Summary

- The domestic gold price ended 5.9% higher in April at Rs46,604/10g1

- The second wave of the pandemic and a higher domestic gold price stifled retail demand in the month

- Indian official imports were steady and the local market premium fell sharply

- Volatility and a decline in the BSE SENSEX led to safe-haven demand through ETF inflows. Total holdings for Indian gold-backed ETFs (gold ETFs) reached 33.1t by the end of April; a net inflow of 1.3t (Rs6.8 bn; US$84mn)

- The Reserve Bank of India (RBI) made no gold purchases in the month, maintaining its total gold reserves at 695.3t.

Gold prices rebounded in April

The fall in the US 10-year bond yield, along with a weakening dollar, lifted the USD gold price and growing inflation expectations contributed further to the price rebound. And in India, a depreciating rupee amid the second wave of COVID-19 provided further upside to the local gold price. As a consequence, the LBMA Gold Price AM in USD and MCX Gold Spot in INR rose by 5% and 5.9%, respectively, during the month (Chart 1).2

Chart 1: Gold prices rebounded in April

Domestic gold price in rupees vs LBMA Gold Price AM in US dollars

Source: Bloomberg, ICE Benchmark Administration, World Gold Council

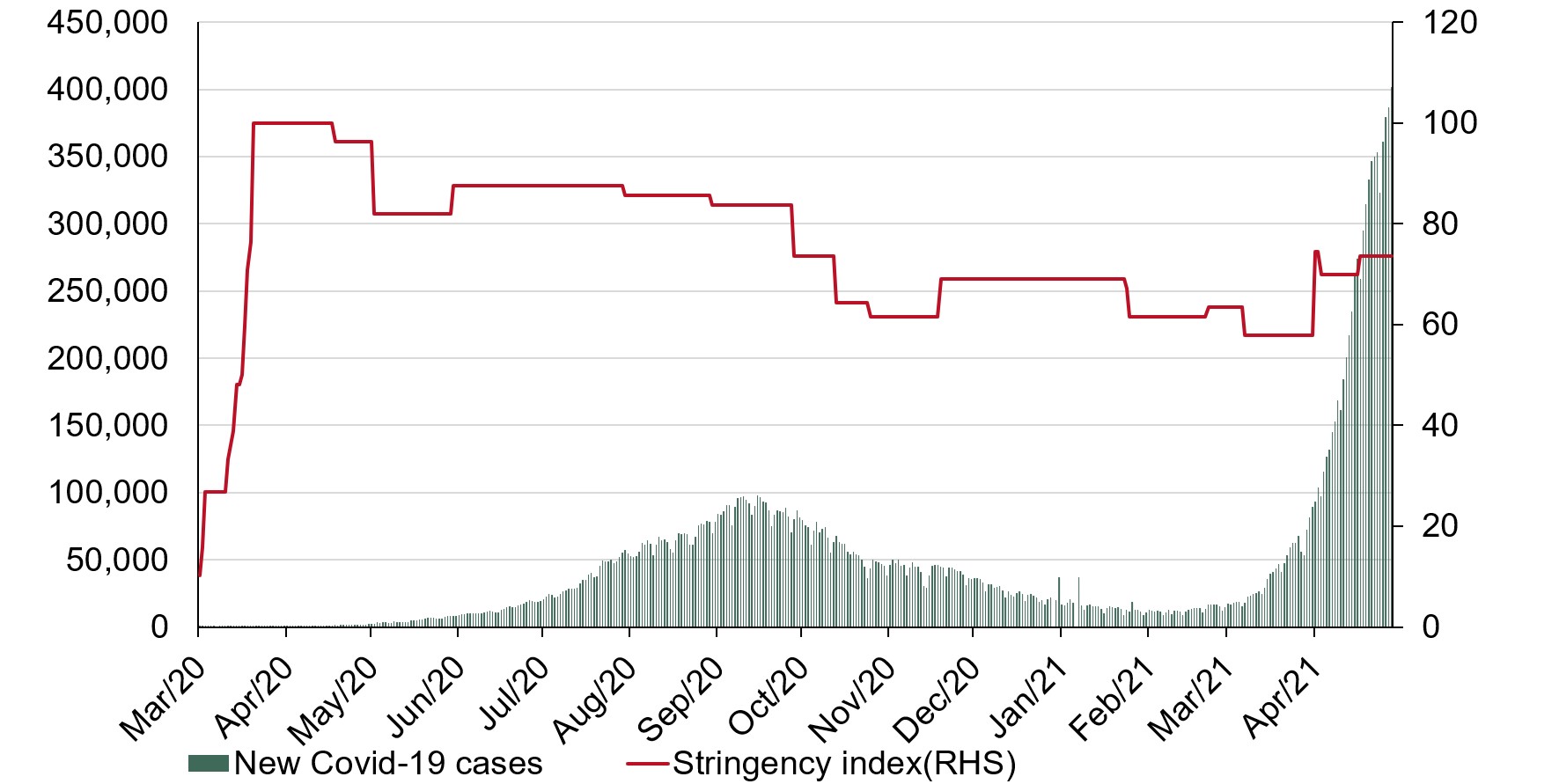

April’s surging COVID-19 cases raise concern for the economy

The ferocity of the second wave of infections has overwhelmed India and made lockdowns and restrictions inevitable. However, fewer restrictions have been imposed in this wave than the first one in 2020, with agriculture, construction, manufacturing and other essential services permitted to continue this time around (Chart 2). But the intensity of the second wave, particularly in metros/cities, and its rapid spread across states, regions and pockets of rural India, has impacted demand throughout the month. Several high frequency indicators, such as E-Way bill, power demand, railway/ flight reservations and passenger vehicle sales contracted in April.3

Chart 2: COVID-19 infections soared but lockdowns less restrictive

Note: A Stringency Index created by Oxford University shows how strict a country’s measures were, and at what stage of the pandemic spread it enforced these measures.

Source: Oxford Covid-19 response tracker, John Hopkins University, World Gold Council

