Key highlights:

- The Shanghai Gold Price Benchmark PM (SHAUPM) in RMB rose in April while the LBMA Gold Price AM in USD saw a slight decline. But the Shanghai-London gold price spread turned negative despite the RMB gold price strength1

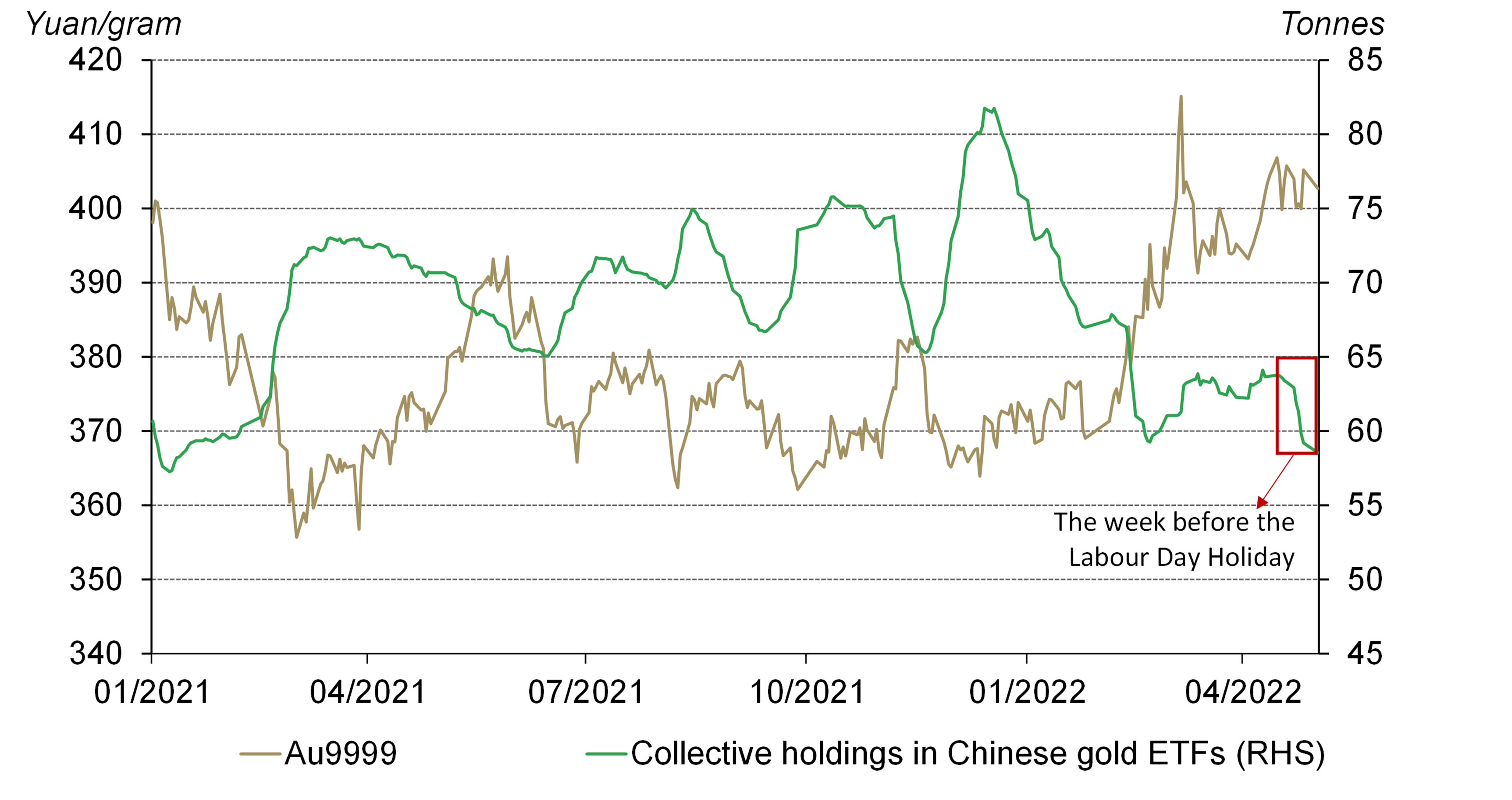

- Chinese gold ETF holdings totalled 58.5t (US$3.5bn, RMB23.5bn) at the end of April, following a 3.3t (US$323mn, RMB1.1bn) outflow in the month2

