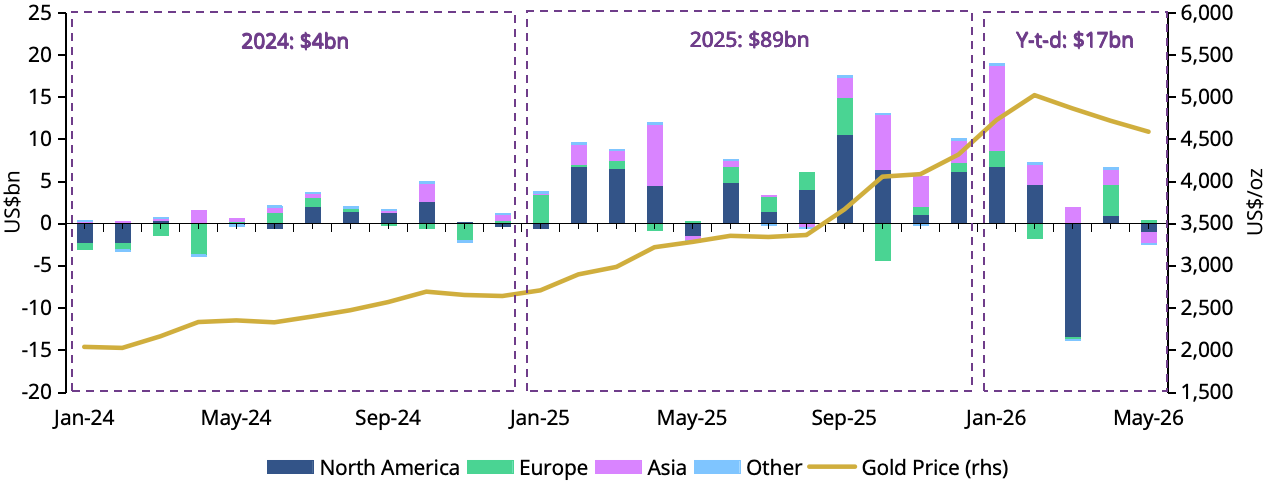

Trading activity inches higher in May

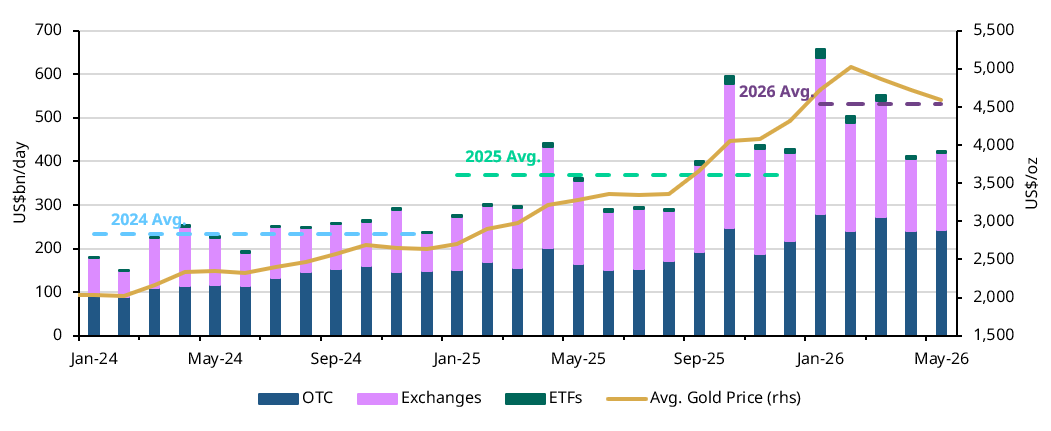

Global gold market trading volumes2 inched higher by 3% m/m to US$424bn/day in May. Volumes remained 15% above the 2025 average of US$368bn/day, signalling ample gold market liquidity despite gold’s recent range-bound performance.

Over-the-counter volumes increased slightly by 1% in the month to US$243bn/day and remained well above the 2025 average of US$180bn/day. Exchange-traded activity reported positive m/m growth, increasing 6% to US$175bn/day. This modest improvement was driven by higher COMEX activity but partially offset by a decline in Shanghai Futures Exchange volumes. Global gold ETF trading volumes saw a notable reduction of 26% m/m to US$6bn and fell below their 2025 average of US$7bn.

Positioning data pointed to a marginal reduction in total COMEX net longs, which declined 2.5% over the month to 466t.3 Interestingly, managed money positions increased in May over three of the four weeks, adding an additional 17t. However, the overall reduction stemmed from selling in other reportables4, which fell by 29t during the month. Non-reportable positions, often associated with retail activity, showed a similar pattern, with a reduction of roughly 12t. Overall, positioning continues to hover in neutral territory as investors await a clear near-term catalyst, while the long-term fundamental story remains intact.

Chart 3: Trading volumes rose despite a rangebound gold price

Average daily trading volumes by segment*

*Data as of 31 May 2026. Gold price based on the monthly average LBMA PM Gold Price USD.

For more information on trading volumes please visit our Trading Volumes page on Goldhub: Gold Trading Volume | Gold Daily Volume | World Gold Council.

Source: Bloomberg, Nasdaq, COMEX, ICE Benchmark Administration, Shanghai Gold Exchange, Shanghai Futures Exchange, ETF providers, Multi Commodity Exchange of India, Dubai Gold & Commodities Exchange, Japan Exchange Group, Thailand Futures Exchange, Borsa Istanbul, Bursa Malaysia, Korea Exchange, World Gold Council