewellery in P12M (n=1,006).It is a multiple-choice question.

Source: World Gold Council

*Base: All who did not purchase fine gold jewellery in P12M (n=1,006).It is a multiple-choice question.

We believe that design issues are being addressed by jewellery manufacturers. Over the years, various innovations have emerged, ranging from Heritage gold products that highlight the traditional Chinese culture, to Hard Pure Gold products focusing on fashionable designs and affordable prices. And by incorporation of different materials, such as enamel, gems and feathers, we anticipate gold jewellery retail stores will shine colourfully, broadening consumer gold jewellery choice.

Where opportunities lie

First, it is important to strengthen the emotional link between gold jewellery and various occasions. As shown above, gold jewellery products, whether purchased for oneself or others, lose out to other jewellery types on a number of occasions.

We believe that greater engagement is required with participants across the gold jewellery value chain. This will serve to highlight gold jewellery’s suitability for different occasions. Effective messages – broadcast through targeted marketing, occasion-based online navigation and the retail environment – will strengthen the consumer’s emotional link between gold jewellery and special occasions.

Second, it is crucial to position gold jewellery as a quality product. When we asked about confidence factors that support gold jewellery purchase decisions, “quality”, “trust” and “guarantee” were among those most commonly selected by respondents (Chart 12).

Chart 12: Consumers demand quality and assurance

Q29. When purchasing the following types of jewellery, what, if anything, gives you the confidence to make the purchase? Please select all that apply.*

Chart 12: Consumers demand quality and assurance

Chart 12: Consumers demand quality and assurance

Q29. When purchasing the following types of jewellery, what, if anything, gives you the confidence to make the purchase? Please select all that apply.*

*Base: All who purchased jewellery in the P12M: All Jewellery (n=2630), Fine gold jewellery (n=2019),

Source: World Gold Council

*Base: All who purchased jewellery in the P12M: All Jewellery (n=2630), Fine gold jewellery (n=2019),

High quality is the top functional need for women in China when purchasing fashion and lifestyle items. While gold jewellery performs well in this regard, it does not stand out, highlighting the need for reinforcement of this characteristic.

When purchasing jewellery, consumers want sellers to be able to prove the quality, and for gold jewellery in particular, they value the presence of a guarantee or warranty.

It is therefore key to ensure sellers support quality perceptions of gold jewellery by providing relevant reassurance (such as a guarantee).

Clear information about products – in other words, transparency – along with guidance via information gathering channels, will help consumers in their purchase decisions. And although gold ownership among young consumers has risen sharply over recent years, it will be necessary to reinforce the value of gold jewellery if it is to remain relevant to future generations. This can be achieved through:

A continuation of design innovation to ensure products fit consumers’ emotional and functional needs

By preserving and highlighting Chinese culture through products such as Heritage gold, whereby traditional elements are combined with modern design.

A closer look at opportunities by segment

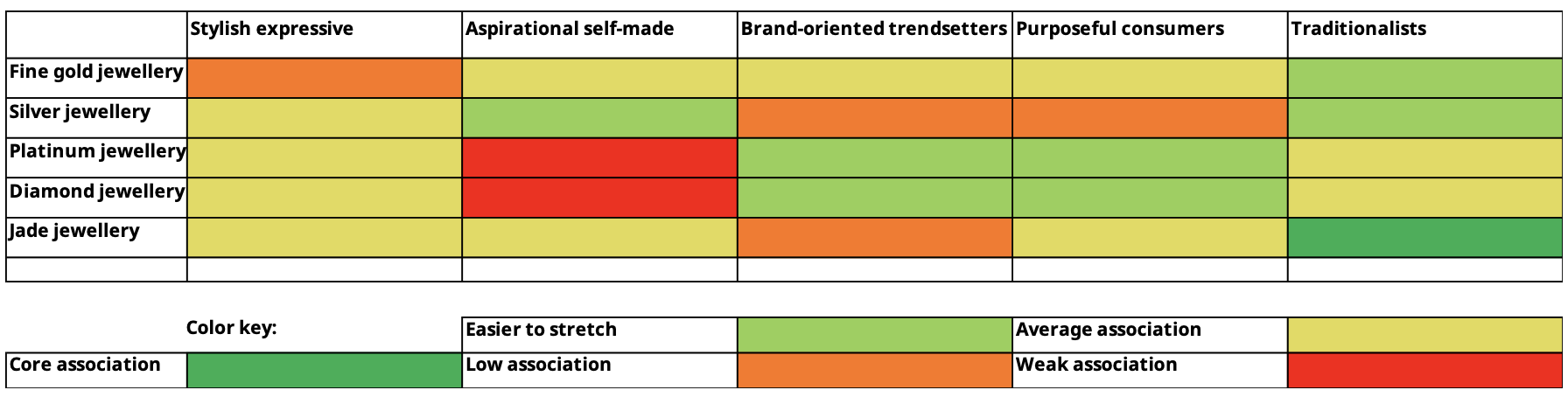

In this consumer research we identified five different consumer segments (Table 1). And we have focused on three: ‘Brand-oriented Trendsetters’; ‘Purposeful Consumers’; and ’Traditionalists’. We examined how well fine gold jewellery matched their needs, and looked at other factors such as the potential for further gold jewellery purchases. And we believe there is untapped potential in these three groups.