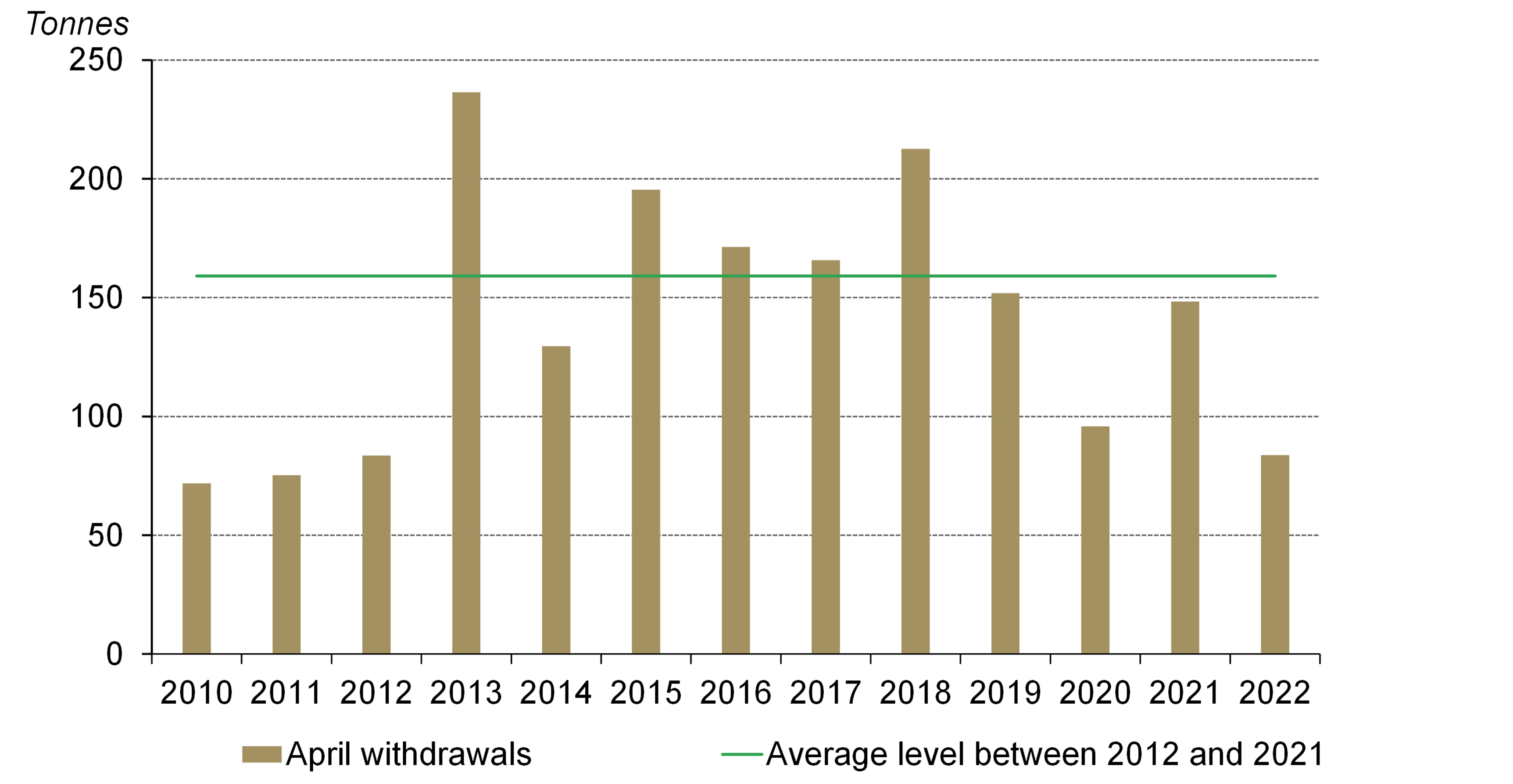

- Gold withdrawals from the Shanghai Gold Exchange (SGE) last month were the lowest April since 2012 – lockdowns in major Chinese cities continued to play a major role weighing on local gold demand

