India’s gold market is steeped in tradition and still highly fragmented. However, over the last few years the industry has become more organised and regulated. Although small independent retailers still dominate the landscape, the market share of chain stores (national and regional) has increased steadily during the last decade. 1

In contrast to the retail jewellery trade, changes at the manufacturing level have been much slower. While manufacturers are becoming more organised, driven by growing demand from chain stores and tighter regulatory requirements (such as pollution licences), artisans still dominate Indian gold jewellery fabrication. 2 But as the gold market continues to develop, organised retail and manufacturing operations will see their market share grow.

Gold jewellery business in India

The gold industry is integral to the Indian economy, contributing 1.3% to Indian GDP. 3 But it is still fragmented – dominated by small and medium-sized enterprises. Over the last decade, the retail jewellery market has undergone a notable shift , driven by changes in consumer behaviour and government regulations designed to encourage the industry to become more organised.

The advent of chain stores in the last 10-15 years and their gradual gain of market share at the expense of stand-alone retailers has been notable. And this market share continues to increase up 5% since 2016 and representing a 35% share of the market by 2021. 4 The competition fostered by such rapid expansion has encouraged innovation; jewellers are now focusing on product offerings that provide both value and diversity to India’s wide cultural and demographic customer base.

Chain stores, with national operations, focus on daily wear and fast-moving jewellery items (such as chains and rings) and these items account for 50-60% of their business. Stand-alone and medium-sized retailers tend to focus on three elements: bridal jewellery (accounting for 60-65% of their business), customisation, and personal relationships with customers.5

Financing remains a crucial challenge for the industry

One of the biggest challenges for the Indian gem and jewellery industry has been securing bank credit – a challenge that has increased in the wake of the Nirav Modi, Mehul Choksi scam when the Indian banking system was defrauded of around Rs130bn (US$2bn). 6

Compounding this, more than 20% of loans given to the sector have become non-performing assets (NPAs), resulting in the gem and jewellery industry gaining just 2.7% of India's total credit issuance. 7

Securing bank finance is especially challenging for smaller independent jewellers who either tend to rely on the monthly gold scheme for funding or who act as money lenders, using that money for financing. One of the key factors preventing smaller jewellers’ access to capital is that most deal in cash and so do not report the full extent of their turnover in their accounts. Many have been unable to keep pace with the recent introduction of transparency measures and regulations and, as a result, their businesses have failed.

The jewellery manufacturing landscape in India

India’s manufacturing industry remains fragmented and unorganised. Only 15-20% of units operate as organised and large-scale facilities; this was less than 10% some five years ago. 55% of manufactured jewellery is handmade by karigars (artisans) who produce intricate pieces, thus sustaining the unique selling point for which Indian gold jewellery is renowned in the global market.8 While karigars form the backbone of the Indian gem and jewellery industry, many work in very poor conditions and a large number are underpaid as compared to many other industries, earning between Rs15,000-16,000 (US$190-200) per month.9

Mandatory hallmarking became effective on 16 June 2021 and applies to six purities: 14k, 18k, 20k, 22k, 23k and 24k. Its introduction will create a level playing field in terms of purity and enable retailers to focus on differentiation through design and customer service. These moves are likely to remove some of the barriers to purchase among young consumers, which in turn should support demand.

Looking ahead

National and regional chain stores will continue to gain market share because of their access to credit and the large inventory they are able to carry. And as many of these players look to open businesses in Tier 3 and Tier 4 cities, they should find a certain level of aspirational demand that they can tap into, allowing them to gain market share quickly. Conversely, if smaller players are not able to meet accepted standards of transparency their access to credit will be limited, as banks and financial institutions remain wary of lending to the gem and jewellery sector.

The manufacturing sector is just at the beginning of the journey to become more organised. Jewellery parks – some of which have already been established – will help manufacturers in this process and address some of the growing concerns among retailers and consumers about ethical standards and working conditions for artisans. As many large players limit themselves to working only with organised manufacturers, market share of organised manufacturers will continue to strengthen.

Retail market structure

India’s gold industry makes a significant contribution to its economy

The gold industry forms an integral part of the Indian economy, reflecting its significance as a key source of employment and foreign exchange earnings. The sector benefits from a large and vibrant market driven by strong domestic consumption and exports dominated by the Indian diaspora. India’s gold industry contributed 1.3% to Indian GDP and is dominated by small and medium enterprises. The domestic market is underpinned by culture, wedding and festive demand, which we will explore in more detail in an upcoming report.

Regulation and consumer preference have fuelled greater organisation and transparency in the industry

The retail jewellery market has undergone notable changes over the last decade, driven by evolving consumer preferences and government regulation that has encouraged the industry to become more organised. That said, a large part of the industry remains fragmented and dominated by independent retailers. There is no single industry definition to distinguish between unorganised and organised retailers. For the purpose of this analysis, Metals Focus has considered jewellers who sell gold via invoice, have proper banking channels and enterprise resource planning (ERP) systems in place, and are registered under the Bureau of Indian Standards (BIS) as organised jewellers. 10

Over the last few years demonetisation and the introduction of the Goods and Services Tax (GST) have helped the industry to become more organised and therefore more transparent (Focus 1). In response to these regulatory changes, many jewellers have adopted proper accounting software and now record sale proceeds via an official bill and maintain books of accounts. It is worth highlighting that the majority of jewellers in large cities and towns fall into the organised category. However, the unorganised sector remains a dominant force in rural centres, where many jewellers also act as moneylenders within their community.

Changing consumer preferences have also aided industry organisation. Consumers desire a better shopping experience, transparent pricing and buyback policies, and they want to purchase via bills and online transactions. It is thus not surprising that chain stores are gaining market share. In addition, a lot of what were regional players – such as Joyalukkas, Senco Gold and Diamonds, among others – have expanded to become national chains (Table 1).

Focus 1: Demonetisation and GST’s impact on the gold industry

Over the last few years, India has implemented several measures to formalise the Indian economy, streamline multiple taxes, improve tax compliance, and reduce dependency on cash transactions. The most notable among these are demonetisation (2016) and the implementation of the Goods and Services Tax (GST) in 2017.

