Portfolio resiliency: Gold’s role amid economic crosscurrents

22 October, 2025

Tariffs, fiscal concerns… and gold to the rescue

Since the publication of our Why gold in 2025? A cross-asset perspective report earlier this year, much has happened on the policy front and in the broader economy. Uncertainties and vulnerabilities remain across geopolitical, fiscal, and trade domains. Investors are particularly concerned about growth and inflation, creating a challenging situation for policymakers as the dual policy goals of the Federal Reserve are in direct conflict. With persistent fears of stagflation, gold has once again stepped into the spotlight, rising more than 50% this year.1 Importantly, the core reasons for considering alternative assets such as gold, as outlined in our May report, remain largely unchanged.

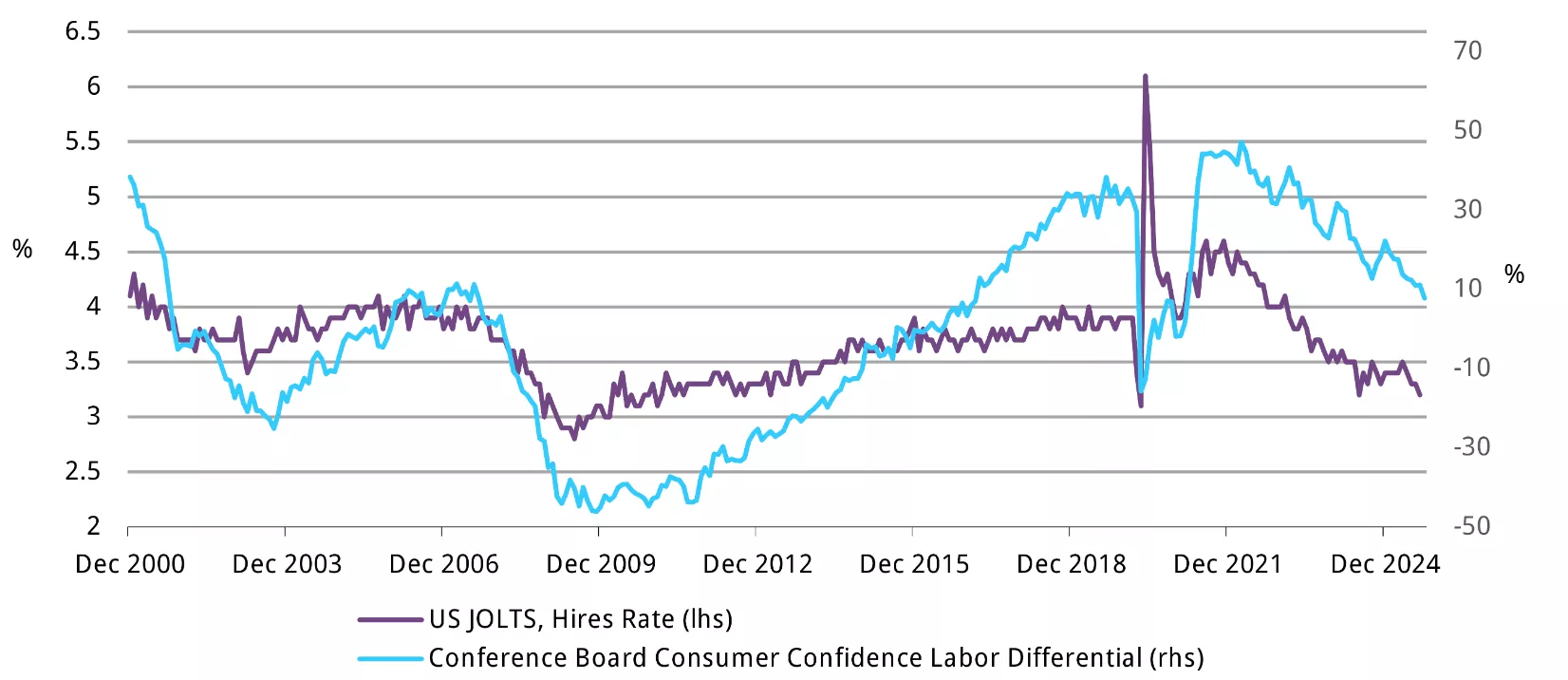

First, equities appear complacent. US equities have posted remarkable gains in recent months, reigniting concerns about valuation excess and concentration risk. Indeed, investors face a market that feels euphoric on the surface but remains fragile underneath. Should economic pressures mount (Chart 1), investors may increasingly seek refuge in safe-haven assets, with gold standing out as a historically resilient option, as outlined in our mid-year outlook.

