The Australian central bank aims to keep rates low

Like many other regions, the Australian central bank lowered its policy rate last year to battle the COVID-19 economic fallout. After rate cuts in both March and November 2020, Australia’s benchmark interest rate reached a record low of 0.1%. In its latest monetary policy decision statement on 2 March 2021, the Reserve Bank of Australia (RBA) reiterated its accommodative monetary policy stance and reaffirmed its intention to maintain the current policy rate until inflation reaches its target – something not likely to happen until 2024 by the bank’s own assessment.1 Meanwhile, the RBA also vowed to keep its three-year treasury yield under its pre-set target of 0.1% to keep the economy’s borrowing cost low.2

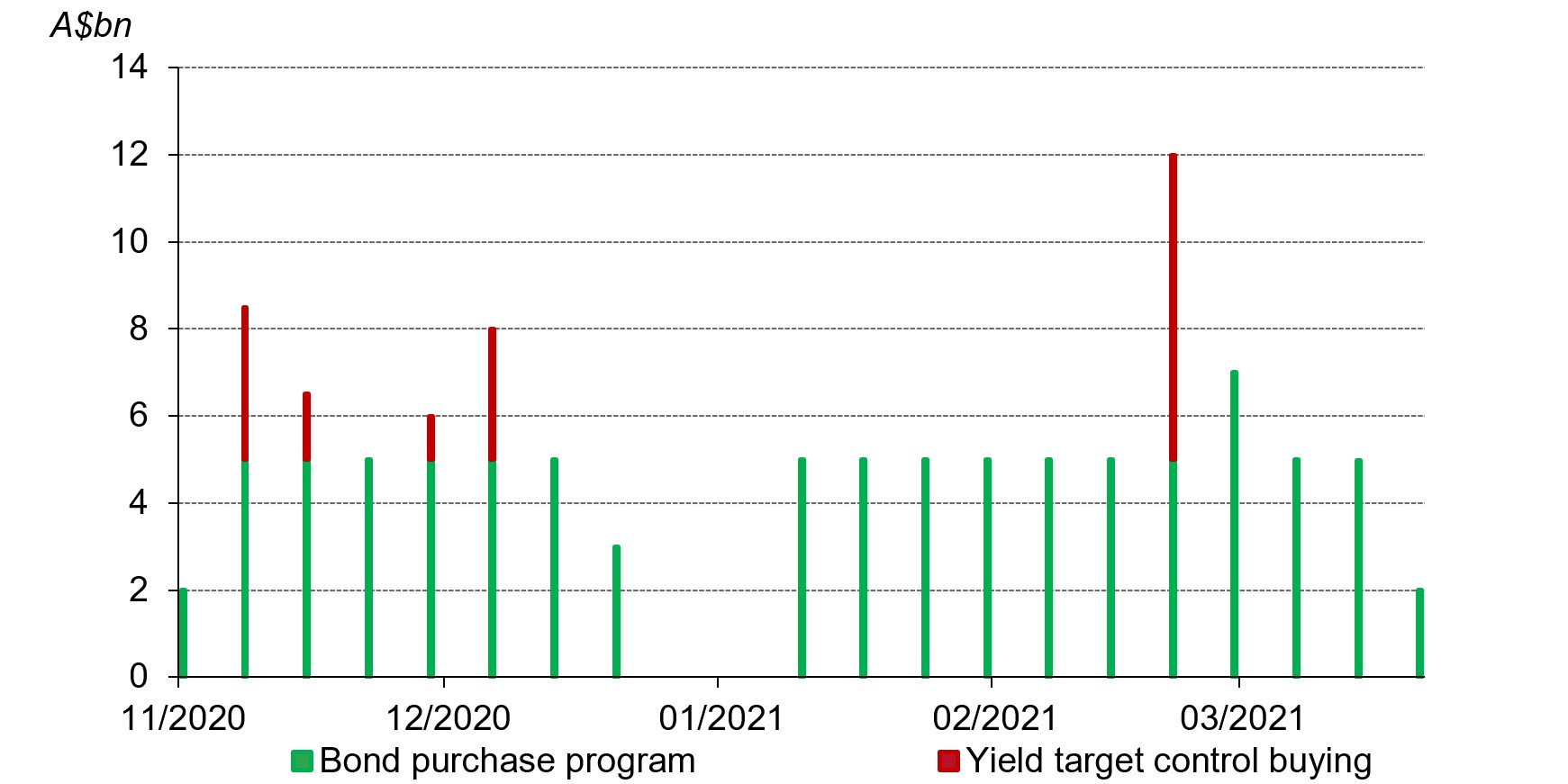

The RBA’s aim of maintaining Australian treasury yields within target is clear. In February, US treasury yields climbed rapidly amid global economic recovery and rising inflation expectations. Similar movements in treasury yields were seen in other markets, including Australia. In response, the RBA increased its bond-purchasing efforts. And it was reported that the Australian central bank also lifted the cost to short government bonds.

The RBA has been increasing its bond-purchasing efforts*

Weekly bond purchase under RBA's QE program (green) and additional purchase (red) to strengthen its three-year yield control

Source: Reserve Bank of Australia, World Gold Council

*Data based on the RBA’s bond purchase program statistics between 1 November and 22 March 2021.

Furthermore, Philip Lowe, the Governor of the RBA, stated in his recent speech that:

- The RBA will continue to keep the economy’s financing costs very low for as long as necessary

- While the current market expectations imply an early increase in the target rate, the RBA holds the belief that the economic conditions will not be able to meet its rate-hiking criteria until 2024

- The RBA will consider extending its bond purchase program further and will act to keep treasury yields low.

