Key highlights:

- Both the Shanghai Gold Price Benchmark PM (SHAUPM) in RMB and the LBMA Gold Price AM in USD registered gains in December. And the SHAUPM ended 2022 with a 10% rise, stronger than its peer in USD on the back of a weaker RMB

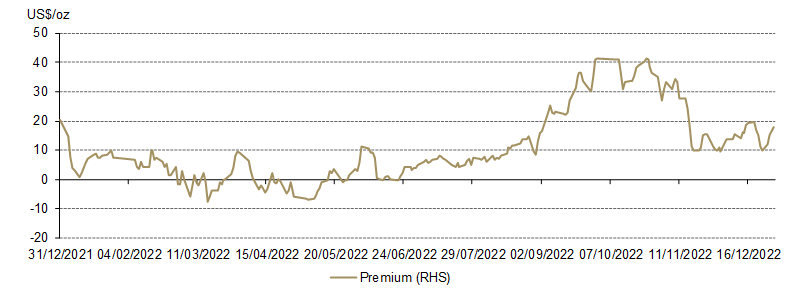

- The Shanghai-London gold price premium fell further in December. Throughout 2022 demand and supply dynamics in China’s gold market were driving the local gold price premium

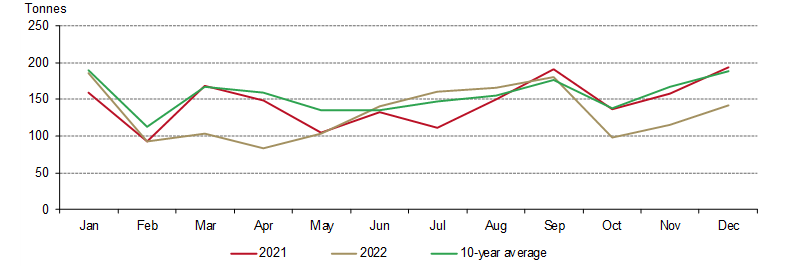

- December gold withdrawals from the Shanghai Gold Exchange (SGE) were the weakest in 10 years as surging COVID infections dented demand; annual wholesale gold demand was 1,571t, 174t lower than 2021

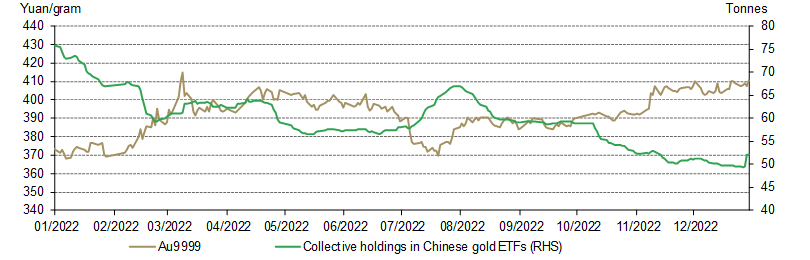

- The positive demand of 0.9t in December was too little too late to reverse the 24t (US$1.4bn, RMB9.8bn) annual outflow from Chinese gold ETFs, the largest annual loss on record