Chart 1: The “slow hire” risks turning into a “no hire” narrative

US JOLTS, Hires Rate and Conference Board Consumer Confidence Labor Differential*

Source: Bloomberg, Bureau of Labor Statistics, World Gold Council

Second, bond markets remain uncertain. The Fed officially resumed its easing cycle in September, cutting the federal funds rate by 25 basis points in response to a cooling labour market (Chart 1) – an action widely anticipated by markets. However, US long-term yields could face renewed upward pressure if tariffs and reshoring efforts drive domestic costs higher, complicating the Fed’s inflation target. At the same time, long-term treasuries remain exposed to concerns over the Federal Reserve’s independence and the US government’s sizeable fiscal funding needs.

Against this backdrop, gold’s appeal as a hedge against both equity and bond market instability is growing – though risks exist. As we discussed in our recent blog, gold’s rapid ascent could prompt rebalancing and profit taking. For example, from a technical standpoint, the monthly Relative Strength Index (RSI) is above 90 and gold is sitting more than 20% above its 200-day moving average. These factors could lead to short-term reversals. In addition, the sharp increase in the gold price could dampen consumer demand while global trade normalisation and a pick-up in GDP growth could revive risk appetite further.

In summary, maintaining a diversified approach and remaining vigilant to shifting market dynamics is essential. Amidst a growing investor base, secular US dollar weakness and continued geoeconomic uncertainty, gold’s enduring resilience and diversification benefits remain as relevant as ever.

Footnotes:

1As of 10 October 2025. Our Gold Return Attribution Model (GRAM) points to a combination of a weaker US dollar and a highly uncertain geopolitical environment as the reasons for the strong investment demand.

Disclaimer

Important information and disclaimers

© 2025 World Gold Council. All rights reserved. World Gold Council and the Circle device are trademarks of the World Gold Council or its affiliates.

All references to LBMA Gold Price are used with the permission of ICE Benchmark Administration Limited and have been provided for informational purposes only. ICE Benchmark Administration Limited accepts no liability or responsibility for the accuracy of the prices or the underlying product to which the prices may be referenced. Other content is the intellectual property of the respective third party and all rights are reserved to them.

Reproduction or redistribution of any of this information is expressly prohibited without the prior written consent of World Gold Council or the appropriate copyright owners, except as specifically provided below. Information and statistics are copyright © and/or other intellectual property of the World Gold Council or its affiliates or third-party providers identified herein. All rights of the respective owners are reserved.

The use of the statistics in this information is permitted for the purposes of review and commentary (including media commentary) in line with fair industry practice, subject to the following two pre-conditions: (i) only limited extracts of data or analysis be used; and (ii) any and all use of these statistics is accompanied by a citation to World Gold Council and, where appropriate, to Metals Focus or other identified copyright owners as their source. World Gold Council is affiliated with Metals Focus.

The World Gold Council and its affiliates do not guarantee the accuracy or completeness of any information nor accept responsibility for any losses or damages arising directly or indirectly from the use of this information.

This information is for educational purposes only and by receiving this information, you agree with its intended purpose. Nothing contained herein is intended to constitute a recommendation, investment advice, or offer for the purchase or sale of gold, any gold-related products or services or any other products, services, securities or financial instruments (collectively, “Services”). This information does not take into account any investment objectives, financial situation or particular needs of any particular person.

Diversification does not guarantee any investment returns and does not eliminate the risk of loss. Past performance is not necessarily indicative of future results. The resulting performance of any investment outcomes that can be generated through allocation to gold are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. The World Gold Council and its affiliates do not guarantee or warranty any calculations and models used in any hypothetical portfolios or any outcomes resulting from any such use. Investors should discuss their individual circumstances with their appropriate investment professionals before making any decision regarding any Services or investments.

This information may contain forward-looking statements, such as statements which use the words “believes”, “expects”, “may”, or “suggests”, or similar terminology, which are based on current expectations and are subject to change. Forward-looking statements involve a number of risks and uncertainties. There can be no assurance that any forward-looking statements will be achieved. World Gold Council and its affiliates assume no responsibility for updating any forward-looking statements.

Information regarding QaurumSM and the Gold Valuation Framework

Note that the resulting performance of various investment outcomes that can be generated through use of Qaurum, the Gold Valuation Framework and other information are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. Neither World Gold Council (including its affiliates) nor Oxford Economics provides any warranty or guarantee regarding the functionality of the tool, including without limitation any projections, estimates or calculations.