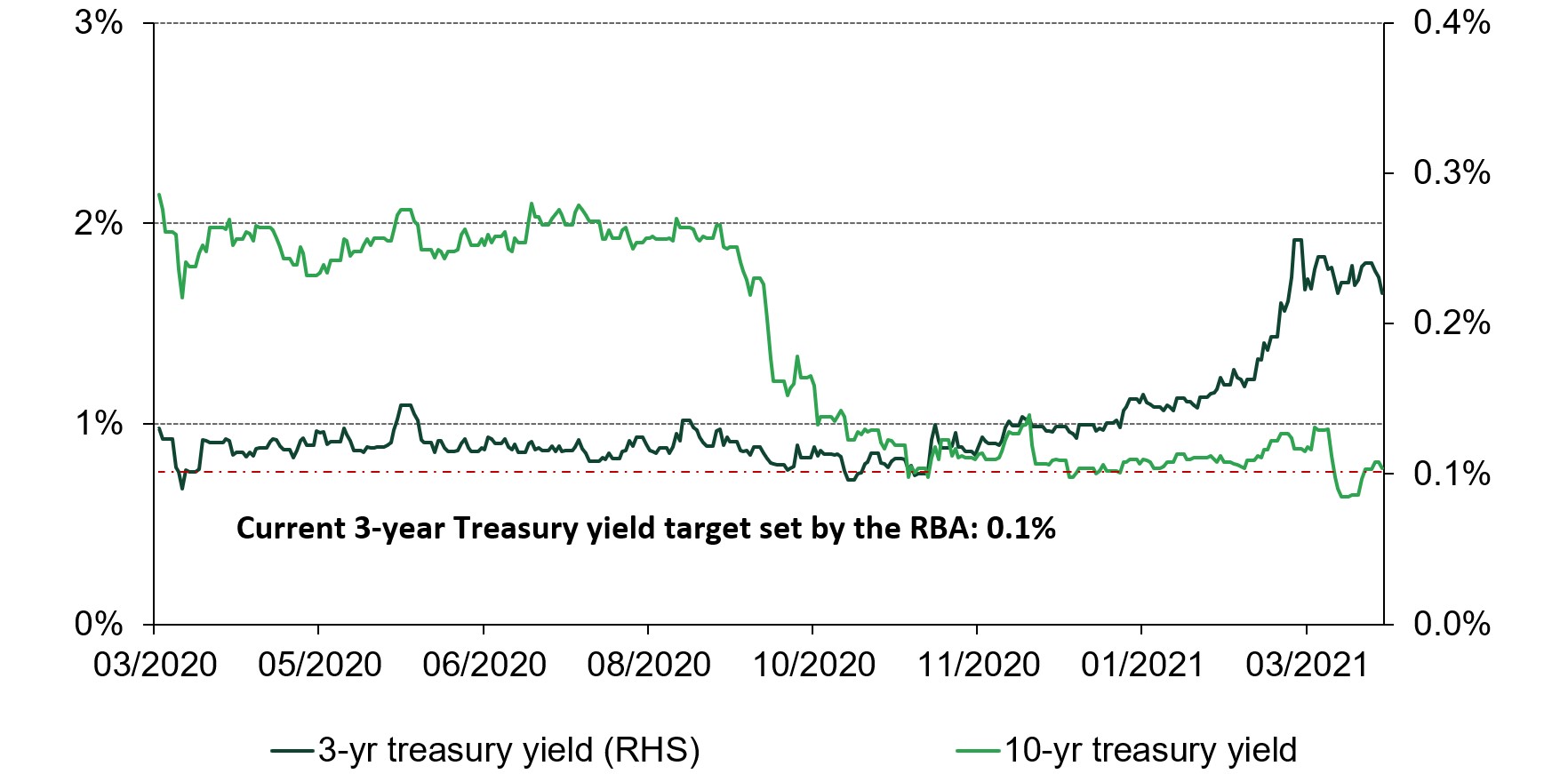

So far, the RBA’s yield curve control efforts seem to have been successful. The 10-year Australian treasury yield has dropped by more than 26 basis points since February, and the three-year Australian treasury yield moved below the RBA’s target of 0.1% in March for the first time this year.3