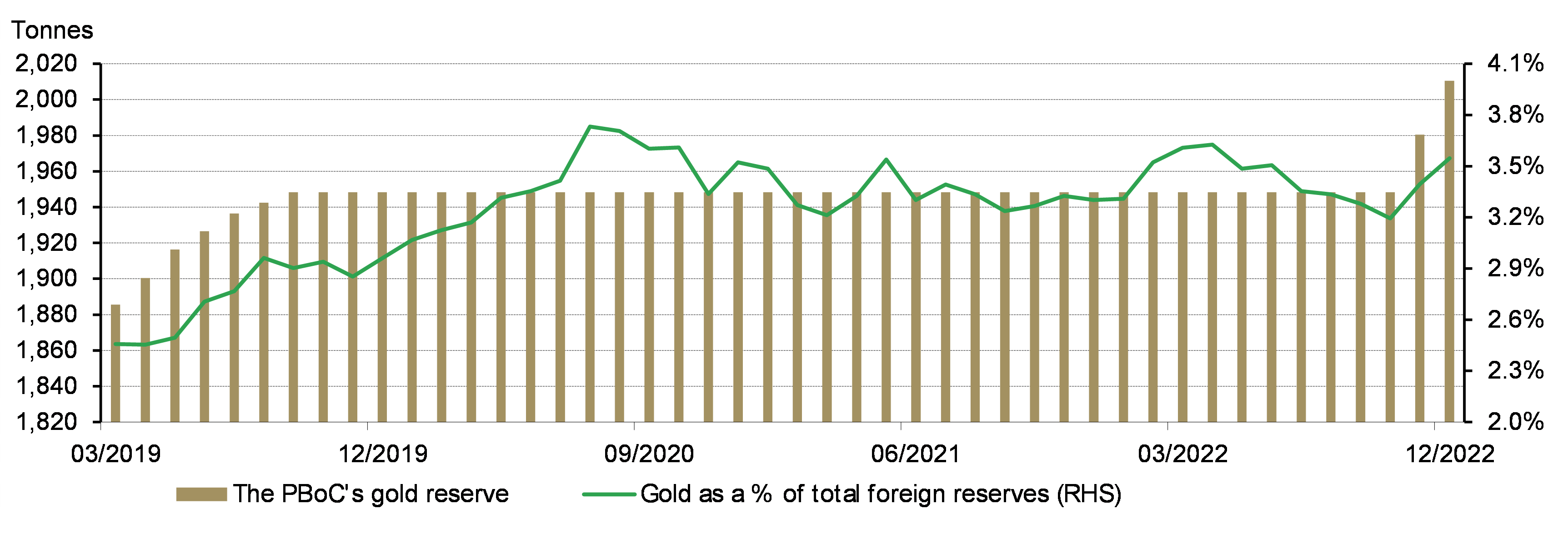

- The People’s Bank of China (PBoC) announced another 30t gold purchase in December, the second consecutive monthly increase after being quiet for three years. This took its total gold reserves to 2011t, 62t higher in the year.

Looking ahead:

- China’s economic recovery and gold consumption should benefit from the end of the strict zero-COVID policy and policy makers’ prioritisation of consumption stimulation. Although challenges such as future COVID infection waves may exist, we expect a rebound in China’s gold demand in 2023, the Year of the Rabbit

- As mentioned previously, in the near-term local gold consumption may receive traditional festive boosts from the approaching Chinese New Year’s (CNY) holiday in late January, especially as the first national COVID wave after opening up peaked in December.

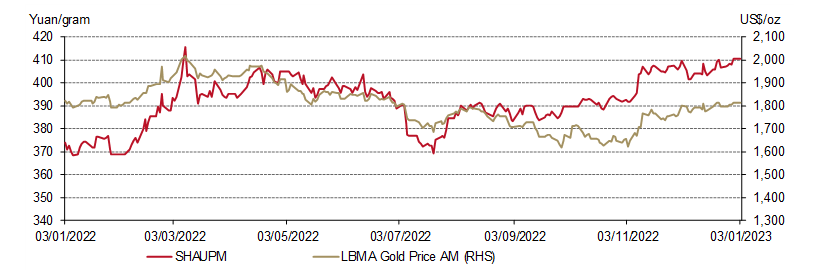

The RMB gold price ended 2022 with a 10% gain

Intensifying expectations of a less-hawkish US Fed bode well for international gold prices during the last month of 2022. While the SHAUPM in RMB rose 1% in December, the LBMA Gold Price AM in USD capped a 3% gain. The appreciating RMB against the dollar during the month contributed to the relative underperformance of the Chinese gold price.

Nonetheless, the RMB gold price concluded 2022 with a 10% gain. Geopolitical uncertainties, inflationary concerns and a weak local currency all contributed to this sizable rise. Meanwhile, the LBMA Gold Price AM in USD saw a mild decline of 0.4% over the year in the face of a strong dollar.2

Chart 1: 2022 – a strong year for the RMB gold price

The SHAUPM in Yuan/gram and LBMA Gold Price AM in US$/oz*

The local gold price premium fell further in December. With local gold demand continuing to weaken as COVID infections surged, the average Shanghai-London gold price spread in December lowered to US$16/oz, a US$4/oz decrease m-o-m. Most days during 2022 saw the spread mirror the changes in China’s gold demand, as detailed below.