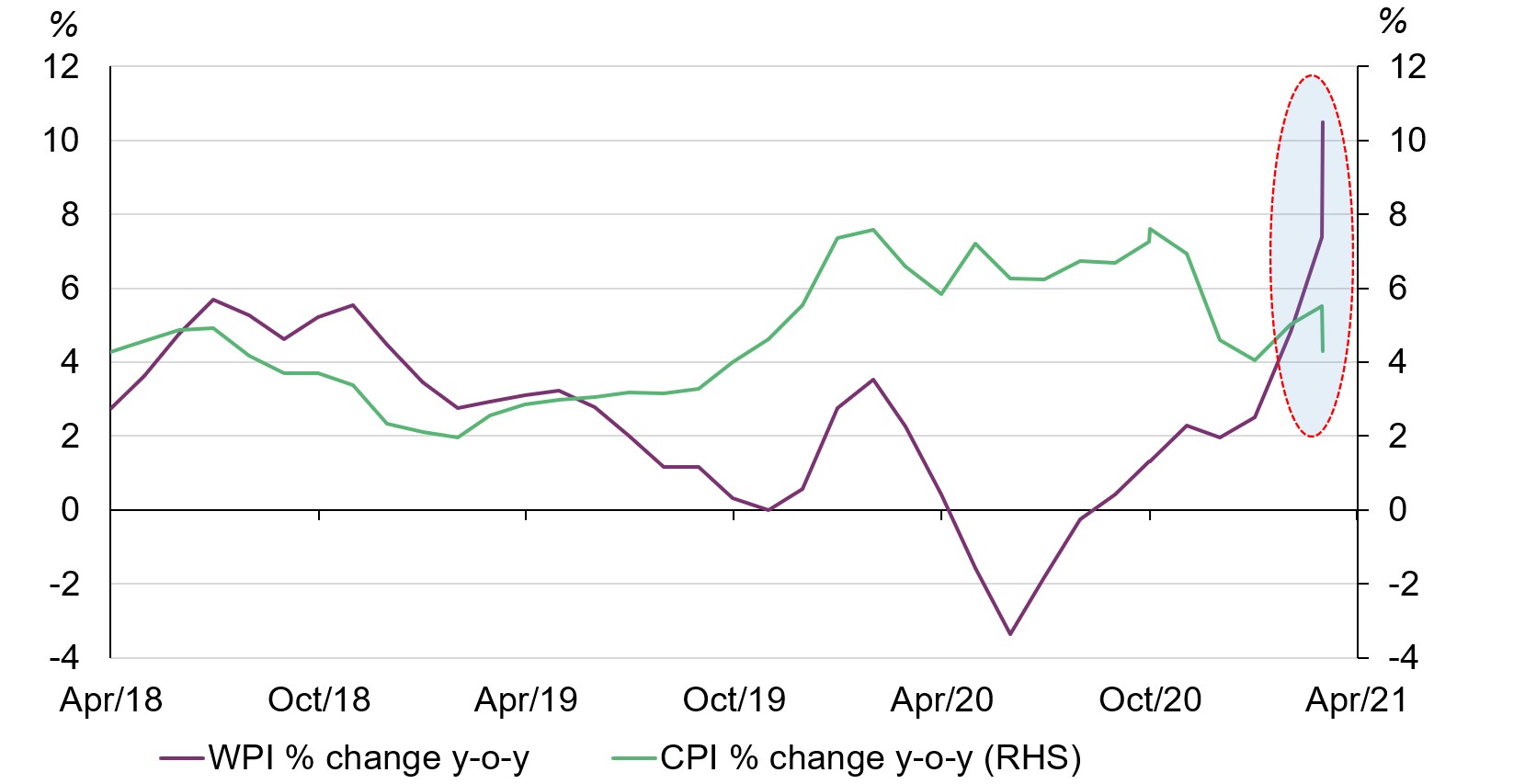

Wholesale and retail inflation diverged in the month

India’s wholesale inflation (WPI) rose in April to its highest for more than a decade (10.49% y-o-y) due to the effect of a low base and the rising cost of food and commodity prices (Chart 3). Supply chain pressure resulting from the second wave also contributed to the rise. Retail inflation (CPI), however, eased to a three-month low of 4.29% y-o-y thanks to lower food prices, but this is expected to pick up as the impact of wholesale inflation works its way through to the consumer. Rising WPI inflation does not leave much space for rate cuts from the RBI even though the monetary stance is expected to remain accommodative.

Chart 3: India's wholesale price inflation rose to the highest in more than a decade in April