I believe that the former gave an important push to the cashless economy, catalysing the growth of digital and banking transactions. Even though demonetisation severely hampered the unorganised sector over short to medium term, businesses and consumers have gradually adjusted to using digital transactions. The benefits of this will also continue to accrue over the coming years as more people become accustomed to this approach. The pandemic further accelerated the acceptance of digital transactions, and the fact that India saw close to 6bn Unified Payments Interface (UPI) transactions in July 2022 is testimony to its growing penetration and acceptance. UPI is a single platform that merges various banking services and features. It enables sending or receiving money and allows scanning a quick response (QR) code to pay an individual, a merchant or a service provider.

Turning to the GST, this was a landmark tax reform in India as it combined several taxes into one and standardised tax rates in India for most products, which helped to reduce business costs. In my opinion, this benefited interstate business transactions the most as different states operated varying tax structures before the GST, which subsumed several of those taxes.

Focusing on the impact of GST on the jewellery trade, the most notable outcome is how it has changed the way manufacturers and retailers transact with each other. Before GST, retailers like us depended on a mix of job work (providing their own metal for fabrication) and outright purchases of jewellery from the same karigars (artisans) and manufacturers. Under the GST, both are now separate transactions and attract GST. As a result, the retailer now either completely relies on job work or makes outright jewellery purchases from a fabricator. Furthermore, to avoid complexities, a large part of the bullion now remains on the manufacturers' books as many retailers prefer to procure jewellery stock directly from fabricators.

That said, the GST has made operations simpler, even for retailers buying their own bullion and then passing it on for job work. With local levies such as VAT eliminated, we can now purchase bullion from any state, taking into account the ease of logistics. For instance, as a retailer in Mumbai I can source bullion in Coimbatore and pass it on to the fabricator there or buy bullion in Mumbai if prices are competitive and then ship it to the fabricator located anywhere in India without worrying about multiple state taxes. In addition, the fact that many bullion dealers have now launched online apps has introduced greater pricing transparency, adding to the convenience for retailers such as myself willing to take bullion on our own books. This has also allowed retailers to secure a better price for our bullion purchases.

In terms of other benefits, we see the GST has helped formalise the trade while hampering the unofficial market. This is because every entity across the value chain must comply with GST to benefit from the input tax credit. To briefly explain this, only the final consumer pays the GST while companies across the value chain (bullion dealers, manufacturers, wholesalers, retailers) simply collect GST and offset the input tax credit against the tax on the outward supply of good and services. While the GST has benefitted the jewellery trade, in my view several challenges remain. Among them is the increased cost of compliance for the sector. This is especially true for small retailers and manufacturers who now must hire dedicated staff to comply with GST accounting and filing and so must invest in systems to ensure proper record keeping. Even for large retailers like us, staff and system requirements have increased, with the estimated additional cost of compliance of around 5-10% for a large part of the industry.

That apart, I believe that the GST has negatively impacted retail gold bar and coin purchases. Indian consumers traditionally accumulate gold over a period of time, which is converted into jewellery at a later date, for example for weddings. Metals Focus estimates that 30-40% of bars and coins have traditionally been converted into jewellery in this way. Under the GST regime, a consumer pays 3% at the time of buying a bar or coin and then pays a further 3% GST on jewellery using that bullion (unless this happens within six months of bullion purchase, in which case an offset is possible). With no offset of GST for the consumer when exchanging their bullion for jewellery, the consumer effectively pays double the tax. Another anomaly within the GST framework is that when an individual provides bullion for job work, he has to pay 18% GST on the making charges (labour charges), while a registered dealer carrying out the same transaction has to pay just 5% GST. I believe this must be addressed to bring the consumer on par in terms of taxation.

As a result of this double taxation on consumers, there has been a slow shift away from bar and coin purchases at the retail level. To some extent, the Sovereign Gold Bond (SGB) may have benefitted from this. However, given that SGBs are not physically backed, they are not the ideal replacement. Also, SGBs are typically bought by urban Indians or more financially literate consumers.

Finally, I believe that a GST rate of 1.25% is the most ideal for the gold trade as the 3% rate applicable currently is high considering that gold is an investment asset. Also, given that the customs duty on gold is already high, bringing down the GST on a high value asset like gold should be considered by the government.

Ashish Pethe Partner, Waman Hari Pethe Jewellers Chairman, Gems and Jewellery Council (GJC) India

Table 1: Top 10 chain stores in India

Name

Stores

Cities/Towns

Tanishq (including Zoya)

382

209

Malabar Gold and Diamonds

150

111

Senco Gold and Diamonds

126

85

Kalyan Jewellers

116

87

Reliance Jewels

99

85

Joyallukas

85

67

PC Jewellers

82

68

Shubh Jewellers

82

N/A*

PC Chandra Jewellers

57

50

Orra Jewellery

58

25

* Not available Source: Metals Focus, World Gold Council

Chain stores have gained market share at the expense of stand-alone retailers

One of the most significant changes in the jewellery market over the last 10-15 years has been the advent of chain stores and the market share they have gained at the expense of stand-alone retailers. According to market intelligence from Metals Focus, by 2021 chain stores (both national and regional) had achieved a 35% market share (Chart 1). 11

Since 2016, chain stores have increased their market share by 5%. Demand for better designs and consumer experience, a growing awareness about hallmarking, better pricing structures and competitive return policies, as well as the introduction of GST and demonetisation, have all accelerated the shift towards chain stores.

Chart 1: Jewellery market landscape in India

Jewellery Market Structure 2022: Chart 1

Data as of

Sources:

Metals Focus,

World Gold Council; Disclaimer

Most gains have been in large cities and towns. But here, chain stores may be nearing a ceiling for expansion as independent retailers catch up with the need for a heightened consumer experience and customer-led designs. Chain stores are therefore shifting their focus to Tier 2 and Tier 3 cities, where there remains aspirational consumer demand ready to be tapped. Metals Focus estimates that over the next five years or so chain stores will continue to expand and their market share will surpass 40%. The top five retailers alone will likely open 800-1,000 stores during this timeframe.

It is also worth highlighting that many jewellers have changed category over the past five years as their businesses have expanded and they have gained market share. For example, Senco Gold and Diamonds – previously considered a regional chain – now operates in more than 13 states and is categorised as a national chain. Furthermore, many stand-alone retailers with prominent brand names have expanded their stores or opened new ones in their region and are now classified as medium-sized retailers.

Customer focus and product offerings are a key differentiation

Given India’s geographic, regional and cultural diversity, it is not surprising that different jewellers focus on different customer segments and product offerings. For example, chain stores – mainly those with national operations – focus on everyday wear and fast-moving jewellery items (such as chains and rings); about 50-60% of their business comes from these products. A focus on everyday wear has helped them gain market share as they can maintain a high inventory and offer a wide choice to consumers. In contrast, regional chains try to build a competitive advantage by focusing on the preferences of their local consumers.

