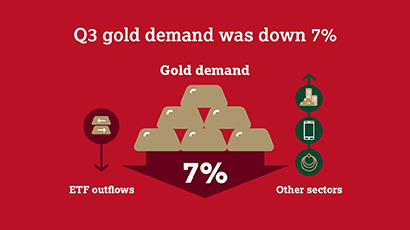

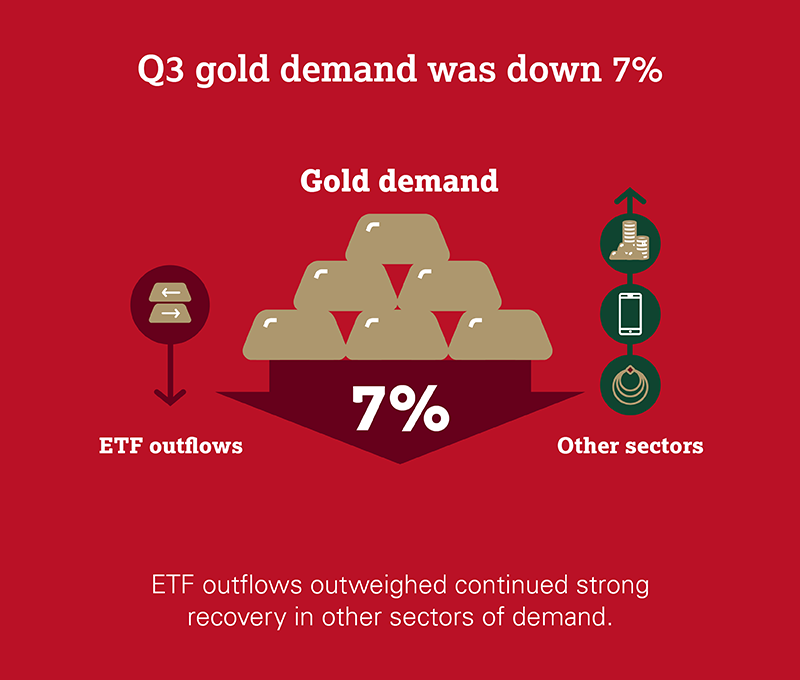

Q3 gold demand down 7% to 831t

ETF outflows outweighed continued recovery in other sectors

Gold demand (excluding OTC) fell 7% y-o-y to 831t in Q3. This drop was almost exclusively driven by ETFs – which swung from very large inflows in Q3 2020 to modest outflows this year – overshadowing strength in other sectors of demand during the quarter. Jewellery, technology and bar and coin were significantly higher than in 2020. Modest central bank purchases were a solid improvement on the small net sale from Q3’20. Supply was down 3% y-o-y due to a significant drop in recycling.

