The September edition of Bank of America’s bellwether Global Fund Manager Survey highlights a growing disconnect between fund managers’ expectations and their positioning: funds remain heavily overweight equities despite increasing pessimism over global economic prospects.

According to the survey, expectations for global growth have tanked to their lowest in nearly 18 months, with only a net 13% of fund managers now looking for the global economy to improve, having peaked at 91% in March. The Delta variant shoulders much of the blame for this deterioration in sentiment.

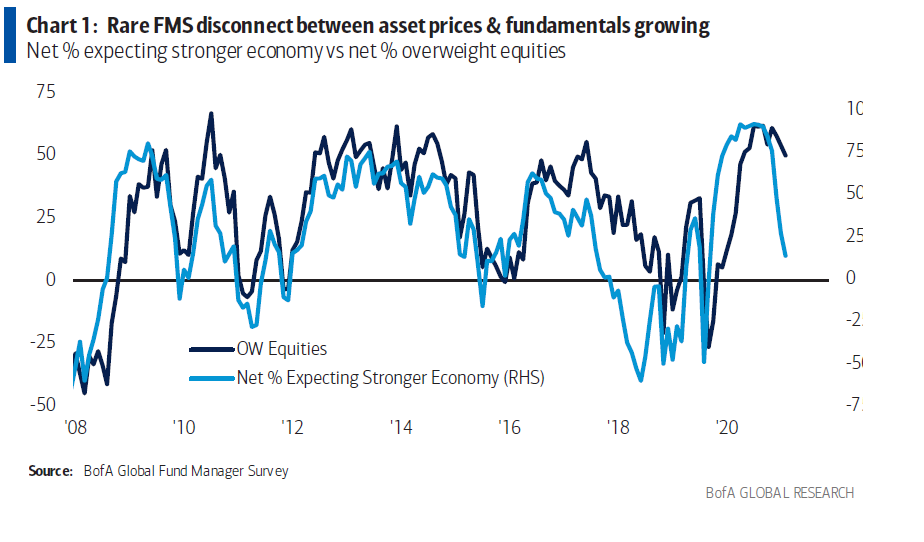

But, despite their increasingly gloomy outlook, the respondents remain overweight equities (by a net 50%). With rates not predicted to rise before Feb 2023, managers are unwilling to bump up their fixed income exposure given the paltry yields on offer, and cash allocations are barely changed at 4.3% (vs 4.2% in August).

The rarity of this combination of growth pessimism and equity positioning is neatly highlighted in the chart, which could suggest an imminent downturn in equity weightings.

Back in January, we highlighted the risk for sharp pullbacks in equities this year, given the growing rift between valuations and the underlying fundamentals in such a crowded trade. Global stock market performances so far this year – particularly in the context of these survey results – does little to suggest that risk has abated. Yet, according to the survey, fewer portfolio managers are hedging their equity exposure against such a correction than at any time since January 2018.

They may be prudent to use gold to help mitigate the potential risks of this approach. Thanks to its historical track record of negatively correlating to equities during sharp equity pullbacks, an allocation to gold has historically helped portfolios to weather such episodes. This is a feature that institutional investors seem to recognise: 77% of respondents to a Coalition Greenwich survey who currently hold gold in their portfolio cited “diversification” as its primary role.1

As the FT’s Robert Armstrong muses ‘Change is coming, gradually or quickly. This year’s massive flows could dribble back into cash and bonds, or come out all at once, in a disorderly rush.’ Diverting a little of these flows into gold now could help stem the tide should it turn unexpectedly.

Footnotes

Conducted by Coalition Greenwich (formerly Greenwich Associates) in partnership with the World Gold Council, this study queried nearly 500 institutional investors across the Americas, EMEA and APAC, examining shifting allocation priorities and strategies (gold and broader asset classes as investors face an unprecedented global reset).