Stand-alone retailers initially struggled to compete with chain stores but the adoption of better practices has allowed them to co-exist in the highly competitive landscape (Focus 2). Stand-alone and medium-sized retailers tend to focus on three elements: bridal jewellery, customisation, and developing personal relationships with their customers (Table 2). Bridal jewellery accounts for 60-65% of this sector’s business; customisation helps improve profit margins, and shop owners and family members – who are involved in the business and are customer facing – develop and maintain solid customer relationships.

The gold jewellery retail market is highly fragmented

The fragmented nature of the industry makes it almost impossible to accurately quantify the number of jewellers in India. Estimates by various trade bodies vary considerably, ranging between 500,000-600,000.

Metals Focus looked at several data sources to better inform their estimates as to the size of the market.

According to numbers released by the Goods and Services Tax (GST) Council, around 86,000 jewellers have registered for taxation purposes, which is mandatory for any jeweller with an annual turnover above Rs4m (US$50,000).12

Table 2: Size of retail shop, stocks and employees

Stand-alone/Independent retailers

Medium sized retailers

Regional chains

National chains

Organised

✓

✓

Unorganised

✓

✓

Distinctive feature

Caters to the market where customers make purchases based on price

This can include family retailers. The focus is on the traditional market

The focus is on local trends and designs. The differentiator is purity and trust.

The focus is on brands and purity. Typically, these chains have high making charges

Shop size in sq ft

150-500

300-1,000

500-3,000

4,000-25,000

Inventory

<10kg

10-50kgs

51-150kgs

151-500kgs

Display in store (% of total stock)

40-50%

60%

80%

90%

Employees per store

4-5

1-15

20-35

40-60

Source: Metals Focus, World Gold Council

In 2021 the Indian government mandated mandatory hallmarking in 256 districts (out of 748) and any jeweller in these districts with turnover of more than Rs4m must register with the BIS to sell hallmarked jewellery. To date, 130,205 jewellers have registered with the BIS.13 Metals Focus also analysed a pan-India database of jewellers in large cities and towns (covering more than 1,200 locations). This database featured over 350,000 unique company names, but a deeper analysis of these statistics revealed that 25-30% sold only artificial jewellery. While India has roughly 4,000 towns, only 400 have a population of more than 100,000, and it is in these larger towns that most jewellers are based.14

There are also more than 600,000 villages in India where, until recently, it was widely believed that many had a local jeweller. 15 However, our research suggests that this is seldom the case and jewellery stores are usually located at the district or taluka (typically comprising several villages) level, or in towns with a Nagar Parishad (city council).16 A jeweller in a local village is usually referred to as either an artisan or a money lender. Furthermore, it is essential to highlight that a significant number of these jewellers focus on moneylending and are therefore likely to have annual gold sales below 1kg. As a result, to extrapolate the number of jewellers in India based on the number of villages is often misleading.

Based on this analysis, we estimate that the number of jewellers with meaningful businesses in precious metals in India is likely to be 300,000- 350,000. 17

Our industry interaction suggests that the top 500 jewellers dominate the entire jewellery landscape. 18 Collectively, these hold about 200-240t of product inventories. 19 While it is difficult to ascertain the total volume of gold in Indian jewellery stores, we have used the above inventory factor and our market intelligence to estimate the amount of stock in jewellery shops at 300-400t. 20

Financing remains a crucial challenge for future growth, especially for small jewellers

One of the biggest challenges for the Indian gems and jewellery industry has been securing bank credit, which has become even more difficult in the wake of the Nirav Modi, Mehul Choksi scam where the Indian banking system was defrauded of around Rs130bn (US$2bn).

According to the latest financial stability report from RBI, more than 20% of loans given to the sector have become non-performing assets (NPAs), second only to the construction sector. It is therefore not surprising that the gems and jewellery industry only accounts for 2.7% of India's total credit issuance, which is less than half that of the textile industry, India’s other key export-driven sector.21 As a result, it has become difficult for small and medium-sized jewellers to expand their businesses.

Even within the industry there is a significant difference between how a large or medium-sized jeweller obtains funding vis-à-vis smaller operations. Securing cash credit from banks is much easier for large and medium-sized businesses. This is because many of these jewellers have much more transparent accounts, making it easier for the bank to judge past and future performance. It is also possible for organised jewellers to avail themselves of gold metal loans from banks. Metals Focus estimates that outstanding gold metal loans were around 65t at the end of 2021.22

Focus 2: Structure of a stand-alone jewellery retailer

India's retail jewellery sector has witnessed a structural shift over the last decade. From a landscape dominated by single and family-owned stores, a notable portion of the industry is now run by chain stores operated by corporates. Moreover, from just a handful of organised retailers a decade back, India now has several large chains with a pan-India presence, with many others operating at the regional level. Amid all this, while single stores initially struggled to compete, many have adopted good practices and now co-exist in this highly competitive landscape.

Organised retailers with large stores and better access to bank finance can hold larger stocks and so can out-compete smaller and single-store retailers. These economies of scale also allow them to offer more competitive retail margins. Standalone retailers on the other hand have faced challenges in inventory management, funding and differentiation in products.

Over the last few years, the smaller retailer has taken on these challenges and is now better positioned in this new retail landscape. To start with, most of these stores are now focusing on specialisation and customisation as their unique selling proposition. For example, in the bridal segment, which is the largest area of gold demand in India, independent retailers have been able to compete, utilising their flexibility, better understanding of local customers and design sensibilities, customising jewellery pieces according to customer budgets, and offering flexibility even with payments. Overall, this strategy had a pronounced impact on their margins.

Furthermore, even in the daily wear segments, independent retailers are now offering customised solutions, which helps them to compete without the need for high stock levels.

In terms of bank finance, the larger standalone retailers have managed to access bank loans and working capital funding has helped many independent retailers to launch new stores. While the rate of interest and collateral is high, single-store retailers can now access banking finance. Those who choose not to inject capital have turned to working with lower inventory and focus on specialisation. Many of the single-store retailers have been in the business for generations and so can fund daily operations using their own funds, but this can restrict their growth due to limited capital for ploughing back into the business. In a scenario of limited available funding the monthly gold saving scheme also presents an important form of working capital for a jeweller. For many jewellers in small cities this makes up 20-30% of their sales, although in large cities the share is much smaller.