Australian treasury yields saw declines after their surge in February*

Source: Bloomberg, Reserve Bank of Australia, World Gold Council

*Based on daily yield movements between 3/24/2020 and 3/24/2021

The low-return environment for Australian super funds

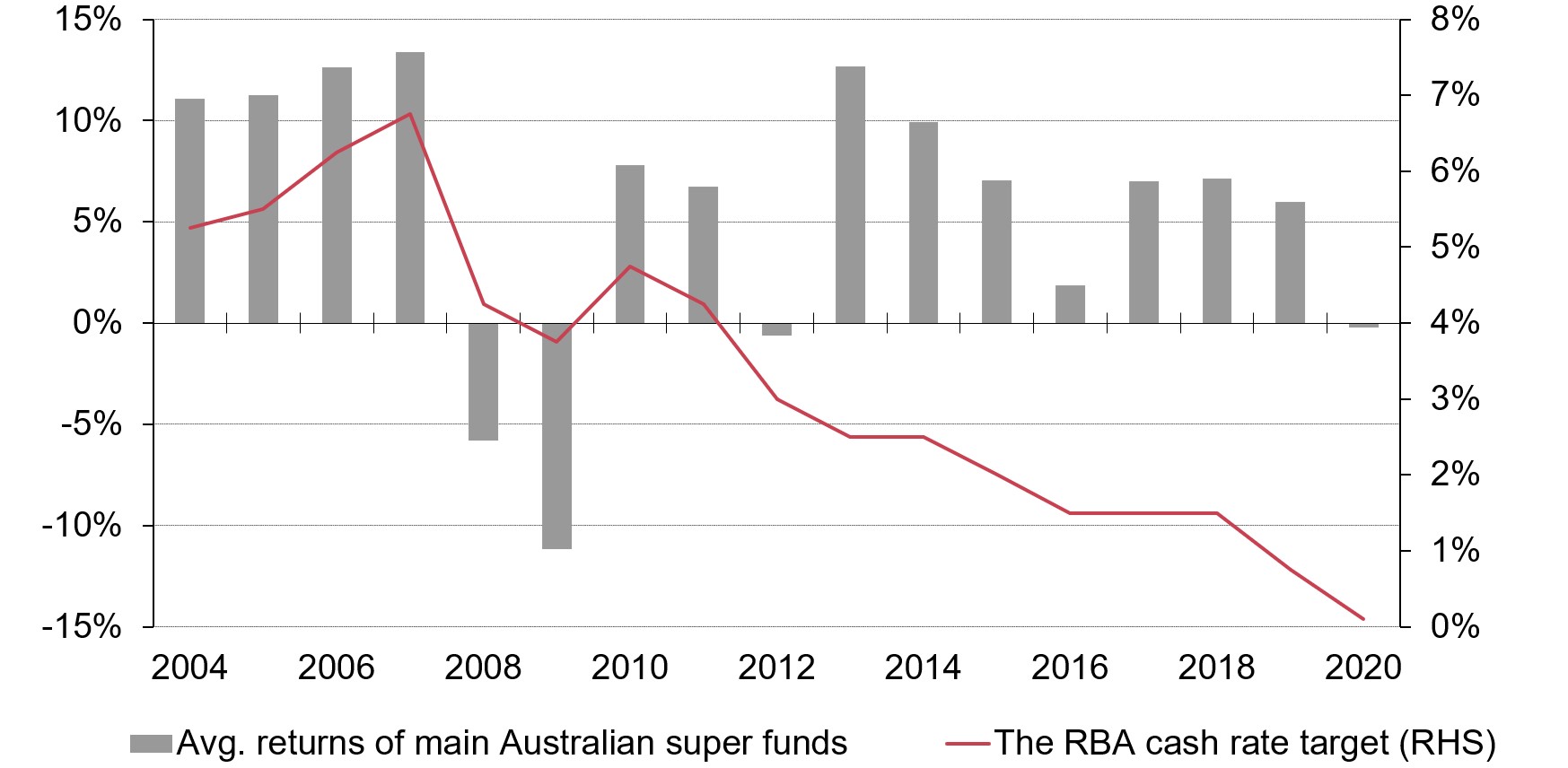

Lower interest rates in Australia have created challenges for asset managers. To combat economic slowdown and declining inflation, the RBA made 15 rate cuts between 2011 and 2020, bringing its interest rate to the lowest ever. And this low-rate environment has been weighing on the region’s treasury yields and local super fund – which, on average, allocates 31% of its assets to fixed-income and cash equivalent products – returns.4

Super funds' average returns have been dropping in tandem with the policy rate*

Average annual returns of 150+ Australian super funds (bar) and the RBA's cash rate target (line)

Source: Australian Prudential Regulation Authority, Reserve Bank of Australia, World Gold Council

*Note: the average returns of super funds refer to the annual average actual returns of over 150 Australian super funds tracked by the Australian Prudential Regulation Authority.