Brand-Oriented Trendsetters

We believe it is key to provide enough information and evidence to demonstrate that gold is trendy via reputable/well known brands and retailers. Based on their emotional and functional needs, which are mainly associated with purchasing on-trend products from widely-known brands, jewellers could attract this segment by:

Offering modern and trendy products that capture attention

Capitalising on their high jewellery purchase frequency by in-store promotion – their main gold jewellery purchase location

Leveraging online channels to attract consumers who are likely to source information via online forums and purchase gold jewellery online

Reinforcing brand credentials and recognition as a globally known or a quality local brand.

Purposeful Consumers

Purposeful Consumers are high-frequency jewellery buyers, who are environmentally-conscious and see their purchases as an investment. Jewellers could offer exclusive and modern products that would increase the likelihood of repeat buying. It is important to emphasise gold jewellery’s key differences to this group, educating them about its attributes as a trendy accessory as well as a long-term investment asset that holds its value. Financial advisors may be able to help reinforce the latter, as they are a key jewellery information source, more so than other segments. And because this group is typically environmentally aware, it is also vital to provide them with information such as the origin of the gold used in the piece and a third-party appraisal.

Traditionalists

Traditionalists are loyal gold jewellery buyers and likely offer immediate opportunity. They will likely respond well to communications that highlight gold’s rich traditional value, as this meets their emotional need to stay close to their roots and traditions. Fine pieces with superior craftsmanship and a guarantee of quality will appeal to these consumers as they value these aspects in their choice of fashion and lifestyle products. In-store support and promotion are paramount as Traditionalists tend to be more dependent on one-to-one interactions and have a higher tendency to purchase offline than our other segments.

Table 1: Segmenting consumers

Stylish expressive

Aspirational self-made

Brand-oriented trendsetters

Purposeful consumers

Traditionalists

Segment size (% of total)

21%

16%

20%

15%

27%

Fine gold jewellery ownership

79%

82%

77%

75%

86%

Likelihood to buy fine gold jewellery in N12M

86%

81%

89%

91%

84%

Purchase frequency (times) of any jewellery in P12M

2.6

2.8

3

2.9

2.5

*Base: Stylish Expressive (n=646), Aspirational Self-Made (n=474), Brand Oriented Stylish Expressive (n=623), Purposeful Consumers (n=453), Traditionalists (n=829). For fit analysis results, see Appendix. Source: World Gold Council

Conclusion

It is likely that the current weakness in gold jewellery demand, in tonnage terms, will persist in the near-mid term amid macro cyclical forces and structural pressure.

But from the consumer perspective, we found that ownership of fine gold jewellery has risen notably, especially among the young. And gold jewellery’s relevance at key buying moments is relatively weaker than other types of jewellery

But there is still potential as shown in Figure 3, which can be unlocked if the industry can strengthen and cater to consumers’ functional and emotional needs highlighted in Chart 9 andChart 10.

Meanwhile, clear and relevant communication with consumers through the channels they frequently use, will allow the industry to encourage and sustain their interest in gold jewellery. Against a backdrop where uncertainties abound and value-preservation is top of mind, consumers’ total spending on gold jewellery may stay elevated. After all, despite recent increases, the gold price relative to Chinese household income or spending remains healthy (Chart 13) – just in line with the long-term average – also implying further potential.

Chart 13: From an income perspective, there is still room for growth in gold jewellery spend*

Chart 13: From an income perspective, there is still room for growth in gold jewellery spend*

Chart 13: From an income perspective, there is still room for growth in gold jewellery spend*

*Based on the quarterly average Au9999 price in RMB, household disposable income and spending data between 2002 and 2024.

Source: National Bureau of Statistics, World Gold Council

Sources:

National Bureau of Statistics,

World Gold Council; Disclaimer

*Based on the quarterly average Au9999 price in RMB, household disposable income and spending data between 2002 and 2024.

Appendix

The Chinese gold jewellery consumer insights report is based on research conducted by a global research agency on behalf of the World Gold Council. Fieldwork for primary data collection across all markets took place from 10 June to 14 October 2024.

The subject of the survey is the claimed jewellery purchase and gifting behaviours, occasions, needs and attitudes among women. Specifically, the research focused on uncovering:

Which categories of products women purchased, were gifted or requested as gifts over different timeframes, with more granular focus on jewellery types, including gold jewellery

What were the key needs and motivations, preferences and attitudes that surrounded jewellery purchases and gifting, and how did gold compare to other types of jewellery in this context.