Regarding the buyback of old jewellery, there is little to separate industry practices across large parts of India, and so there is no specific advantage left with organised stores. Finally, with mandatory hallmarking, some of the traditional consumer apprehensions about the quality of the jewellery they are buying have eased, which will further benefit independent stand-alone retailers.

Jatin Chheda

Chheda Jewels

The other advantage that large, organised jewellers enjoy is credit from manufacturers. For many of the large jewellers, obtaining credit is essential to their operations. For example, discussions between Metals Focus and the trade revealed that jewellery retailers often enjoy between one and three months of credit from a fabricator, which helps them with inventory management and allows them to expand their operations by offering more products.

The other important means of funding, which we believe is unique to India, is the monthly investment scheme run by jewellers, which Metals Focus estimates accounts for 20-30% of their funding.23 This works as a monthly gold saving scheme where consumers deposit a specific amount of money with the jeweller for 11 months, with the jeweller then paying the consumer one month’s equivalent of their deposit as interest. At the end of the year the consumer chooses to buy gold jewellery or minted products with accumulated savings and interest.

In contrast to large and medium-sized jewellers, it is extremely difficult for small and independent jewellers to secure cash credit from banks; they either tend to rely on the monthly gold scheme for funding or they lend money. Most act as money lenders, offering loans against gold jewellery and charging customers annual interest of 18-30%. 24 This forms a large part of their business and if a consumer misses a couple of payments the interest rate can increase further, or the jewellery is retained. Unlike banks and non-banking financial corporations (NBFCs) where loan-to-value (LTV) is 90% as stipulated by the RBI, the LTV for jewellers is about 60-70%, offering them a better margin of safety and profitability.25

Many small jewellers have been in business for generations, during which time they have converted part of their profits into gold and re-routed that back into the business to help fund operations. However, this can restrict growth as there is only limited capital available to plough back into the business. One of the key reasons smaller jewellers find it hard to access capital is that most deal in cash and do not report total turnover in their accounts; this helps to explain why only a fraction of these jewellers are registered under GST. All the regulatory changes that have taken place over the last decade – including the requirement of a PAN card for transactions above Rs200,000 (US$2500), restrictions on cash transactions and, more importantly, demonetisation and the introduction of GST – have made it difficult for many smaller jewellers to remain in business. It is not surprising that many have closed their shops, especially those in large cities and towns.

Expansion of the gold metal loan market has been limited

The gold metal loan (GML) is a mechanism under which a jewellery manufacturer can borrow in gold instead of rupees. The loan is then settled in rupees (INR) with the eventual sales proceeds. Gold Metal Loans can be secured for 180 days in the case of domestic jewellery manufacturers and 270 days for exports. GMLs are provided by nominated banks (approved by the RBI), but only to jewellers who produce gold jewellery. Jewellers cannot sell the gold borrowed under the GML scheme to any other party to for the purposes of manufacturing jewellery.

According to the latest notification by the RBI, nominated banks authorised to import gold and designated banks participating in the Gold Monetisation Scheme (GMS) (2015) can extend GMLs to jewellery exporters or domestic manufacturers of gold jewellery.26 These loans are repaid in INR, equivalent to the value of the borrowed gold on the relevant dates.

Under this new notification, certain changes were made to the existing regulations:

i) Banks shall provide an option to the borrower to repay a part of the GML in physical gold in lots of one kilogram or more, provided:

the GML has been extended from locally sourced/GMS-linked gold

repayment is made using locally sourced India Good Delivery (IGD)/LBMA Good Delivery (LGD) gold

gold is delivered on behalf of the borrower to the bank directly by the refiner or a central agency acceptable to the bank, without the borrower’s involvement

ii) Banks shall continue to monitor the end use of funds lent under GML. While the size of the metal loan market has increased over the last ten years, growth and penetration have been slow, rising from 40-45t in 2002 to about 65t in 2021. In a scenario where funding is difficult for the industry, GMLs present a great opportunity to raise funding at low interest rates for medium and large manufacturers.27 However, due to the industry’s lack of transparency and the weak balance sheets of jewellery manufacturers, most are unable to take advantage of this option.

One issue that has impacted GMLs over the last few years has been the rise in gold prices. To understand the impact of higher gold prices it is necessary to understand how a GML works. A bank that wishes to provide a GML would decide on the local premium/discount and the rate of interest at which the loan would be granted; the price of gold will be fixed on the day the gold jewellery is sold. The borrower draws the GML with a stipulated initial margin. The exposure of the jeweller is then marked to market daily, and the jeweller is required to service the margin if the threshold limit is crossed. With gold prices increasing over the last two years, jewellers needed to service margin calls regularly, but a lack of funding impacted their working capital cycle. As a result, many jewellers have closed their metal loan accounts; we estimate that some 5-6t of loan accounts would have been closed due to this one issue. 28

Cash remains the preferred mode of payment

During research for this report Metals Focus visited more than 25 cities, and one common thread that stood out was that cash remains the preferred means of making a purchase, accounting for some 50-60% in metros and large cities and 70-80% across the rest of India, in terms of value. 29 According to the half-yearly Target Group Index (TGI) study conducted by Kantar for the World Gold Council, cash remained the dominant mode of payment for gold purchases, in terms of value, accounting for 67% in 2018 and 2019. Among cash purchasers of gold, females aged 35+ were the highest segment.

It is often believed that large cash transactions in the jewellery industry reflect a lack of transparency and that cash purchases are used to ‘park’ unaccounted income. However, it is important to put this into perspective: there is no denying that cash dominates purchases, but a large proportion of these transactions are not unaccounted purchases. First, the Metals Focus’ discussions revealed that 80-90% of all cash purchases at large retail stores are backed by an invoice and so both customs duty and GST are paid. Second, it is important to understand that 50-60% of gold purchases in India take place in rural locations. This is because a large section of the population in rural India is dependent on agriculture, which is exempt from tax. Furthermore, many consumers withdraw cash from their bank to buy jewellery as they do not want to share their bank details or are not comfortable with digital transactions. Since the money is already part of the banking system, it does not represent unaccounted cash and therefore all cash purchases cannot be deemed as unaccounted even though some jewellers do not record them in order to evade tax. The report of the Household Finance Committee by RBI mentioned that gold is a preferred asset for tax evasion purposes. The committee proposed that the PAN card requirement for gold transactions from jewellers should be extended to all transactions, and not just those above Rs200,000. To prevent the PAN card requirement from driving gold transactions underground, the committee recommended that all gold transactions should be registered using an electronic registry such as a depository. 30

Another key issue is the Merchant Discount Rate (MDR). Banks charge jewellers a fee for processing payments via credit or debit cards, usually ranging from 1-3%. This is high in the context of the price of gold and the low margins that jewellers receive compared to retailers in other industries.