Gold: a return-generating asset in low-rate environments

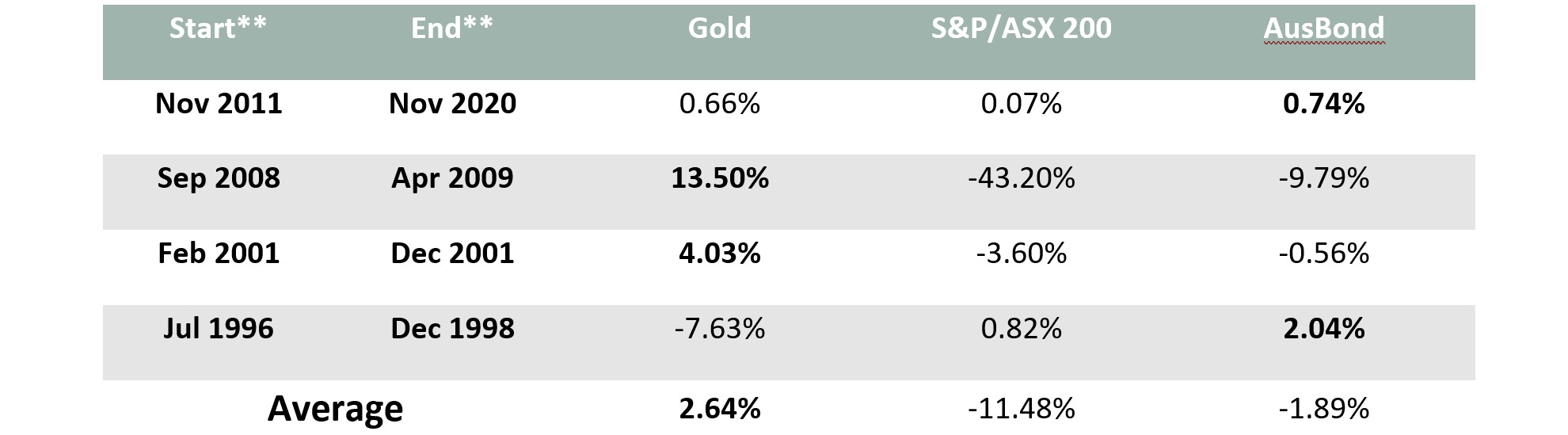

Historical data shows that gold has offered attractive returns during Australia’s monetary-easing and post-easing cycles. In four rate-cutting cycles since 1990, gold in Australian dollars averaged an annualised return of 2.6%, outperforming other major assets.

Gold in Australian dollars performed well during easing cycles*

Source: Bloomberg, World Gold Council

* All returns are compound annualised growth rates based on daily data in AUD of the LBMA Gold Price AM, S&P/ASX 200 Total Return Index and Bloomberg Composite AusBond 0yrs+ Index.

** “Start” means the first rate cut following a rate hike and “end” means the last cut in the rate cutting cycle before the next rate hike.