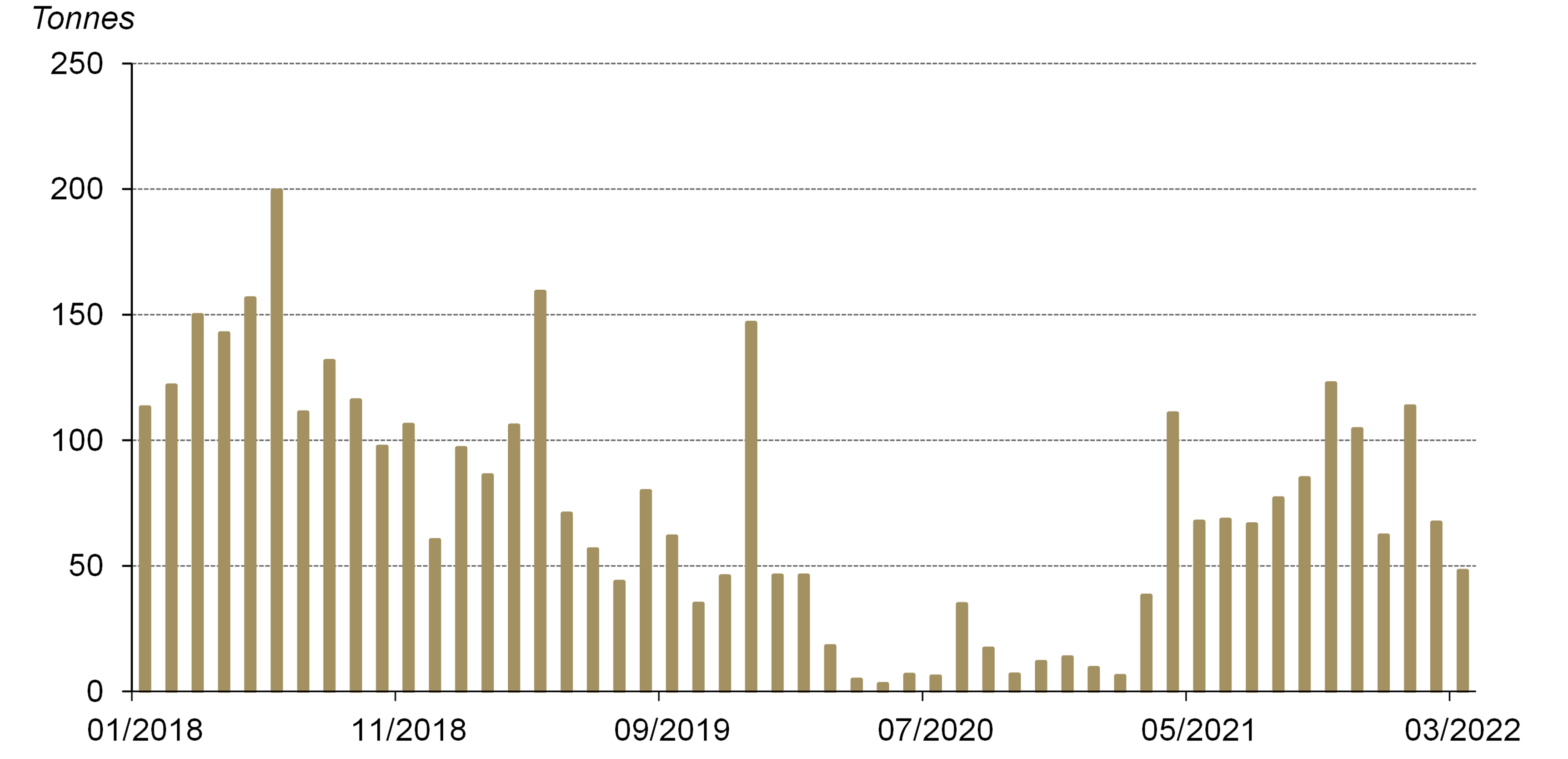

- Despite a decline in March, China’s gold imports in the first quarter were significantly higher than either 2021 or 2020 thanks to strong local gold consumption during the first two months of 2022.3

Looking ahead:

- In the short run China’s gold consumption is likely to remain weak amid COVID-related lockdowns in various cities. But in the longer-term China is likely to adopt accommodative policies to support economic growth, which should benefit China’s gold consumption.