India's WPI % change y-o-y vs CPI % change y-o-y

Source: Bloomberg, World Gold Council

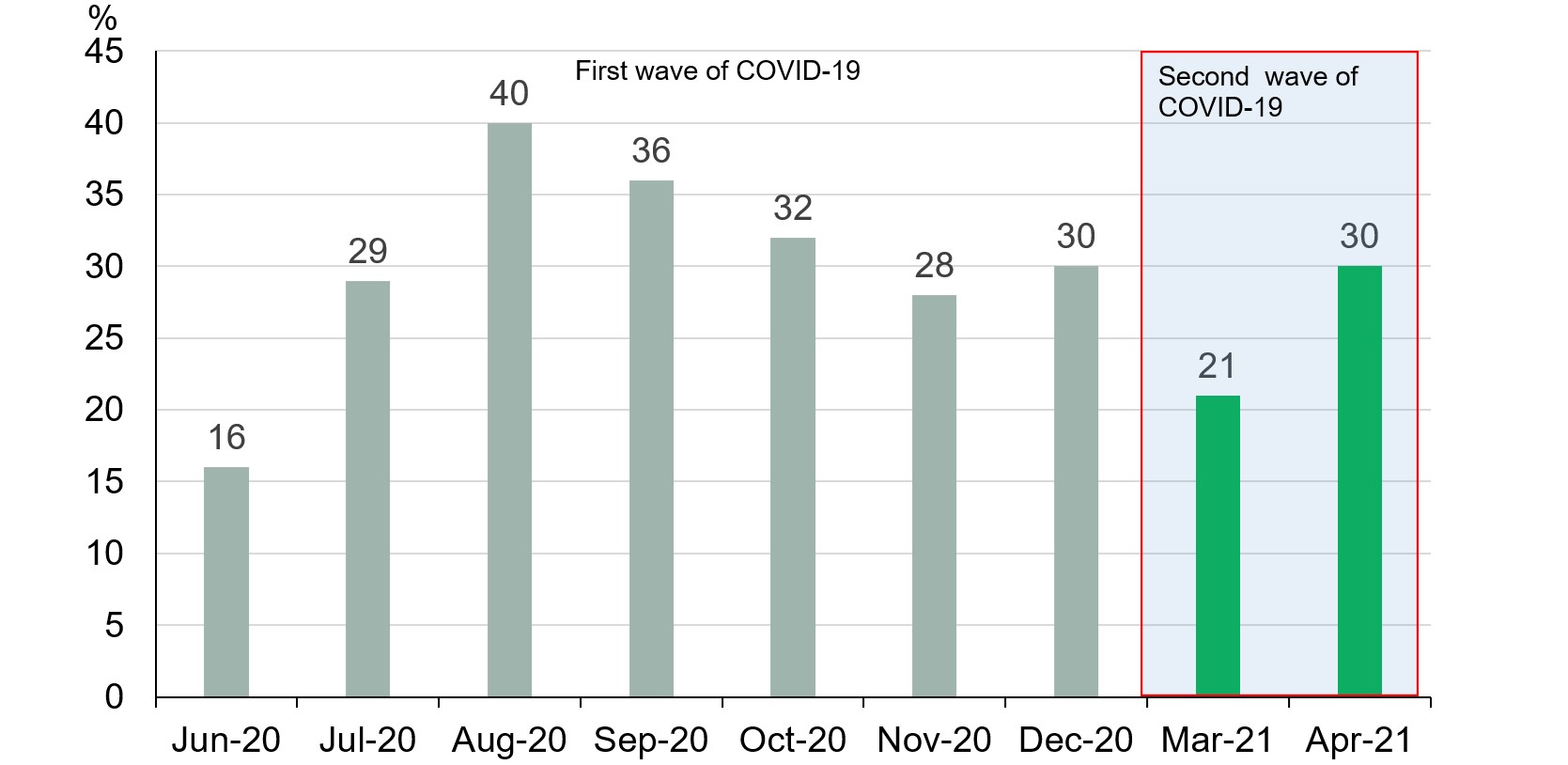

Retail demand was stifled by the second wave of COVID-19

The healthy retail demand in March slowed in April under pressure from surging COVID infections and a rising domestic gold price. Many states implemented partial lockdowns initially in response to rising infection rates, although essential business were allowed to remain open. Consumer confidence dipped markedly during the last two weeks of the month as COVID cases surged and states announced more restrictions and lockdowns. Anecdotal evidence suggests that wedding postponements increased, impacting important wedding purchases. The rising number of COVID cases in rural India – a major source of gold demand – further impacted sales in semi-urban and rural towns (Chart 4).

Looking at market sentiment in May, retail demand on Akshaya Tritiya (AT) – the major gold buying festival, which fell this year on 14 May – remained muted due to store closures. Sales found marginal support through retailers’ digital/omni-channel strategies and demand for digital gold remained strong.

Retail demand is expected to remain muted in May as the majority of states are still under lockdown. However, daily cases of the virus are now starting to decline. If this downward trend continues, lockdowns will likely ease and non-essential businesses re-open, bolstering retail demand.

Chart 4: Rising number of COVID-19 cases in rural India hit demand

Percentage of rural districts with new COVID-19 cases

Note: rural districts defined as those with more than 70% of population categorized as ‘Rural’ as per Census 2011.

