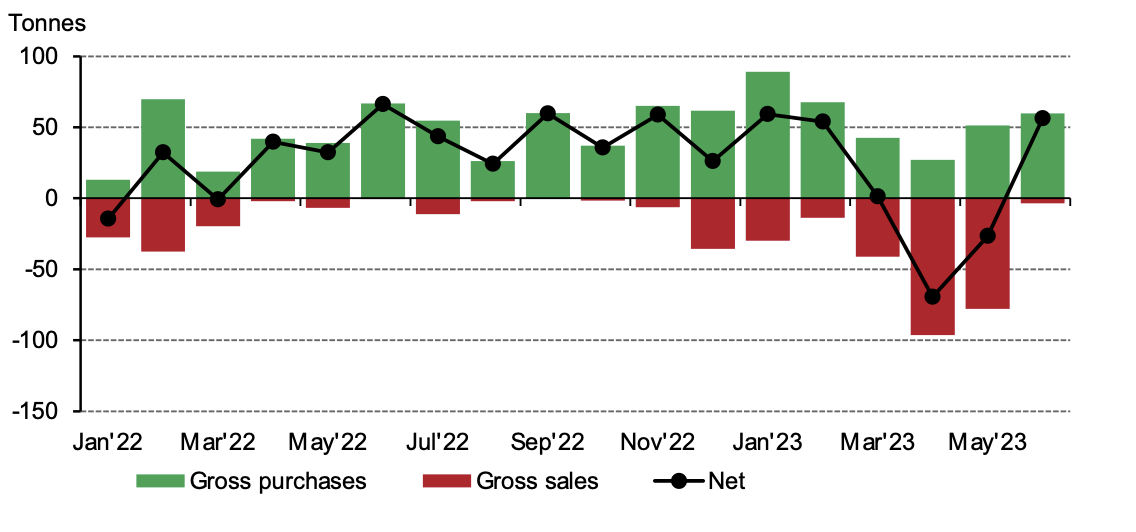

- Central banks bought a net 55t of gold in June following three straight months of selling

- The Central Bank of Türkiye's return to net buying in June helped the trend in central bank demand remain steadfast

Source: IMF IFS, respective central banks, World Gold Council

*Data as of 30 June 2023 where available

Reported net purchases from central banks totalled 55t, the first month of sizeable global net buying since February.1

As in recent months, activity from the Central Bank of Türkiye (CBRT) was pivotal to the global total.2 Having been a significant net seller between March and May in order to meet local demand, it swung back to net buying in June, adding 11t to its official reserves.3 The CBRT’s total gold reserves stood at 440t at the end of June (29% of total reserves).

The bank’s activity underlined and clarified the continuing trend in central bank gold demand. Six central banks added gold during the month, with only two notable sellers. Among the buyers, the People’s Bank of China was the largest. It added 21t to its gold reserves during June, the eighth consecutive month of purchases. Since it began reporting increases in November 2022, gold reserves have grown by 165t (+8%), of which 103t has been bought in 2023, making it the largest buyer y-t-d.

The National Bank of Poland (NBP) was another large purchaser in June, increasing its gold reserves by 14t. This is the third consecutive month of buying from the bank, which last year indicated that it planned to add 100t to its gold reserves.4 The NBP has added 48t y-t-d, pushing its total gold holdings to 277t. Uzbekistan (8t), the Czech Republic (3t), Qatar (2t) and India (1t) were the other notable buyers in June.

At the time of writing, Kazakhstan and Singapore were the only significant (one tonne or more) sellers in June. Kazakhstan’s official gold reserves fell by 3t to 314t (56% of total reserves), with the bank indicating that more selling will likely occur before the end of the year.5 More frequent buying and selling from banks that obtain gold from domestic sources, such as Kazakhstan, is not uncommon. The Monetary Authority of Singapore reduced its gold reserves by 1t during the month.

To read more about central bank gold demand in H1 as a whole, please see our latest Gold Demand Trends report.6

1Based on monthly IMF IFS data and supplemented with data from respective central banks where available and not reported through the IMF at the time of publication. IMF IFS data is reported with a two-month lag, and while most institutions report on a regular basis, some may report with a – sometimes significant – delay. Figures may be subsequently revised as more data becomes available. The data used here informs but is distinct from the central bank demand estimates we report in Gold Demand Trends. Please see footnote 3 for more information.

2Türkiye official sector gold reserves are the sum of central bank-owned gold and Treasury gold holdings. This is equivalent to gross gold reserves less all gold held at the central bank in relation to commercial sector gold policies (such as the Reserve Option Mechanism (ROM), collateral, deposits and swaps). For information on this methodology, click here.

3For more, see: Turkey to suspend some gold imports after earthquake -Bloomberg News | Reuters

6For purposes of Gold Demand Trends, central bank demand is defined as net purchases (i.e. gross purchases less gross sales) by central banks and other official sector institutions, including supra national entities such as the IMF and sovereign wealth funds where applicable. Our quarterly central bank demand data is sourced from Metals Focus, whose proprietary estimates of official sector activity incorporate various sources, including IMF IFS reports, international trade data, and others. As such, IMF IFS data is a subset of what is included in Gold Demand Trends. Both data sets are subject to revision as new information is made available and/or to accommodate late or updated data reported by official institutions.

使用微信扫一扫登录

[世界黄金协会]