Key highlights:

- The Shanghai Gold Price Benchmark PM (SHAUPM) in RMB and the LBMA Gold Price AM in USD both declined. Meanwhile, the Shanghai-London gold price spread turned positive as local gold demand started to recover1

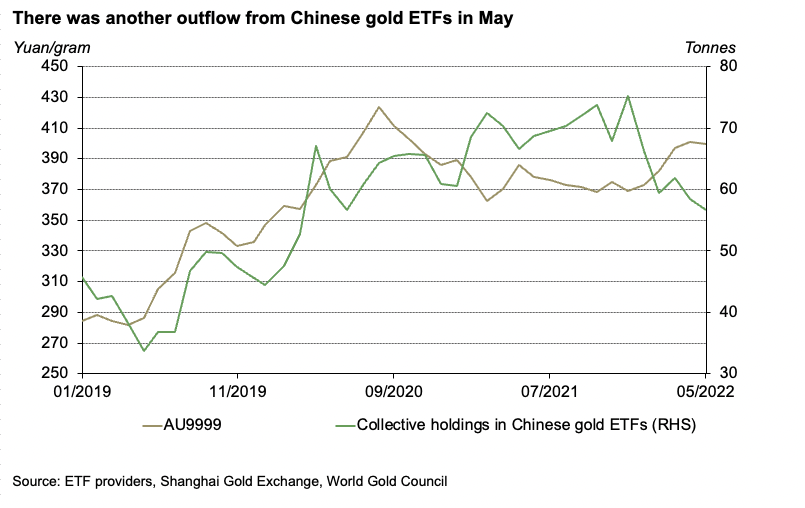

- At the end of May, Chinese gold ETF holdings totalled 56.7t (US$3.4bn, RMB22.7bn), representing a 1.8t (US$143mn, RMB0.8bn) outflow during the month2

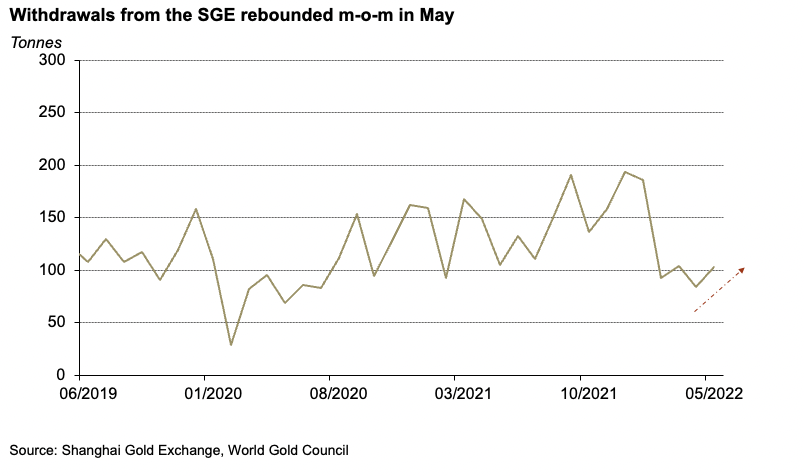

- Driven by falling COVID cases and the industry expectation of improved consumption, gold withdrawals from the Shanghai Gold Exchange (SGE) rebounded m-o-m.

Looking ahead:

- As major Chinese cities emerge from the COVID resurgence and related restrictions come to an end, local gold demand is likely to improve in the near term. And various demand-side stimulus measures could also benefit Chinese gold consumption.3

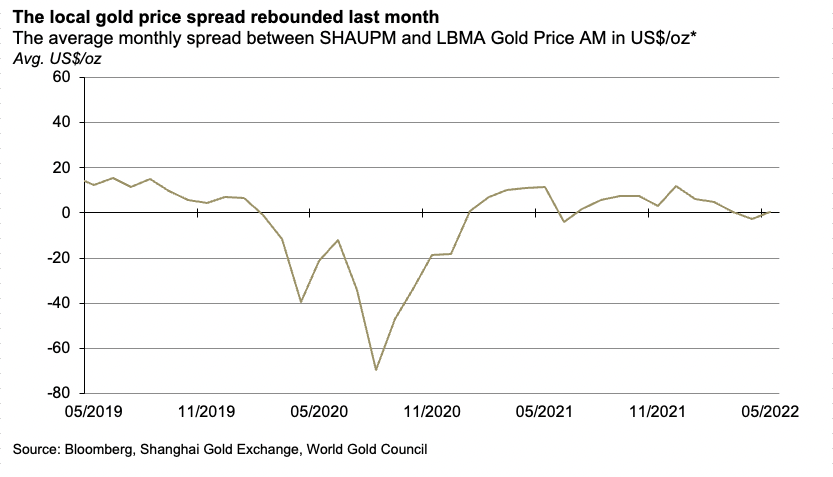

Gold prices declined but the local gold price spread rose

Gold prices fell in May. Primarily driven by negative momentum impacts as well as lower risk and uncertainty, the SHAUPM in RMB and the LBMA Gold Price AM in USD fell by 1.8% and 3.2% respectively in the month. And with the RMB depreciating against the dollar, the gold price in RMB had a narrower decline than its USD peer.