Chart 2: The local gold price premium

The 5-day rolling average spread between SHAUPM and LBMA Gold Price AM in US$/oz*

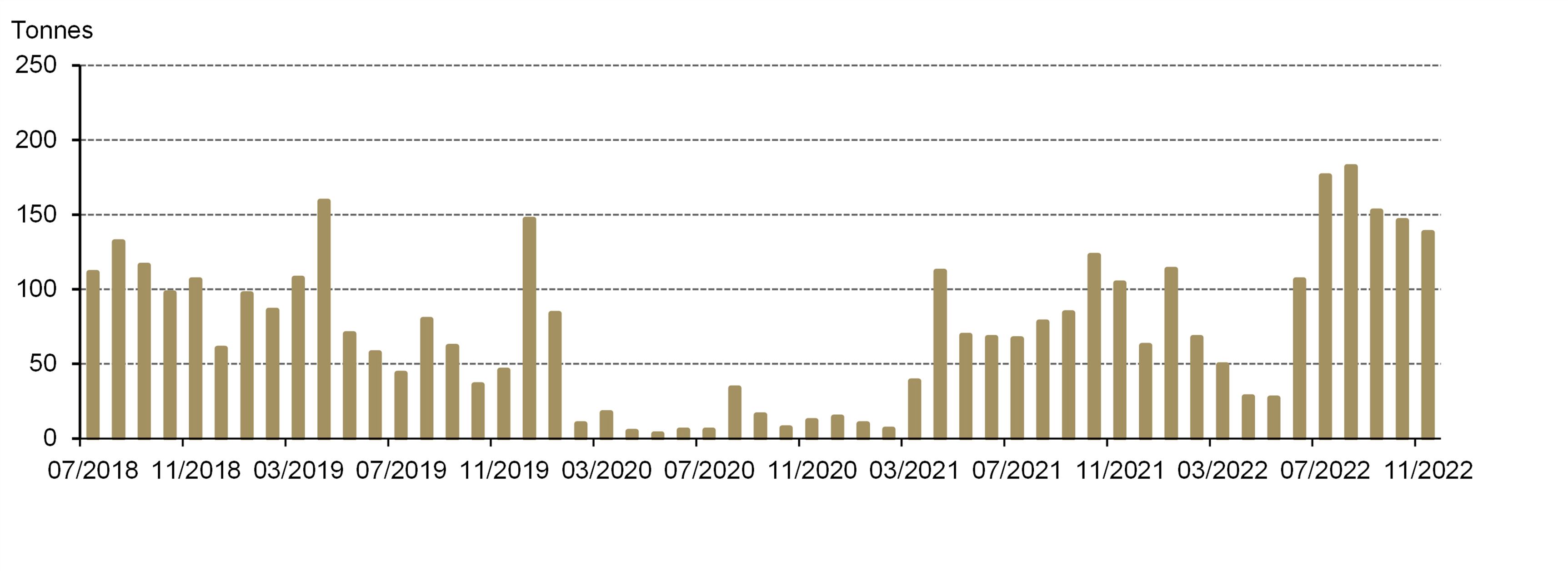

Weak December wholesale gold demand reflects a weak 2022

Last month 142t of gold left the SGE’s vaults, 26% lower y-o-y and the weakest December since 2012. The rapid spread of Omicron after China’s sudden lifting of almost all domestic mobility restrictions in early December infected many, denting both local economic activity and gold demand. Meanwhile, temporary labour shortages amid the infection surge limited the ability of gold manufacturers to replenish stock ahead of the anticipated sales boost during the Chinese New Year (CNY) holiday.

On a m-o-m basis, gold withdrawals from the SGE were 26t higher. This can be partially attributed to easing mobility restrictions compared to previous months and to seasonality, albeit significantly weakened by the rapid spread of the virus.