The RMB gold price rose, local gold price spread turned negative

International and domestic gold prices diverged in April. While the RMB gold price – SHAUPM – rose 2.9%, the LBMA Gold Price AM in USD fell by 0.5% amid higher interest rates in many markets and a stronger US dollar in the month. The relative outperformance in the RMB gold price could be primarily attributed to a depreciating Chinese currency against the USD.

Even so, the Shanghai-London gold price spread dropped into negative territory in April, averaging -US$2.8/oz, the first average monthly discount since June 2021. Local gold demand remained weak amid prolonged COVID-related lockdowns in major Chinese cities.

The local gold price spread turned negative in April

The average monthly spread between SHAUPM and LBMA Gold Price AM in US$/oz*

April saw outflows from Chinese gold ETFs

Chinese gold ETF holdings saw an outflow of 3.3t (US$323mn, RMB1.1bn) last month, reducing total assets under management (AUM) to 58.5t (US$3.5bn, RMB23.5bn). Continued stock market weakness and the listing of another new Shanghai Gold ETF in April were not able to stop the outflow, which was likely driven by:

- possible profit-taking activities as the local gold price rose

- investors unwinding positions ahead of the five-day Labour Day Holiday (30 April – 3 May) to avoid potential volatilities while local markets were closed.

Wholesale physical gold demand in April fell to its lowest since 2012

Gold withdrawals from the SGE amounted to 84t last month, 19% lower m-o-m, 44% lower y-o-y. The weakest April wholesale gold demand in China since 2012 came as no surprise given prolonged COVID-related lockdowns imposed on major Chinese cities, including Shanghai.

Gold imports continued to fall in March

Gold imports totalled 48t in March, according to the latest data from China Customs. This is 19t lower m-o-m, reflecting lower local gold demand and the inconvenience in clearing customs due to various city-wide lockdowns. Furthermore, the sharply lower Shanghai-London gold price spread also dulled the appeal for importers.

Gold imports continued to fall in March

Chinese gold imports reported by China Customs under HS code 7108

Driven by strong gold consumption during the first two months of the year, China’s Q1 gold imports were resilient despite the COVID resurgence in March. Gold imports totalled 229t in the first quarter of 2022, significantly higher than the same periods in 2021 and 2020, when border controls were much stricter. And this was only 60t lower than the pre-pandemic level in Q1 2021.