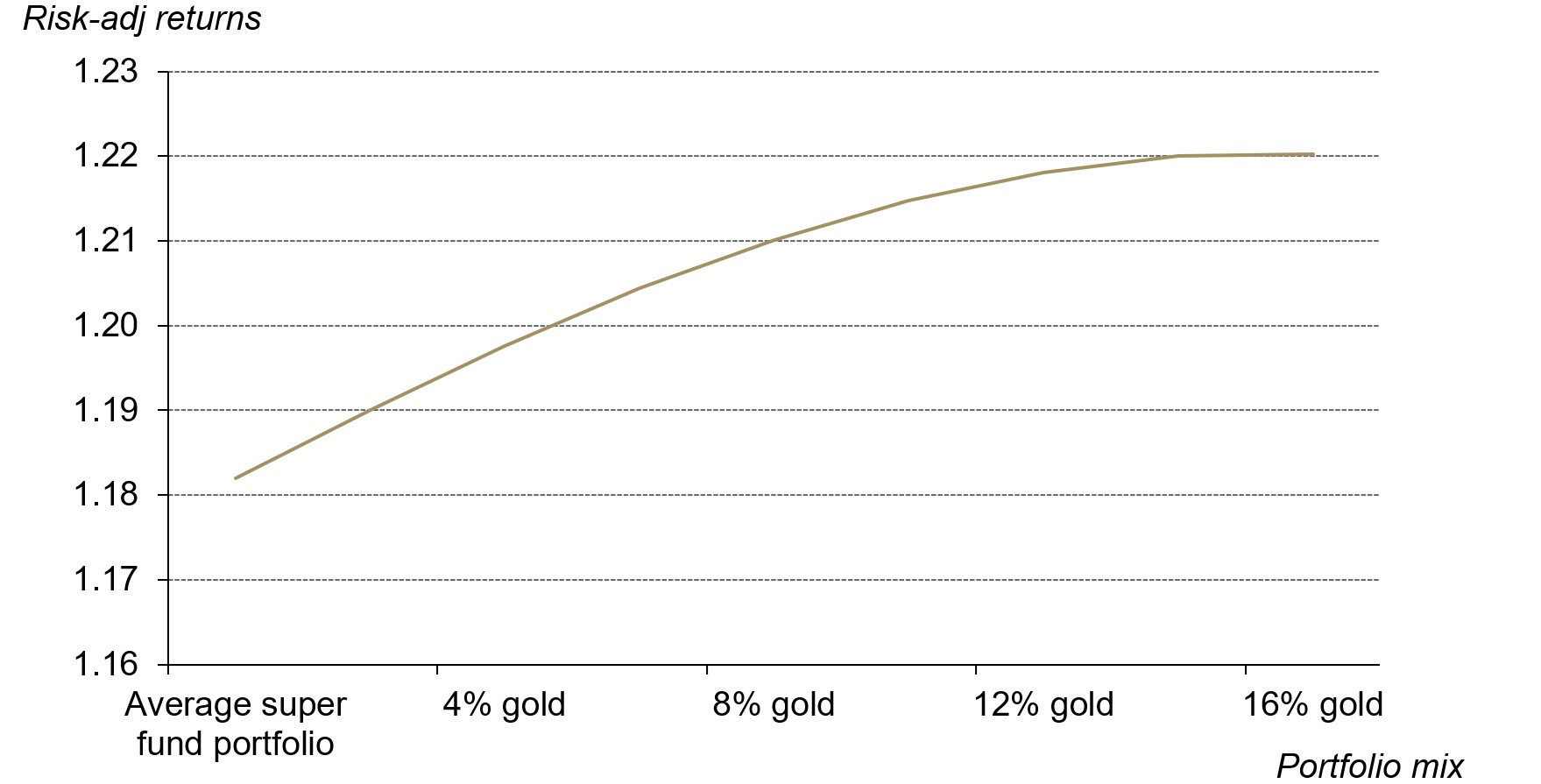

Our analysis also shows that an average Australian super fund portfolio’s risk-adjusted return could benefit from allocating a portion of its assets to gold during these cycles. For instance, by allocating 2%~16% of its assets to gold, an average Australian super fund would have enjoyed higher risk-adjusted returns during the latest easing cycle between November 2011 and November 2020.

An average Australian super fund portfolio could benefit from allocations to gold*

Risk-adjusted returns of an average super fund portfolio with different allocation to gold

Source: Australian Prudential Regulation Authority, Bloomberg, World Gold Council

* Based on monthly total returns from 30 November 2011 to 30 November 2020. The hypothetical average Australian superannuation fund portfolio is based on the average Australian super funds’ asset allocation in 2020 according to the Australian Prudential Regulation Authority’s superannuation asset allocation update. It includes annually rebalanced total returns in AUD of a 50% allocation to equities (21% S&P/ASX 200 Total Return, 25% MSCI World ex Australia Net Total Return and 4% Australia Public Unit Trust Unlisted Equity Trusts), 21% allocation to fixed income (12% Bloomberg AusBond 1+ Year Index and 9% Bloomberg Barclays Global Aggregate ex Australia Total Return Index), 12% allocation to cash products (Bloomberg AusBond Bank Bill Index) and 17% to alternative assets (8% S&P/ASX 200 A-REIT, 6% MSCI Australia Infrastructure Net Total Return Index and 3% Eurekahedge Australia New Zealand Hedge Fund Index).