Source: CRISIL, World Gold Council

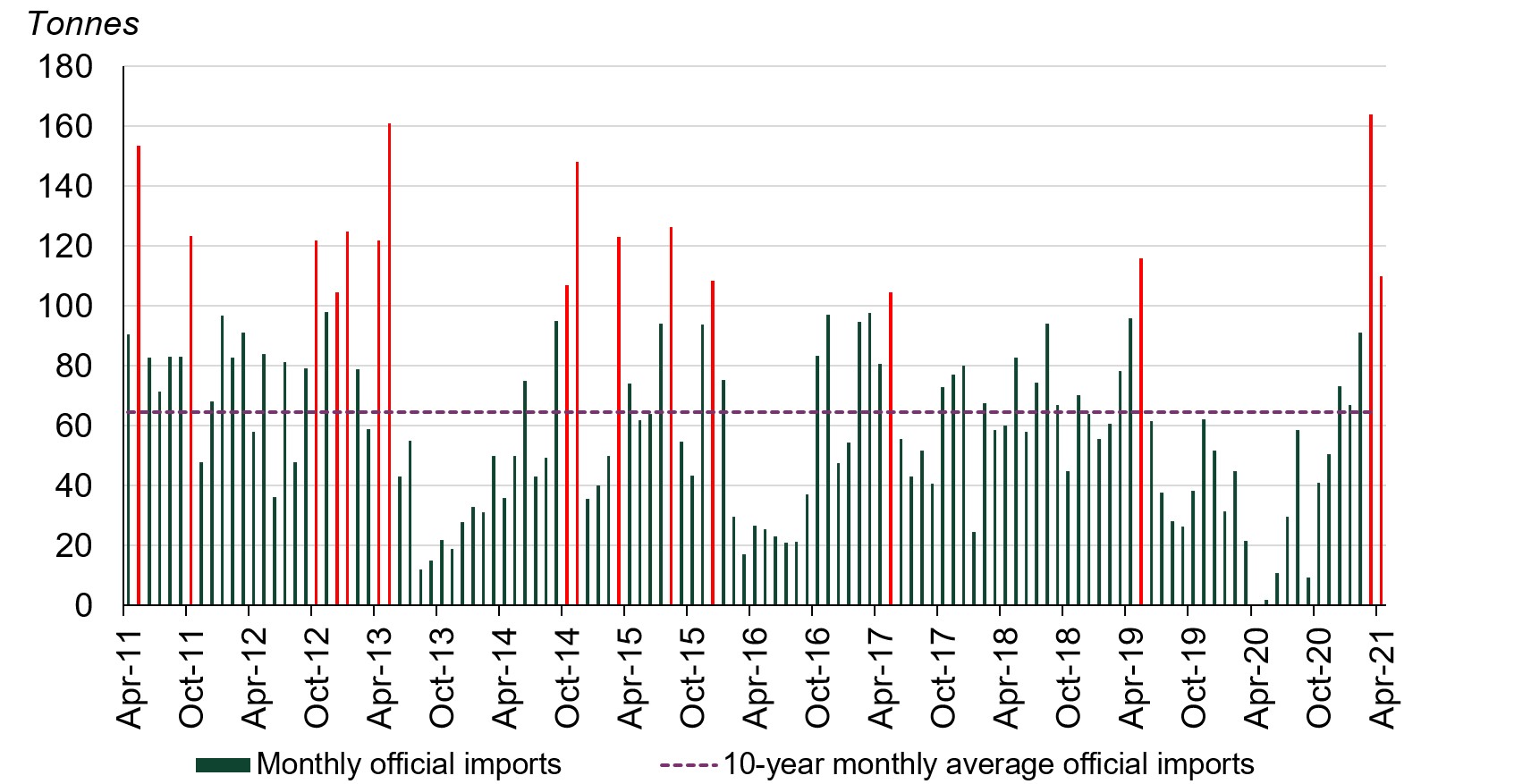

Indian official imports in April were above the 10-year monthly average

Indian official gold imports totalled 110t in April 2021 compared to a negligible 50kgs of imports in April 2020 – at which time imports had been hampered by global supply chain disruptions and nationwide lockdown in India. Official imports in April were also 71% higher than the 10-year monthly average imports of 65.5t (Chart 5). We believe that there were two drivers behind this high import figure: purchases ahead of Akshaya Tritiya and anticipated strong wedding demand. However, neither fulfilled expectations due to the country’s rising infections and consequent restrictions. Looking at official imports, ~60% landed in the first two weeks of the month, maximising benefit from the lower custom tariff in force at the time (US$542/10gm); from 16 April the tariff was raised to US$549/10gm in line with the rising international gold price.4 A total of nine banks, nominated agencies and exporters imported 91.3t of bullion and 18 refineries imported an equivalent 18.7t of fine gold content in the form of gold doré.

From a total of 110t in official imports, 42.3.3t was imported via the Sri City Free Trade Warehousing Zone (FTWZ).5 Seven overseas banks were responsible for these imports, with JP Morgan, ANZ, Rand Merchant Bank and Standard Chartered accounting for 79% of the total.

We anticipate that official imports will remain subdued throughout May. The global reduction in international flights and strict border controls in India are likely to create significant headwinds for gold flows into the country.

Chart 5: Indian gold imports in April were above 10-year monthly average

Indian monthly gold imports from April 2011 - April 2021

Note: Red bar indicates month when imports exceeded 100t.

Source: Infodrive India, Ministry of Commerce & Industry Govt. of India, World Gold Council