Metals Focus’ trade feedback noted that if MDR charges were reduced to around 0.5% this would likely encourage many jewellers to shift towards card transactions. Current MDR charges mean that many jewellers either refuse card transactions or pass on the MDR charges to the customer. This deters consumer purchases via card and encourages the use of cash. That said, many large and medium-sized jewellers have now started to renegotiate MDR with the banks and so have access to rates as low as 0.25-0.5%, which should help digital transactions going forward.

Other positive changes in payment behaviour have emerged over the last few years:

more cash transactions are being made via an official bill

digital transactions are increasing significantly, typically via the Unified Payment Interface (UPI) 31

consumers are becoming more comfortable with digital payment methods and with using credit or debit cards for high value purchases

Millennials drive online jewellery sales

The Indian online jewellery market has seen rapid growth over the last few years, driven by demand from millennials, growing internet penetration and a hike in smartphone sales. While Indian consumers still strongly prefer face-to-face when it comes to jewellery purchase, they were prevented from doing so during the pandemic. The lockdown restrictions and an aversion to going out in public saw many consumers switch to buying jewellery online, and this accelerated the pace of growth in the jewellery e-commerce market. The online market can be broken down into three segments: e-commerce platforms (such as Flipkart, Amazon and Snapdeal); specialised online jewellery retailers (such as CaratLane, BlueStone, Candere); and jewellery retailers with their own websites.

While the number of platforms offering gold jewellery has increased, Metals Focus estimates that the share of online sales remains in the order of 3-5% of total jewellery sales value. Most sales are driven by consumers aged between 18 and 45. Interestingly, while online jewellery purchases have risen, the average ticket size has not; most jewellery purchased online has remained between 5 and 10 grams.32 Online buyers tend to purchase lightweight daily wear/fashion jewellery in 18-carat gold.

Looking ahead, Metals Focus estimates that the market share of online jewellery in the next five years could increase to 7-10%. 33 This will be driven by greater online offerings from jewellers and a growing acceptance of online channels. Metals Focus forecasts that lightweight jewellery will continue to dominate online sales, with the average weight remaining in the 5-10 gram bracket.

Retailers have increasingly adopted advertising to drive sales

The last decade has seen two significant changes in the jewellery industry: increased competition and changes in consumer behaviour, leading many jewellers to adopt aggressive advertising to broaden their appeal. However, the advertising space is still dominated by chain stores and medium-sized jewellers that have a strong local presence.

It is important to understand how advertising methods have changed over the last few years. In the past, advertising was largely confined to print and electronic media (television), but today, websites, social media and outdoor (banners, hoardings and displays) are prevalent.

Social media marketing uses platforms like Google and Facebook to push products via keyword searches or promote products on channels such as Instagram. Most large jewellers, especially those focusing on bridal jewellery, have an Instagram account. In addition, many jewellers link up with social media influencers and celebrities to wear their products, upload on their pages and tag the jeweller. This is a popular option for jewellers who want to target younger consumers. In particular, Indian women aged 18 to 24 look to social media and influencers for inspiration in curating their choices: the India Influence Report 2018 found that 86% of the most viewed beauty videos on YouTube that year were made by influencers and, as a consequence, 62% of existing advertisers planned to increase their influencer budgets. 34

Large, organised retailers take marketing very seriously, allocating significant budgets. To give a sense of individual company spend, top branded jewellery chain Titan Company Limited increased its advertising expenditure from Rs380mn (US$6mn) in 2015 to Rs2,080mn (US$28.3mn) in 2021. Over the same period, Kalyan Jewellers increased its spend on advertising from Rs700mn (US$11mn) to Rs920mn (US$12.5mn). 35

Manufacturing market structure

Jewellery manufacturing remains fragmented but is slowly changing

Despite being one of the largest fabricators of gold jewellery globally, India’s manufacturing industry is fragmented and unorganised. Unlike jewellery retailing, which has become increasingly organised since the advent of corporate retailers such as Tanishq some 15 years ago, the manufacturing industry is still dominated by small jewellery workshops and artisans. While there is no official estimate on the number of manufacturers in India, and many operate independently as freelancers, industry estimates suggest there are 20,000-30,000 manufacturing units across the country.

Only a very limited number of manufacturers operate large-scale factories, although their numbers have increased over the years. Only 15-20% of units operate as organised and large-scale facilities; five years ago this was less than 10%. Metals Focus attributes this growth to three distinct factors: the expansion of organised retailing; a growth in exports; and a clampdown by authorities. Orders from overseas and domestically-organised retailers tend to be quite large and so cannot be fulfilled by small workshops. That aside, organised retailers and foreign buyers only tend to place orders with large players due to transparency and the availability of capital.

Many large, organised players also outsource manufacturing to small manufacturing units and artisans (Chart 2). This reflects the nature of jewellery manufactured in the country; about 55% is handmade (Chart 3), a figure that was much higher in the early 2000s. The high share of handmade jewellery means that many karigars are involved in producing intricate pieces, which is a unique selling point for Indian gold jewellery in the global market.

Chart 2: Many large, organised manufacturers outsource manufacturing to small manufacturing units and artisans

Jewellery Market Structure 2022: Chart 2

In-house vs outsourced manufacturing (% of volume of manufactured gold jewellery)

Sources:

Metals Focus,

World Gold Council; Disclaimer

Chart 3: Majority of manufactured jewellery is handmade in India

Jewellery Market Structure 2022: Chart 3

Handmade vs machine-made jewellery (% of volume of manufactured gold jewellery)

Sources:

Metals Focus,

World Gold Council; Disclaimer

Regions specialise in producing different types of jewellery

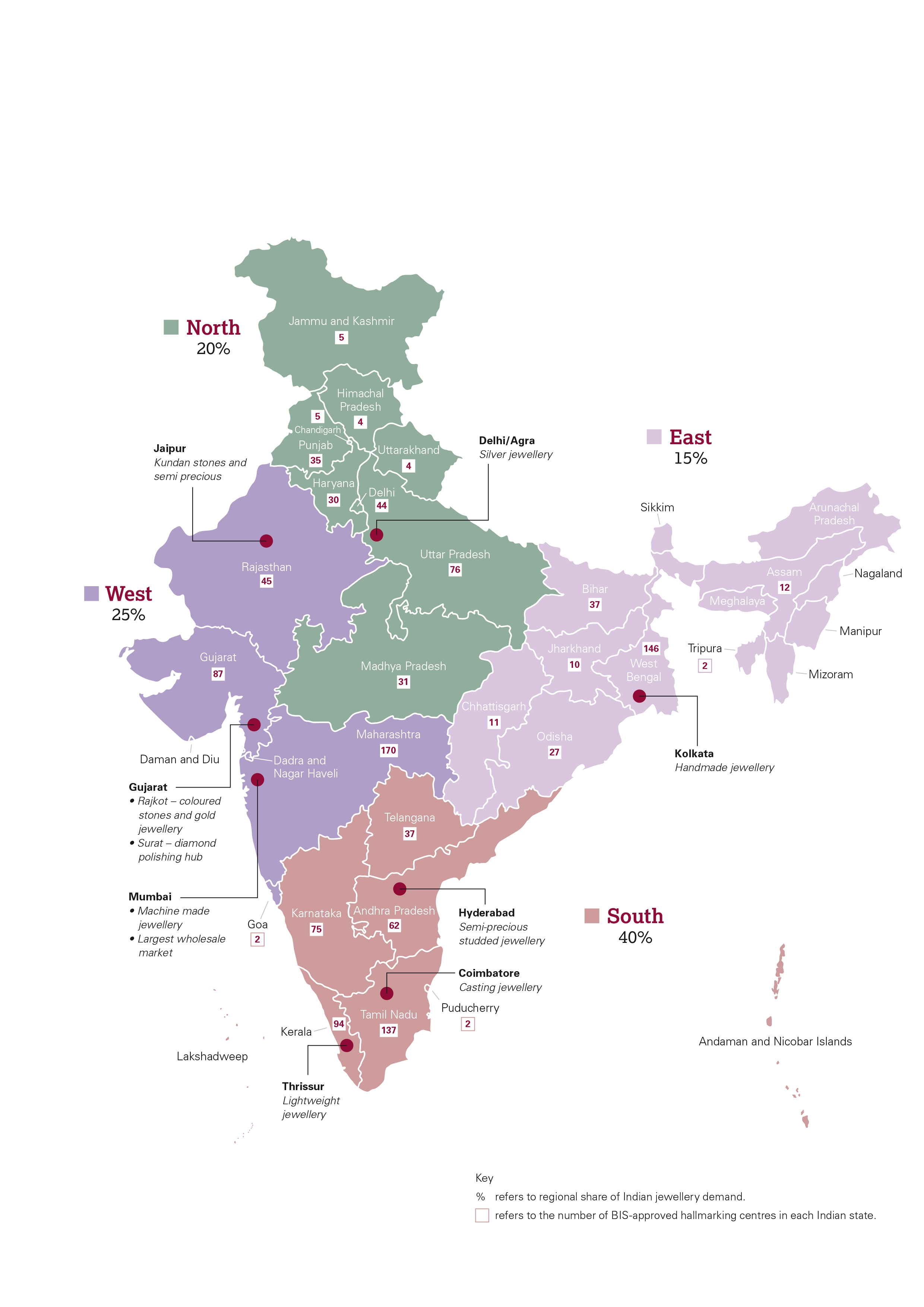

The Indian jewellery market is extremely diverse, with different regions having different tastes and buying preferences. There are some 10 key manufacturing centres, producing around 75-80% of India's jewellery. Of these, Mumbai, Chennai, Kolkata and New Delhi dominate the manufacturing landscape. The other main centres are Rajkot, Surat, Jaipur, Coimbatore, Thrissur and Hyderabad (Figure 1).

Each of these centres specialises in a different kind of jewellery. For example, Mumbai is the hub of machine-made jewellery, whereas Jaipur specialises in jewellery studded with Kundan and semi-precious stones and Surat is the hub of diamond jewellery; Coimbatore is the centre for casting jewellery while Chennai and Kolkata are known for handmade pieces.

The majority of manufacturing facilities in India are small workshops with two to four employees

Figure 1: Major jewellery manufacturing and hallmarking centres in India

The map shows the number of BIS-approved hallmarking centres in India

Working conditions for karigars/artisans must improve

While karigars form the backbone of the Indian gem and jewellery industry, many work in very poor conditions (Focus 3). The National Institute of Labour and Economic Research and Development (NILERD) under the aegis of NITI Aayog published a paper in 2020 called 'Socio-economic and working conditions of workers in the Indian gold industry’. The report highlighted some startling facts. Most karigars/artisans working in the industry are employed on a contractual basis with very little access to healthcare or proper working conditions. Moreover, a large proportion are underpaid, earning between Rs15,000-16,000 (US$190-200) per month, much lower than many other industries.36 The report mentioned that 71% of workers do not have social security benefits such as an Employee Provident Fund (EPF).

Jewellery parks will help the industry become organised and improve working conditions for artisans

To encourage and streamline the manufacturing of gems and jewellery, various state governments are looking at promoting the set-up of jewellery parks by themselves or by industry bodies. These integrated industrial parks provide access to facilities under one roof, including manufacturing units, commercial areas, residences for industrial workers, commercial support services and an exhibition centre.

Currently, most jewellery manufacturing takes place in congested areas with a lack of proper facilities for artisans or for the movement of goods. Most workers spend approximately 12 hours a day in small rooms that are not self-contained units and lack toilets or kitchens. Moreover, there is no proper worker accommodation, no training and no other ancillary facilities. Such manufacturing could relocate to jewellery parks, thus improving conditions and helping to develop the trade itself.

Jewellery parks would also help modernise the trade, as units would be better designed and there would be ample space available for modern machinery. Sitapura Special Economic Zone (SEZ) in Jaipur and Santacruz Electronics Exports Processing Zone (SEEPZ) in Mumbai, set up on 200 acres, boast manufacturing units with technology that has helped improve export potential. Currently, there are two jewellery parks operational in Ankurhati and another in Surat. Ankurhati focuses on plain gold jewellery whereas Surat engages in diamond cutting and polishing, and jewellery manufacturing. Three more jewellery parks will likely emerge over the next five years, two in Mumbai and one in Raipur.