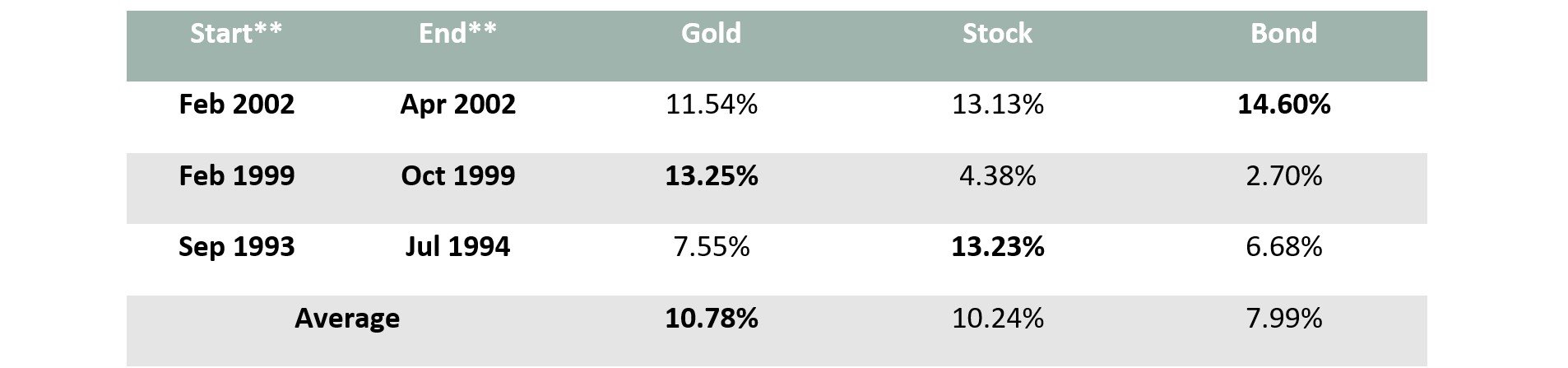

Gold also performed well during post-easing cycles in Australia. On average, gold in AUD has provided an average annualised return of 11% during the RBA’s post-easing cycles between 1990 and present, higher than stocks and bonds.

Gold can also generate sizable returns during post-easing cycles*

Source: Bloomberg, World Gold Council

* All returns are compound annualised growth rates based on daily data in AUD of the LBMA Gold Price AM, S&P/ASX 200 Total Return Index and Bloomberg Composite AusBond 0yrs+ Index.

** “Start” means the last rate cut in the last easing cycle and “end” means the first rate hike in the next tightening cycle .

Gold’s relevance as a strategic asset in Australia

Gold’s ability to generate returns during the monetary-easing and post-easing cycles in Australia stand on two legs. First, as we highlighted in The relevance of gold as a strategic asset in Australia, opportunity cost constitutes one of the four key drivers for gold’s local performance. With yields on assets such as Australian treasury notes declining drastically over the past decade, the opportunity cost of holding gold in Australia fell to almost zero, supporting gold’s performance in Australian dollars.

Second, gold has a global and diversified market. While Australia is one of the largest gold producers in the world, between 2010 and 2019 its mined gold production accounted for less than 9% of the global total on average. In fact, gold is produced on almost every continent and such geographical dispersion has brought stability to the gold market.

Gold’s demand is also diversified. It is purchased by consumers, investors and various industries as accessories, a safe-haven asset and a technology component. In 2020, when consumer demand for gold was hampered by the global economic fallout from COVID-19, investment demand for gold – including sales of gold bars and coins as well as gold ETF inflows – surged, limiting the volatility in global gold demand and underpinning gold’s stable performance in all regions.