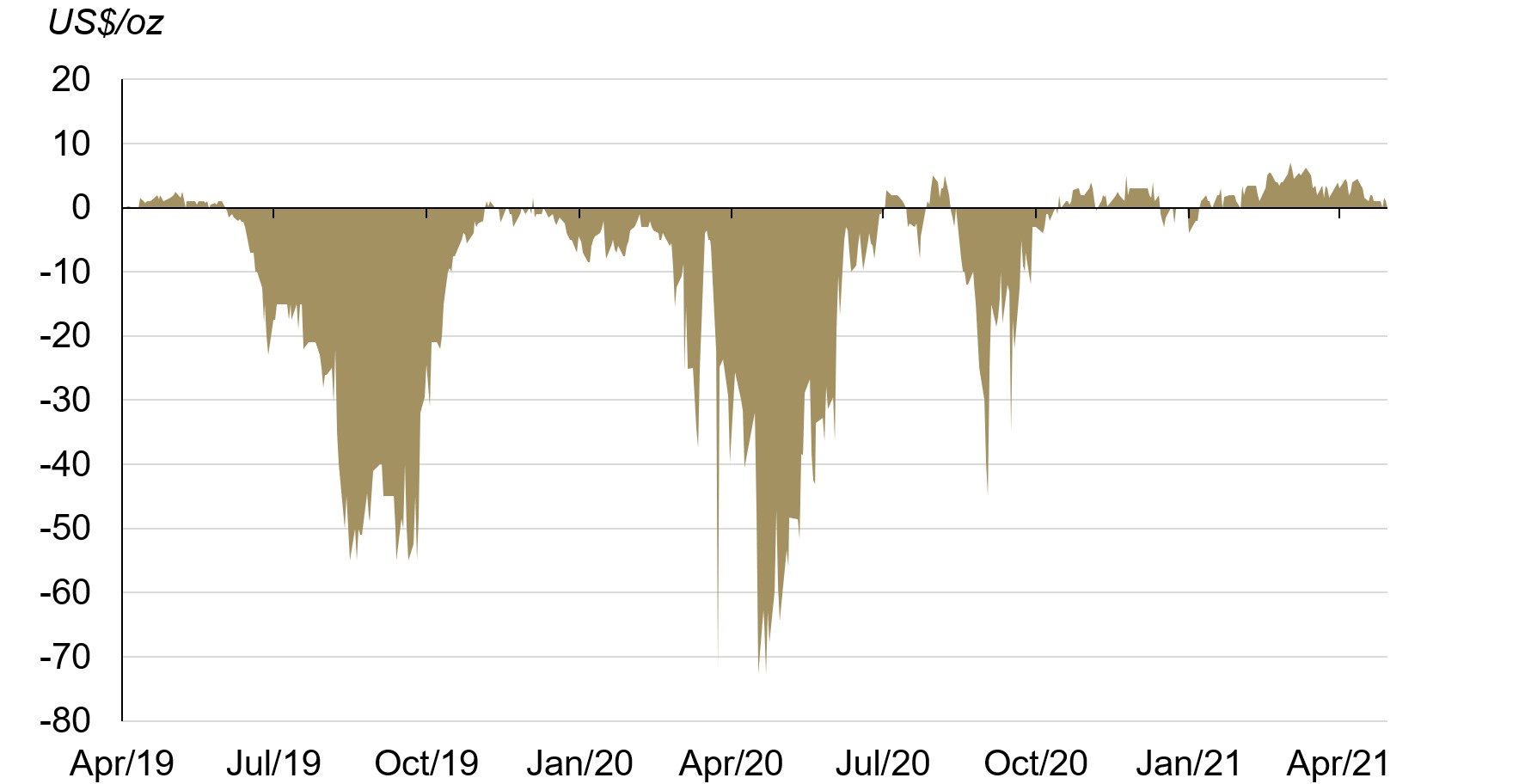

Local market premium fell sharply in the month

The combination of higher imports and weak retail demand led to a sharp fall in the domestic premium with local market trading at par by end of the month compared to a premium of US$3-4/oz at the beginning of the month (Chart 6).6 In early May the local market returned to discount amid weak retail demand and by the third week of the month the discount had increased to US$5-6/oz.

Chart 6: Local market premium fell sharply in April

Difference between MCX Gold Spot price and landed gold price in India derived from LBMA Gold price AM