The Shanghai-London gold price spread flipped back to positive territory in May, averaging US$0.4/oz. This was primarily helped by a m-o-m rebound in local wholesale physical gold demand – see more details below – and a possible shrink in supply due to lower imports during recent months.

*Before April 2014 the spread calculation was based on Au9999 and LBMA Gold Price AM; click here for more.

Chinese gold ETF holdings fell further

Outflows from Chinese gold ETFs continued last month. Total assets under management (AUM) in Chinese gold ETFs reduced by 1.8t (US$143mn, RMB0.8bn), to 56.7t (US$3.4bn, RMB22.7bn) in May. As COVID restrictions in Shanghai eased and various stimuli were rolled out, local investor risk appetite improved: the CSI 300 Stock Index saw its first monthly gain this year, and this has led to a decline in local investor demand for safe-haven assets such as gold.

Wholesale physical gold demand improved m-o-m

As the COVID resurgence in China cooled and related restrictions in various regions eased, wholesale physical gold demand started to recover.4 Gold withdrawals from the SGE saw a 19t rebound m-o-m, totalling 103t in May. And on a y-o-y basis they were 2t lower than May 2021.

Meanwhile, policy makers rolled out various stimulus measures to stabilise China’s economic growth.5 And these measures may have shored up jewellery retailer and manufacturer confidence, contributing to higher gold withdrawals in the month.

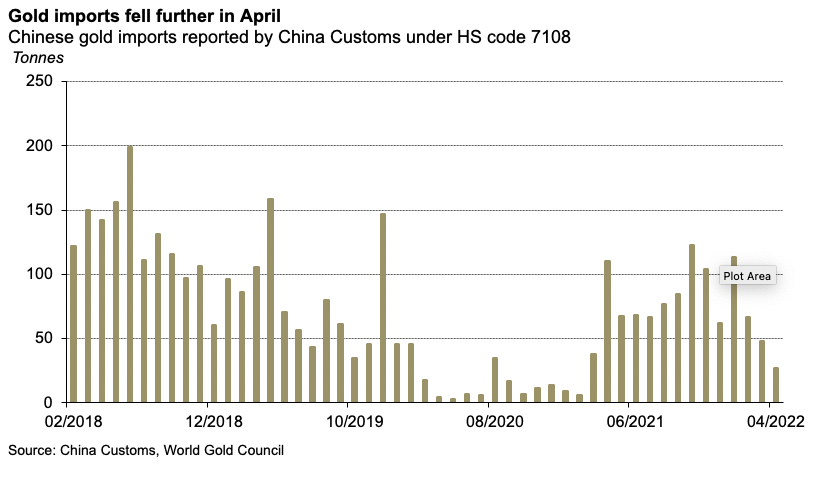

In April, gold imports saw another decline

China imported 27t of gold in April, 21t lower m-o-m and 84t less than April 2021. Weakened gold demand amid strict lockdowns in key regions, including Shanghai, and a negative Shanghai-London gold price spread in April both weighed on gold imports in the month.6

Looking ahead

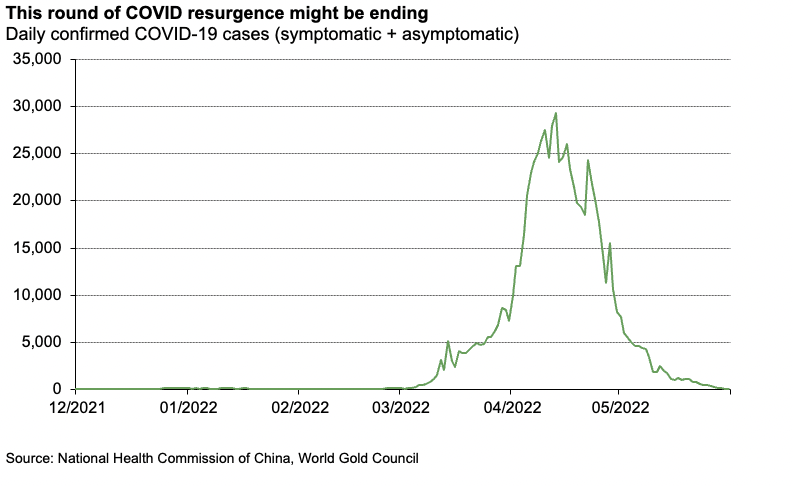

Strict COVID restrictions have finally yielded fruit. Confirmed local COVID cases fell sharply in May allowing related restrictions to be eased; the lockdown in Shanghai was lifted on 1 June and restrictions in Beijing were relaxed.7

To support economic growth, China has rolled out various stimulus measures. These include supply-side stimuli such as rate and tax cuts, and demand-side support including consumption vouchers and electric car subsidies.8

As China gradually recovers from the most recent COVID hit and as stimulus measures gather pace, we expect Chinese gold consumption to improve over the coming months. A weakening currency, rising inflationary pressures and lower bond yields may help raise investor interest in gold investment products. And we believe a stable gold price and pent-up wedding demand could also benefit gold jewellery consumption.