Looking back at 2022, manufacturers withdrew 1,571t of gold from the SGE, 174t lower y-o-y and the second weakest in the past 10 years. The COVID pandemic has undoubtedly impacted China’s economic recovery and local gold demand. During the majority of H1, severe COVID-related lockdowns in major cities limited China’s economic activities and hammered local gold demand. Wholesale gold demand started to recover in June as the spread of COVID stabilised but hopes were dashed as local infections surged in Q4.

Chart 3: Weak wholesale gold demand in 2022

Chinese gold ETF holdings lost 24t in 2022

Holdings in Chinese gold ETFs totalled 51.4t (US$3bn, RMB21bn) at the end of 2022, an inflow of 0.9t (US$53mn, RMB369mn) during December. Chinese gold ETF holdings lowered by 24t (US$1.4bn, RMB9.8bn) last year, the largest annual loss on record.

Tactical moves drove demand for Chinese gold ETFs during 2022. While the strong RMB gold price contributed positively to many investors’ portfolios, some viewed these gains as opportunities to take profits. Others utilised gold price dips to either enter the market or increase their holdings. In general, changes in Chinese gold ETF holdings and the local gold price exhibited a negative relationship during the year.

Chart 4: Chinese gold ETF investors responded to local gold price changes

Daily Chinese gold ETF holdings and close of Au9999 price

The PBoC announced its second consecutive monthly gold purchase as 2022 ended

Following its November purchase, the PBoC made another announcement of its gold reserve increase in December. China’s gold reserves stood at 2,011t as of 2022, 30t higher m-o-m and accounting for 3.6% of its total foreign reserves.

In 2022, China declared two gold reserve rises during November and December, totalling 62t. And the announcements broke the PBoC’s silence on gold purchases since September 2019. During a 2015 press conference, the State Administration of Foreign Exchange indicated that it regarded gold as an asset with multiple functions that could benefit its reserve portfolio’s performance.4

Chart 5: The PBoC’s gold reserves rose again in December

Gold imports fell further in November

China imported 138t of gold in November, 34t higher y-o-y and 8t lower m-o-m (Chart 6). Similar to the previous month, imports continued to moderate m-o-m with the pace of local wholesale gold demand. But the elevated local gold price premium may have encouraged the y-o-y strength.

Chart 6: China’s gold imports declined further in November

China’s gold imports under HS7108*

2023 Chinese gold demand outlook

China’s reopening, albeit hasty, should bode well for its economic recovery and gold demand. Even though raging COVID infections initially kept many consumers at home, figures from late December show that economic activity is restoring vitality. According to Bloomberg’s median forecast, China’s GDP growth in 2023 is likely to reach 4.8%, a notable rebound from 2022. This will likely be a key driver in providing support to local gold consumption.

In addition to the removal of COVID restrictions, China’s gold demand may benefit from the government’s efforts to stimulate consumption, as indicated at the year-end Central Economic Work Conference chaired by President Xi.5

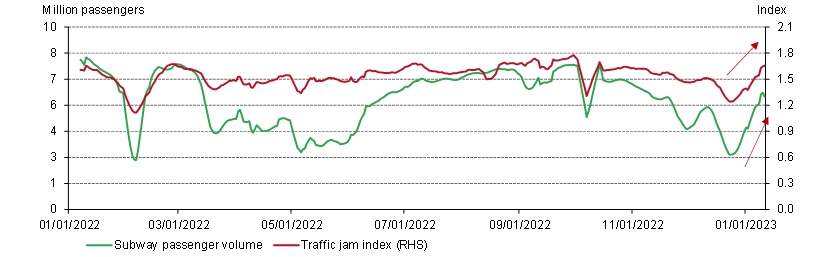

Chart 7: City traffic is increasing

7-day rolling averages of daily subway passenger volumes and the traffic jam index in major cities*

The above-mentioned should support Chinese gold demand’s rebound in 2023 but challenges remain. First, as restrictions are removed, the potential surge in domestic and international travel may impact the budget that consumers have to spend on gold.6 Second, future waves and virus variants could bring further consumption disruptions, although the impact is likely to diminish as vaccination rates rise and immunity in the general population increases. In general, we expect China’s gold demand in 2023 to rebound from its 2022 low.

For more detailed analysis, please stay tuned for our 2022 Gold Demand Trends later this month.

Footnotes