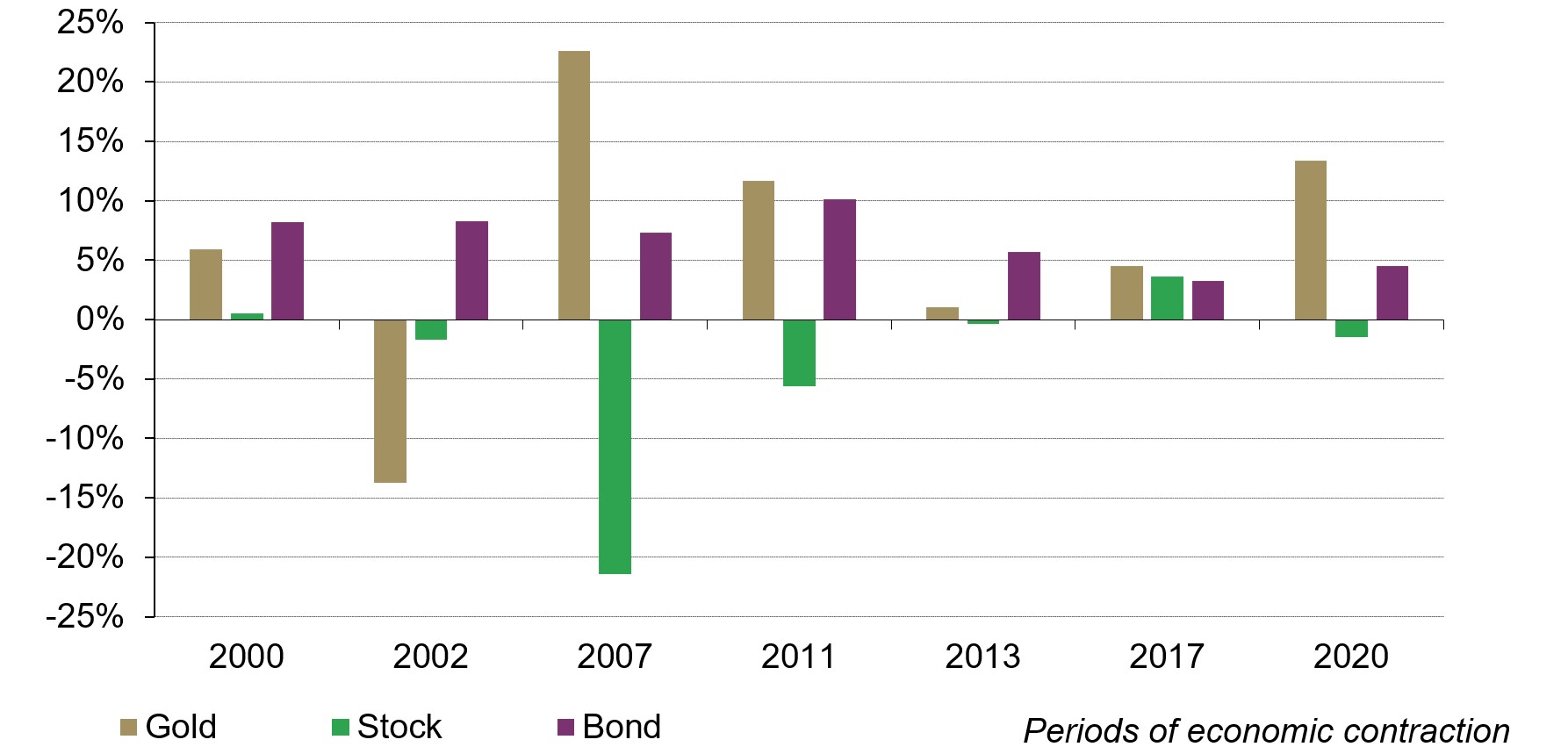

Gold’s global and diversified supply and demand dynamics resulted in its low dependence on changes in the Australian economy. In Australian dollars, gold has offered an average compound annualised return of 6.5% during the region’s economic contractions.

Gold has performed well during Australian economic contractions*

Compound annualised returns of assets during economic contractions in Australia since 2000**

Source: Bloomberg, Melbourne Institute, World Gold Council

*Compound annualised growth returns based on daily data in Australian dollars of the LBMA Gold Price AM, S&P/ASX 200 Index and Bloomberg AusBond 0yrs+ Composite Index.

** Dates: 6/2000-11/2001, 11/2002-6/2003, 5/2007-5/2009, 1/2011-8/2012, 8/2013-3/2016, 1/2017-6/2017, 12/2019-12/2020 Economic contractions as defined by the Melbourne Institute, for more detailed information, please visit Phases of business cycles in Australia: Melbourne Institute.

Conclusion

Globally, central banks have responded to the turbulence in bond markets. The US, Europe, Japan and India have kept borrowing costs low to accommodate economic recoveries, while the RBA increased its efforts to cap treasury yields. Reportedly, the RBA is not expecting its current policy rate and three-year treasury yield target of 0.1% to change until 2024. And as mentioned in our 2021 Gold Outlook, while this global low-rate environment could prevail, other risks such as ballooning budget deficits, inflationary pressures and potential market corrections amid lofty valuation might also negatively impact investors’ portfolio returns.

Against this backdrop gold may offer investors a source of returns and effective diversification. As previously mentioned, in historical periods of economic contraction and low rates gold has generated relatively attractive returns compared to stocks and bonds, and improved risk-adjusted returns for Australian investors.

Footnotes

Statement by Philip Lowe, Governor: Monetary Policy Decision, RBA, 2 March 2021.

Introduced in March 2020 to lower the economy’s borrowing cost, an initial 3-year treasury yield target of 0.25% was set by the RBA. It was reduced to 0.1% in November 2020 alongside the policy rate cut.

10-year Australian Treasury yield’s change based on the difference between 26 February 2021- the last trading day of February – and 24 March 2021.

Based on the average asset allocation of over 180 Australian super funds’ between December 2019 and December 2020 according to the Australian Prudential Regulation Authority’s website.