Hallmarking was made mandatory at last

The Bureau of Indian Standards (BIS) first introduced hallmarking in 2000. Through its networks of offices the BIS grants licenses to certify gold jewellery under BIS Standard IS1417. BIS certification was brought in to stop under-carating in the country. According to our study in 2017, some 10-15% of jewellery sold was below the stated purity.37 In 2018 the new BIS (hallmarking) regulation was introduced, laying the roadmap for the introduction of mandatory hallmarking within the trade and protecting consumer interests. Consultation between the BIS and the industry has helped to ensure the required infrastructure is in place.

The Department of Consumer Affairs, the ministry governing BIS, issued a notification to make gold jewellery hallmarking mandatory on 15 January 2020. However, the intended launch date of January 2021 was postponed until June of that year due to the pandemic. Meanwhile, the industry had raised concerns about the lack of assaying centres in many towns; in response, the government announced the implementation of hallmarking in 256 districts (out of 742). Discussions between Metals Focus and BIS indicate that the remaining districts will be subject to mandatory hallmarking in the next couple of years.

Under the new BIS guidelines, mandatory hallmarking is applicable to six purities: 14k, 18k, 20k, 22k, 23k and 24k. While the initial guidelines had only allowed 14k, 18k and 22k, the remaining two were added later after industry representations. Jewellery of other purities will not be allowed to be sold in the domestic market unless:

The gold jewellery item weighs less than 2g

The jewellery is for export and re-import

The jewellery is made for exhibitions or is an item studded with Kundan, Polki or Jadau.

The guidelines also state that manufacturers, wholesalers and retailers with an annual turnover of more than Rs4m need to be registered with the BIS if they are to sell hallmarked gold jewellery. Despite the many changes to the original guidelines – which were implemented after industry consultation – further challenges impeded their smooth implementation. Additional guidelines were therefore issued in June 2021 with significant clarifications:

Hallmarking at the first point of sale means the onus is effectively shifted to the manufacturer or wholesaler

Purchase of non-hallmarked jewellery is allowed

Jewellery hallmarked before 16 June 2021 does not need to be melted and re-hallmarked

Artisans involved in job work are not required to register with the BIS.

Focus 3: Working conditions of artisans

India is one of the largest markets for gold and gold jewellery, with gold playing a significant role in representing the culture and art of India and expressing the owner’s stature in society. From a marketing perspective, gold jewellery offers a glamorous look to customers, but on the other hand, the manufacturing process of gold jewellery and the hands creating it are often unnoticed.

The Indian gold manufacturing industry can be segregated into two forms: regulated (formal) and unregulated (semi-formal and informal). The former covers a formal hierarchy and processes, and often a corporate touch. The conventional system, which is unregulated, also exists side by side with the formal. Together, the sector is one of the largest employment generators with an estimated 4.65 million employees (as per Gem and Jewellery Skill Council in India).

Seeing the growth and value of the sector and potential employment opportunities, the government has also introduced skill development initiatives for the sector. The market employs a large number of artisans (karigars), who learn the craft through an informal but well-set system of “apprenticeship”, and a “karigar life cycle” that embeds the gold worker in the system for many years. We worked on a research project intended to explore Human Resource Management and labour management practices in gold jewellery manufacturing. The research idea was to understand labour and talent management in the formal, semi-formal and informal sectors, and explore whether any convergence or divergence in the HRM/labour management practices can be observed.

Our analysis of the informal sector shows the existence of “precarious work”, while formal sector companies have progressive practices that can qualify as best in class across different sectors. The latter is motivating the others, particularly semi-formal companies, to improve the working conditions of artisans and take initiatives to increase work productivity. Responsible outsourcing and adopting various practices for improving social security standards and safety conditions of the artisans are a few steps taken by formal companies. Another significant step being adopted is creating future skill sets and career paths. However, when compared with the universe of gold jewellery manufacturing such firms are very few.

In the current situation, the industry in general is facing a scarcity of experienced artisans and young talent. The new generation is not willing to join the industry. Reasons for this include the absence of basic amenities and hygiene at the workplace and poor reward practices. Most importantly, artisans feel that work recognition is absent, i.e. there is no appreciation for the sweat and hard work that they put in.

The average artisan’s income is low when compared to other sectors, and as contractual employees, they often receive remuneration that is not sufficient as a starting point for a career. In addition, the variable pay doesn’t add much to total earnings, which is also one of the main reasons for attrition in the industry.

Furthermore, existing artisans do not encourage their children to join the industry. Since the manufacturing process and talent pipeline have changed, we suggest that skill development is taken as a priority and should be implemented quickly for the sector to remain competitive. The government should set up training centers where the existing, as well as the new talent entering the industry, can be trained. Without some skill enhancement, the future of this sector in India is uncertain. Stakeholders associated with the industry have voiced repeatedly that, while there is job security in the industry due ample employment opportunities, there is a lack of social security. As a good HRM practice we suggest that employers/manufacturers should take on the responsibility to introduce government social security schemes for both permanent and contractual karigars.

The labour dynamics in the sector resemble the gig workers paradigm. A section of artisans is not willing to be bound with employers/contractors. In fact, they prefer to work according to their own choice and convenience. Another section of artisans wants to work in a formal set-up, earning a fixed salary and other benefits, thereby enjoying more security. The set of artisans who are not comfortable working in a formal set-up believe their freedom will be compromised, and we observed that they are fine compromising their living standards for flexibility and freedom offered by the informal sector. Many young entrants use the informal sector as a launch pad (for learning opportunities) to build more secure careers in the formal sector. We find that in the gold jewellery manufacturing sector formal, semi-formal, and informal work all co-exist. Hence, clear segregation of work boundaries is not possible as the formal and semi-informal sectors directly or indirectly depend on the informal sector for production, or for artisans.

In this context, responsible outsourcing is an approach that can improve the conditions of existing artisans and secure the future of the industry. Stakeholders in the sector (industry, associations, trade unions, etc.) should work towards creating a responsible supply chain and contribute to training in advanced machinery and manufacturing practices for artisans, helping to enhance the artisans’ overall skill sets and livelihood opportunities.