Source: NCDEX, World Gold Council

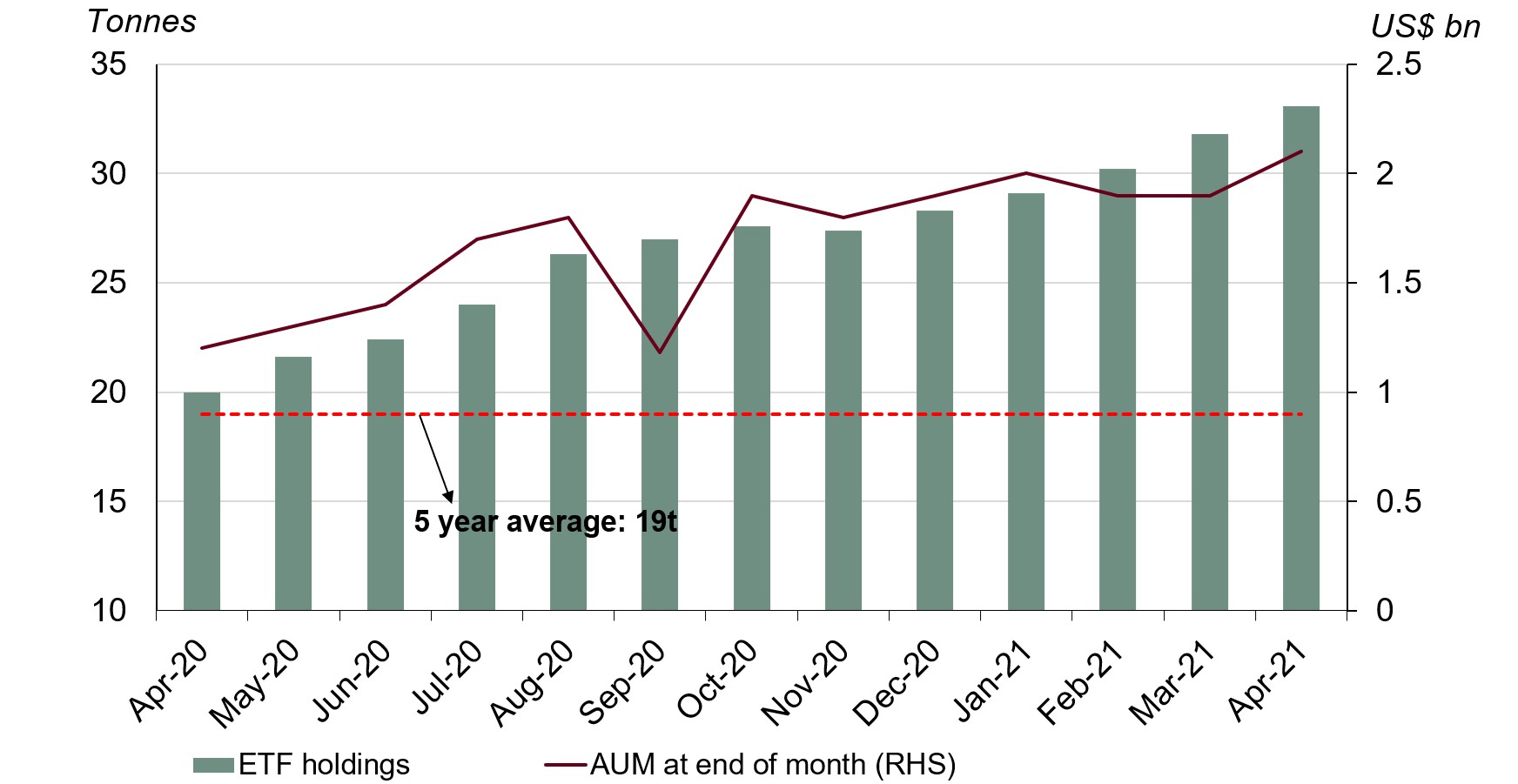

Gold ETFs continued to attract inflows

Against a backdrop of surging COVID-19 cases, the BSE SENSEX fell 1.45% during the month. Volatility in the BSE SENSEX hit 13.34% in April, higher than the MSCI US (8.17%)7 and this led to renewed safe-haven demand through gold ETFs. Inflows increased by 1.3t (Rs6.80bn; US$84mn) during April, taking total gold ETF holdings to 33.1t (Chart 7).