Looking ahead

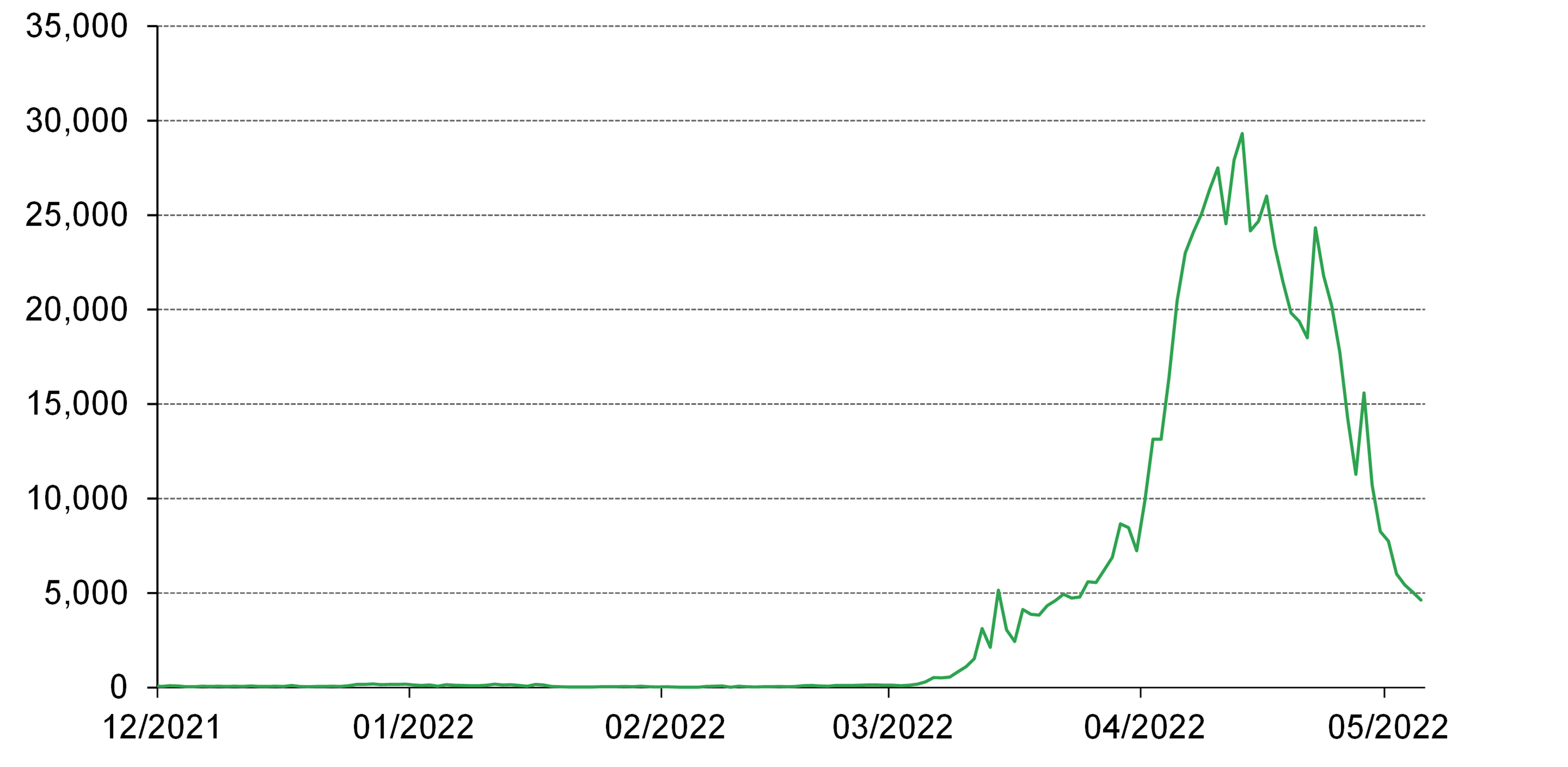

Progress in containing COVID-19’s resurgence is key to China’s gold demand in the short term. While recent declines in confirmed cases were a cause for optimism, lockdown policies in Shanghai and other cities have remained strict. And Beijing has begun to implement social restrictions to stifle the Omicron outbreak there.4

We expect China’s gold consumption to stay weak in May even though this is traditionally a peak month in the otherwise quiet Q2 period as retailers take advantage of the Labour Day Holiday and Mother’s Day to promote gold products. And this could exacerbate the seasonal weakness of Q2’s gold consumption as a whole.

But in the longer run we believe policy makers are likely to roll out various stimuli to support China’s recovery, including accommodative monetary and fiscal policies, such as distributing consumption vouchers. These measures could support a recovery in Chinese gold consumption. Similar actions were taken after Q1 2020 when the pandemic first hit China and they contributed to the recovery in gold demand that year.

The COVID resurgence since March might be near its end

Daily confirmed COVID-19 cases (symptomatic + asymptomatic)

Footnotes

We compare the LBMA Gold Price AM to SHAUPM because the trading windows used to determine them are closer to each other than those for the LBMA Gold Price PM. For more information about Shanghai Gold Benchmark Prices, please visit Shanghai Gold Exchange.

Please note that the inflow/outflow value term calculation is based on the difference between end-of-period assets under management, which is based on the end-of-period Au9999 prices in RMB and the USD/CNY rate.

There is a one-month lag in China Custom’s gold import and export data publication schedule.

For more information, please visit: Beijing asks residents to work from home - Chinadaily.com.cn