Prof. Biju Varkkey, IIM Ahmedabad

Prof. Jatinder Kumar Jha, XLRI Jamshedpur

Novel Ansari, Research Associate, IIM Ahmedabad

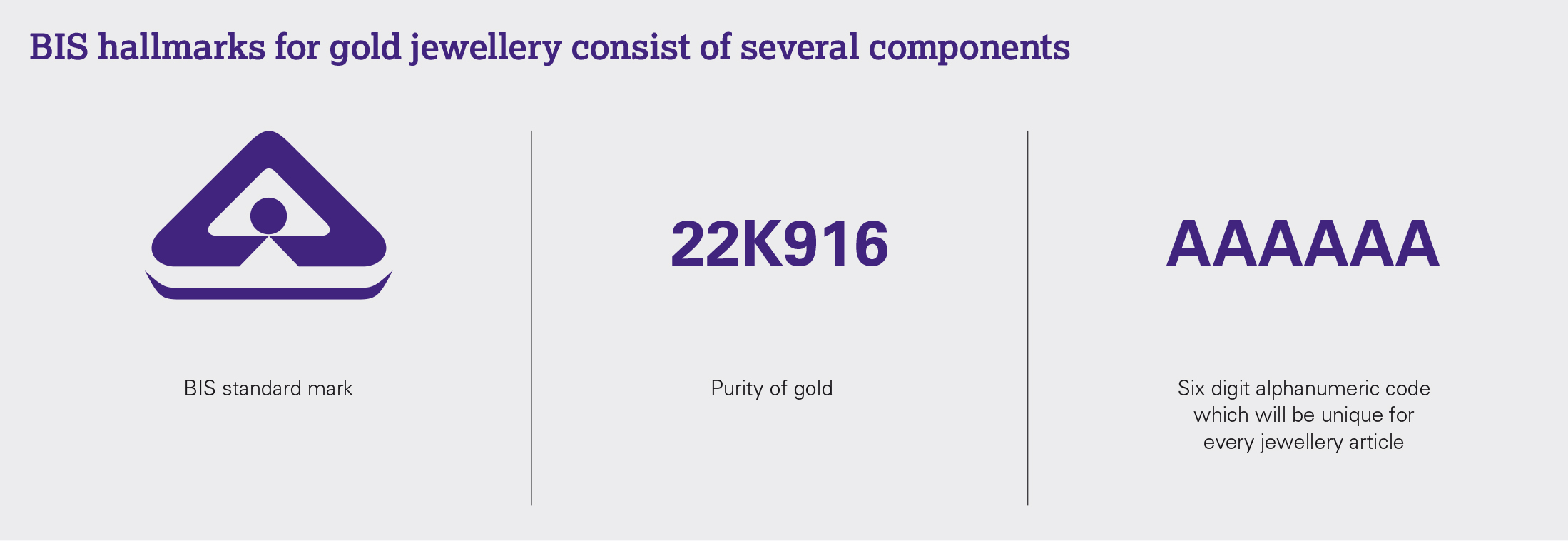

Hallmark Unique Identification (HUID) number could transform the market

The Indian government has focused on technology to transform the Indian economy and bring greater transparency to the social benefit delivery system. It is thus not surprising that they have announced the use of technology to ensure the authenticity of hallmarking through the introduction of the Hallmark Unique Identification (HUID) number. The HUID is a six-digit alphanumeric code unique to each piece of jewellery (Figure 2). The jewellery is manually stamped with this number at an assaying and hallmarking centre. The ID is automatically generated without any human interference to ensure that there are no malpractices.

Figure 2: Hallmarked jewellery with HUID

Source: JJ Gold House, Kolkata

According to the BIS, the new hallmark consists of three symbols: the BIS logo, the purity and finesse, and the HUID number. Such traceability will enhance consumer confidence in the jewellery they buy. The government aims to create a central platform where consumers can look up an HUID number and see all details linked to that piece, notably the jewellery manufacturer, hallmarking and assaying centre, and the jeweller's name.

Mandatory hallmarking will level the playing field and increase demand

Aside from having funds for aggressive marketing campaigns and the ability to offer a wide choice of designs, one factor that has helped retail chain stores gain market share over the years has been the assurance they offer around purity. Chain stores have guaranteed that their gold jewellery is of the quality stated, and that consumers will receive full value when exchange or return takes place. Despite this, it is widely accepted that a large amount of jewellery sold in India is under caratage. According to discussions between Metals Focus and refineries, gold that comes back as scrap for melting often ranges between 70-85% purity.38 This has bred mistrust among many consumers. Our consumer insights study published in November 2019 highlighted that 28% of jewellery consumers who had not previously purchased gold cited a lack of trust as a barrier to purchase.39

This lack of trust has, in the past, benefited large, organised players but the introduction of mandatory hallmarking will help to level the playing field in terms of purity, and focus competition on elements such as design and customer service. Furthermore, mandatory hallmarking is likely to increase trust among young consumers. Our consumer insights study highlighted that trust is a major factor for gold jewellery purchases. The government has stated that increasing trust is one of the key objectives in the introduction of mandatory hallmarking. Metals Focus believes that hallmarking will increase demand over the longer term.

Outlook

The Indian jewellery market has seen many structural changes over the last decade, some brought about by regulation and some by a shift in consumer behaviour. While the hallmarking regulations will provide a level playing field, national and regional chain stores are set to continue to gain market share because of their access to credit and the large inventory they carry. However, as many players start entering Tier 3 and Tier 4 cities, there should be a certain level of aspirational demand that they can tap into, allowing branded players to quickly gain market share. Small players need to become more transparent if they are to access credit, as banks and financial institutions are currently wary of lending to the gems and jewellery sector.

While the jewellery retail sector continues the trend it began over a decade ago and becomes increasingly organised, the manufacturing sector is only at the beginning of this journey. Government and industry are focusing on shifting manufacturing from congested centres to jewellery parks and this will aid organisation within the trade. Meanwhile, the growing concern among retailers and consumers about ethical standards and working conditions of artisans represents an industry threat. In response, many large players only want to work with organised manufacturers, and it is these who will see their market share strengthened going forward.

footnotes

Chain stores are jewellers with more than 10 jewellery stores.

Artisans are skilled workers who manufacture handmade jewellery.

A study on socio economic and working conditions of workers in Indian gold industry, National Institute of Labour and Economic Research and Development (NILERD)

As per Census 2011 there are 4,041 Statutory Towns in India. Statutory towns are defined as places with a municipality, corporation, cantonment board or notified town area committee, etc.

Census 2011

A Nagar Parishad or city council is a form of urban political unit in India comparable to a municipality. A Nagar Parishad will have a population of more than 20,000 and less than 100,000

The Unified Payments Interface is an instant real-time payment system developed by the National Payments Corporation of India to facilitate inter-bank, peer-to-peer and person-to-merchant transactions.