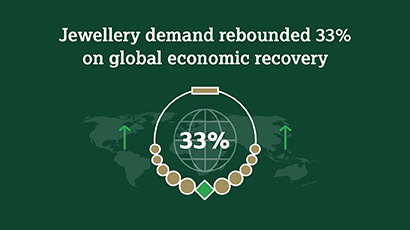

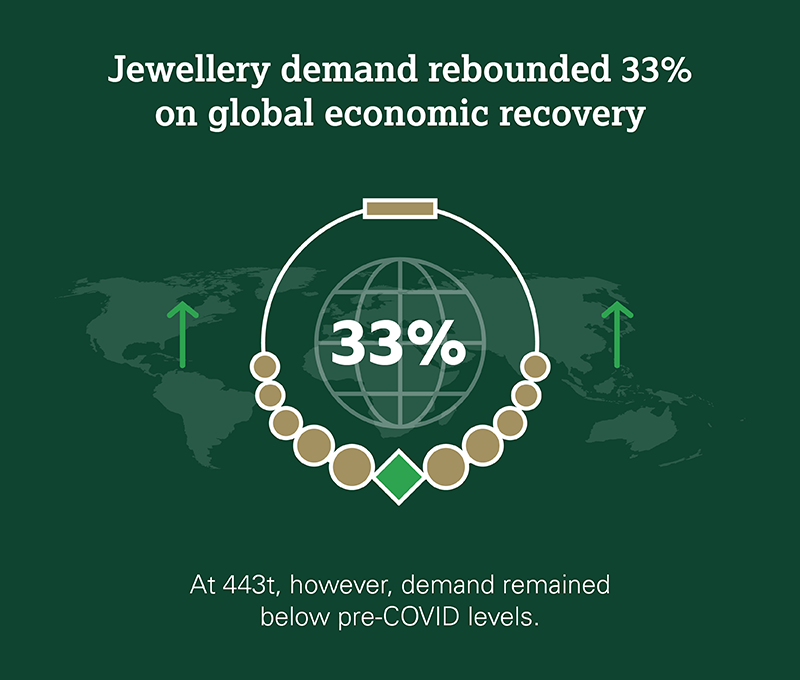

Jewellery continued to draw strength from the ongoing global economic recovery: Q3 demand rebounded 33% y-o-y to 443t.

Bar and coin investment increased 18% y-o-y to 262t. The sharp August gold price dip was used by many as a buying opportunity.

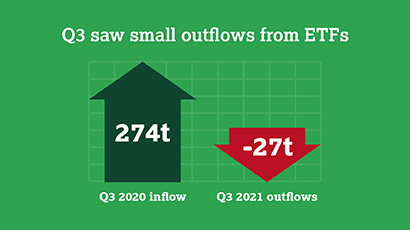

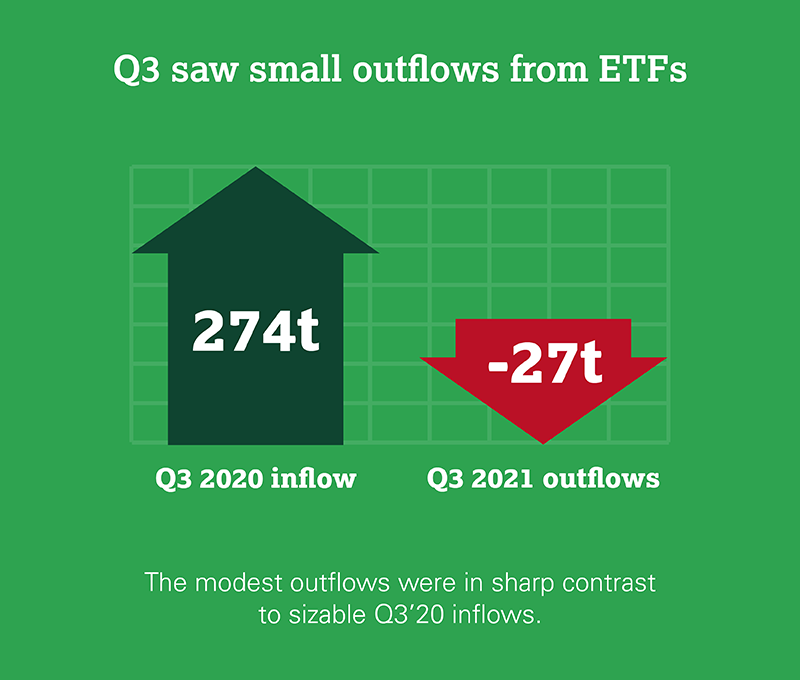

Small outflows from global gold ETFs (-27t) had a disproportionate impact on the y-o-y change in gold demand, given the hefty Q3’20 inflows of 274t.

Central banks continued to buy gold, albeit at a slower pace than in recent quarters. Global reserves grew by 69t in Q3, and almost 400 y-t-d.

Technology gold demand grew 9% y-o-y, driven by continued recovery in electronics. Demand of 84t is back in line with pre-pandemic quarterly averages.

{kind=link}

{kind=link}

{kind=link}