Footnotes

The LBMA Gold Price PM was nearly 13% higher y-t-d as of 1 December, performing better than the Bloomberg Commodity Index, Bloomberg Global Bond Aggregate, and the MSCI All Country Index excluding the US.

Bond derivatives markets are pricing around 75bps of cuts by the Fed and European Central Bank starting in June, with other central banks such as the Bank of England to follow. In addition, the Fed’s dot plot indicates that most FOMC members expect the fund rate to be down from current levels by the end of 2024.

ISM economy-weighted composite PMI at 51.3. Manufacturing PMI at 46.7. As of October 2023. Source: Bloomberg

Real average hourly earnings at 0.8% as of October 2023. Source: Bloomberg

Data Revisions and Pandemic-Era Excess Savings | San Francisco Fed (frbsf.org)

At the time of writing, US payroll growth was 200,000 per month based on a seasonally smoothed three-month average.

Sahm Rule Recession Indicator, St. Louis Fed (stlouisfed.org). It is worth noting, however, that Claudia Sahm, author of this indicator, has recently said that the Sahm Rule may break without a recession due to pandemic and post-pandemic economic distortions. Claudia Sahm: ‘We do not need a recession, but we may get one’, FT.com, November 2023

Some investors are taking an alternative view that Fed funds futures are pricing no landing rather that a soft landing. See: Fed Funds Futures Pricing in "No Landing" - Apollo Academy

Prospects for a global ‘rebound’ | TS Lombard

The Great Pandemic Mortgage Refinance Boom - Liberty Street Economics (newyorkfed.org)

The notorious wall of maturities revisited (ft.com)

From UAW to WGA, here’s why so many workers are on strike this year (cnbc.com)

Soft, Hard or No Landings, Ukraine - Time to Have Your Say - Bloomberg

Gold also responds to supply-side factors: primarily recycling in the medium term, and mine production as the longer-term determinant, based on its scarcity.