What were the key drivers or barriers to gold jewellery purchase and gifting.

Sample

This research was conducted in China using mixed-method data collection. The following samples were achieved: 2,640 interviews were collected via online self-completion surveys (CAWI), and 385 were collected via in-person interviewer-assisted interviewing (CAPI). The data collection methodology design is reflective of the desire to reach a broad and diverse sample of women from 1 ~ 4 tiered Chinese cities.

Quotas and data weighting

Quotas were applied across age, region, working status, and Tier in China.

Online sample quotas were set using census data to nationally representative proportions of women across age and region, as well as on working status for China.

The offline sample quotas were designed with specific geographical, socio-economic and demographic coverage in mind. Only Chinese cities in Tier 1-4 (as of 2024 rating) and women aged 55-65 were covered.

Data weighting has been applied to combine and correctly represent online and offline samples across the key variables of age and region as well as working status and Tier.

Specific definitions and references in the report:

Gold jewellery owners are those who claim to currently own fine gold jewellery that is not gold plated and which excludes diamonds.

Gold jewellery buyers are those who claim to have bought fine gold jewellery that is not gold plated and which excludes diamonds.

Jewellery buyers are those who claim to have bought at least one type of jewellery.

Attitude statements: responses are recorded using a 5-point scale, and references to “agree” / “net agree”, “disagree” / “net disagree” refer to the netted answers of the top two codes (e.g. “strongly agree” and “somewhat agree”) or to the netted answers of the bottom two codes (e.g. “strongly disagree” and “somewhat disagree”).

At purchase category, purchase occasion and some other questions, respondents were asked to select from a pre-coded list (with the option of giving an “other specify” response). Data for these questions is subject to these pre-coded lists and the answers chosen by respondents.

Differences indicated in the data between the groups of interest are based on two-tailed significance tests with a 95% level of confidence.

Indexing calculation was applied to some of the data in the report. Differences over an index of 120 or under an index of 80 are highlighted, derived via direct comparison of a specific data point to the average of all responses in that group.

Fit analysis

The Fit analysis (Figure 4) shows how well a product meets the needs of a segment. It is a statistical procedure using correlations of product associations with the needs of segments (based on Asspatts).

Figure 4: The segmentation Fit analysis*

*Base: based on products vs needs rating from Q20 (Emotional): Thinking about the items you have purchased for yourself / received as a gift in the past 12 months, or would consider buying for yourself / requesting as a gift in the next 12 months, which, if any, of the statements below best fits with each? And Q21 (Functional): Again, thinking about the items you have purchased for yourself / received as a gift in the past 12 months, or would consider buying for yourself / requesting as a gift in the next 12 months, which, if any, of the characteristics below best fits with each? Source: World Gold Councill

Asspatts – these are double normalised scores created from associations. They are created based on needs (Emotional and Functional) as well as from the associations of how products deliver against these needs. Asspatts are calculated for needs within each segment and for each product at an overall level.

Fit score – this is a summary metric derived from the correlation of the Asspatts for segments and products. It shows how well each product performs against the needs of each segment. It is classified into different bands through grouping correlation scores by percentiles. We show a fit score that is a weighted average of the fit of Emotional and Functional needs.

2Base: All respondents (n=3,025). Q2. Which, if any, of these items have you ever personally purchased? Please select all that apply. Q3. And which have you personally purchased in the past 12 months? Please select all that apply. Questions were asked between August and September 2024.

32021 Chinese gold jewellery market insights: mainstream, younger and more transparent | World Gold Council, September 2021. 2023 Chinese jewellery market insights: Gold continues to lead the market | World Gold Council, October 2023.

Diversification does not guarantee any investment returns and does not eliminate the risk of loss. Past performance is not necessarily indicative of future results. The resulting performance of any investment outcomes that can be generated through allocation to gold are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. The World Gold Council and its affiliates do not guarantee or warranty any calculations and models used in any hypothetical portfolios or any outcomes resulting from any such use. Investors should discuss their individual circumstances with their appropriate investment professionals before making any decision regarding any Services or investments. This information may contain forward-looking statements, such as statements which use the words “believes”, “expects”, “may”, or “suggests”, or similar terminology, which are based on current expectations and are subject to change. Forward-looking statements involve a number of risks and uncertainties. There can be no assurance that any forward-looking statements will be achieved. World Gold Council and its affiliates assume no responsibility for updating any forward-looking statements.

Information regarding QaurumSM and the Gold Valuation Framework

Note that the resulting performance of various investment outcomes that can be generated through use of Qaurum, the Gold Valuation Framework and other information are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. Neither World Gold Council (including its affiliates) nor Oxford Economics provides any warranty or guarantee regarding the functionality of the tool, including without limitation any projections, estimates or calculations.