Chart 7: Indian gold ETF holdings reached 33.1t by the end of the month

Source: Respective ETF providers, Bloomberg, World Gold Council

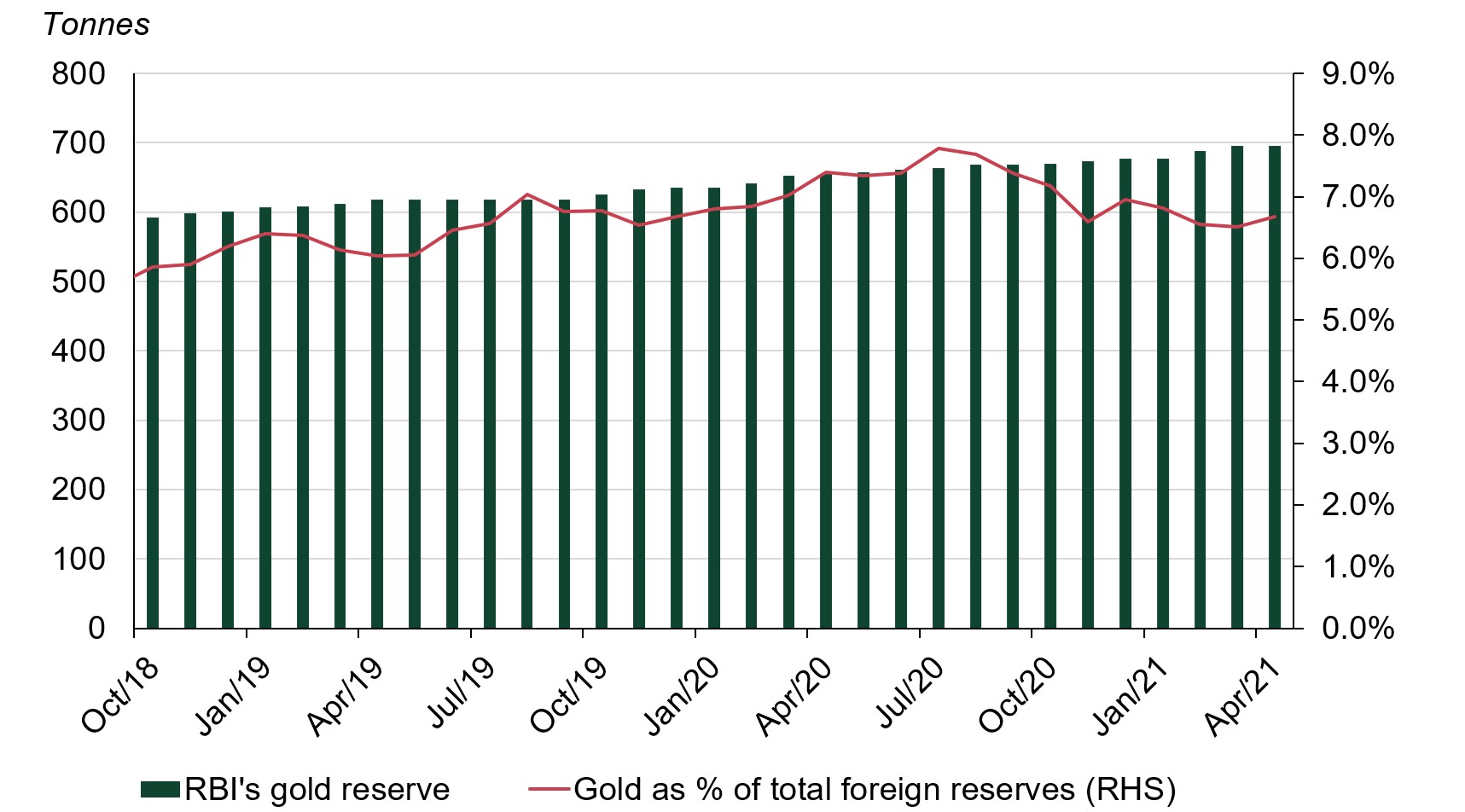

RBI made no gold purchases in April

After 7.5t of purchases during March, the RBI bought no further gold in April, maintaining its gold reserves at 695.3t or 6.7% of total reserves (Chart 8).8 The RBI has stepped up gold purchases over recent years and has added 18.7t to its gold reserves y-t-d.

Chart 8: RBI made no gold purchases in April

Source: IMF, RBI, World Gold Council

Footnotes

Based on MCX Gold Spot price in rupees as of 30 April 2021

We compare the LBMA Gold Price AM with MCX Gold Spot price as their trading hours are closer to each other than the most commonly referenced LBMA Gold Price PM.

An E-Way bill is an electronic bill for movement of goods and is generated on the E-Way Bill Portal. A GST registered person cannot transport goods in a vehicle without an E-Way bill if the value of goods exceeds Rs50,000.

Custom Tariff value in US$/10gm is published by Central Board of Indirect Taxes and Customs each fortnight based on the international gold price. Custom duty on gold is levied on custom tariff value and hence is a key component in determining the landed cost of gold in India.

FTWZ offers a distinct advantage as overseas suppliers can import gold into the custom-bonded warehouse of FTWZ without paying customs duty for authorised operations. Imported gold can be stored in FTWZ for a long period – as long as the letter of approval (LOA) is valid – thus reducing the logistics time in supplying to the domestic market as compared to importing from the overseas market.

The premia/discount data is based on Gold premium polled spot price from National Commodity & Derivatives Exchange Ltd

Gold Price Volatility from Goldhub; one-month volatility as of April 2021. We are using end-of-day VALUE i.e. BSE SENSEX and MSCI US for our volatility calculations.

Central Bank data is taken from IMF-IFS; IFS up until March and weekly statistics from the RBI for April. Please refer to our latest Central Bank Statistics https://www.gold.org/goldhub/data/monthly-central-bank-statistics.