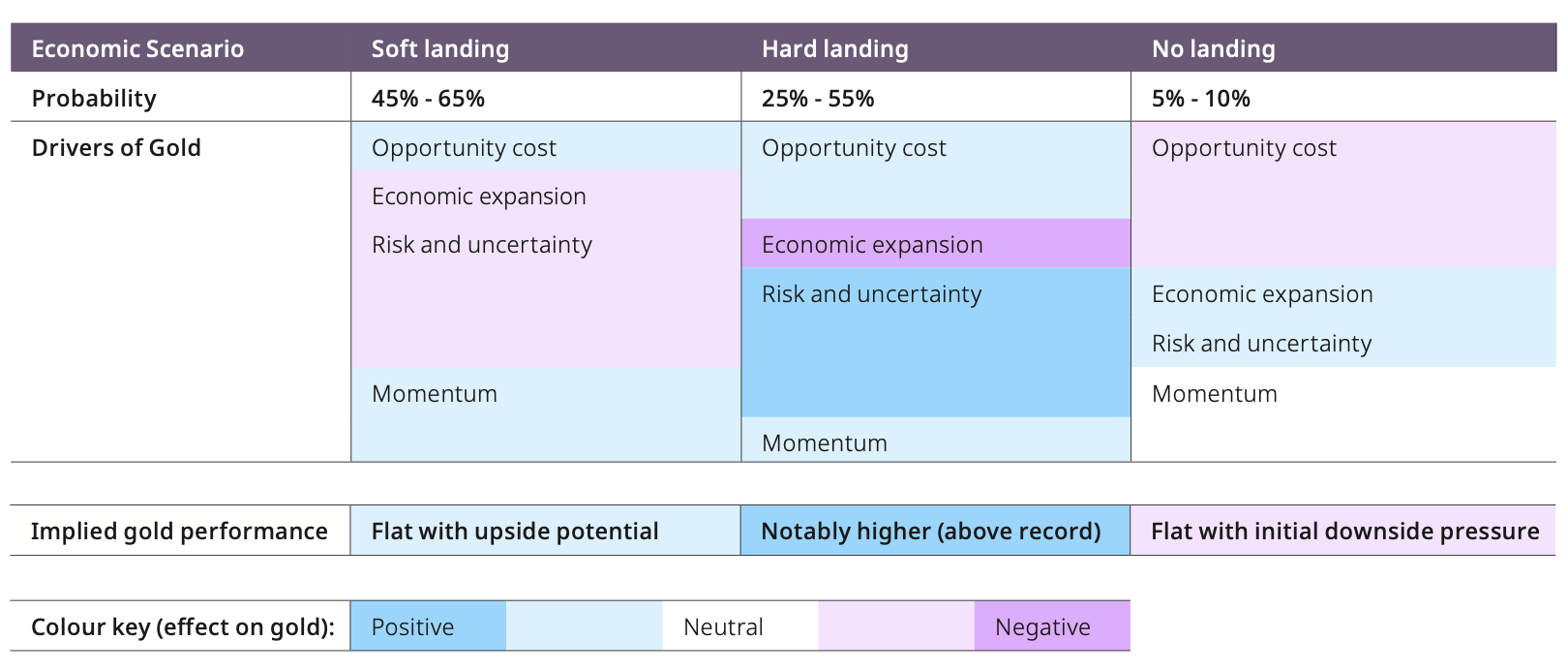

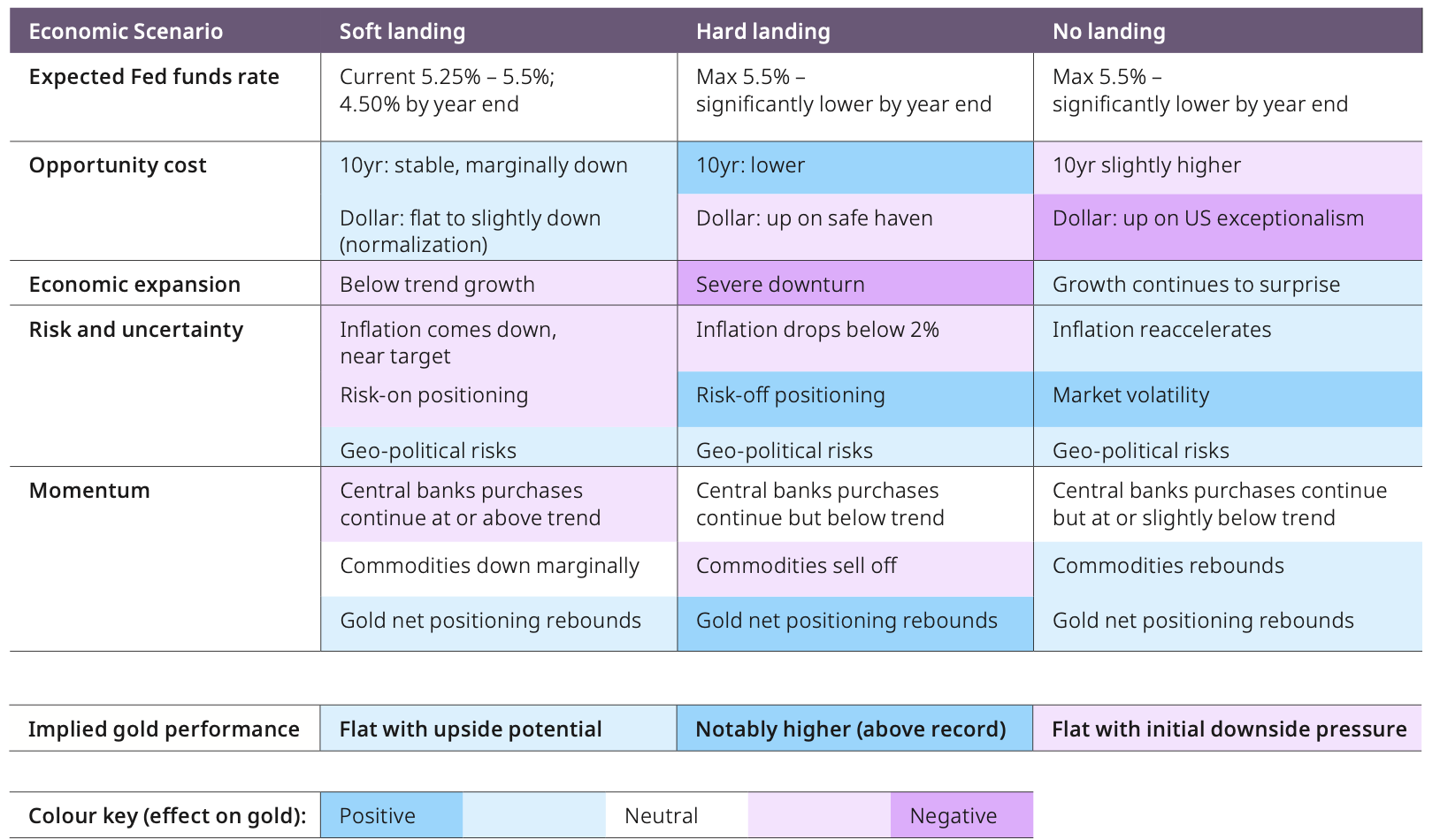

It is common for investors to look at gold’s performance through two factors: real interest rates and the US dollar. While useful in the very short term, these factors alone are not sufficient to explain its behaviour and can lead to inaccurate perspectives.

S&P 500 2024 consensus earnings growth forecast of 12% y/y.

“In 2024, countries making up over 50% of global GDP will undergo decisive elections.” Eight Key Elections to Watch in 2024, Brunswick Geopolitical, September 2023.

2023 Central Bank Gold Reserves Survey, May 2023.

Conversely, slower than expected demand would likely create a drag gold.