Weak Q4 set the seal on an 11-year low for annual 2020 gold demand

The global gold market was ravaged by COVID-19 disruption throughout the year, while record high prices were a mixed blessing.

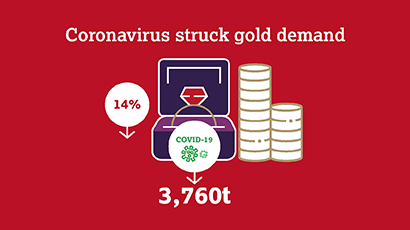

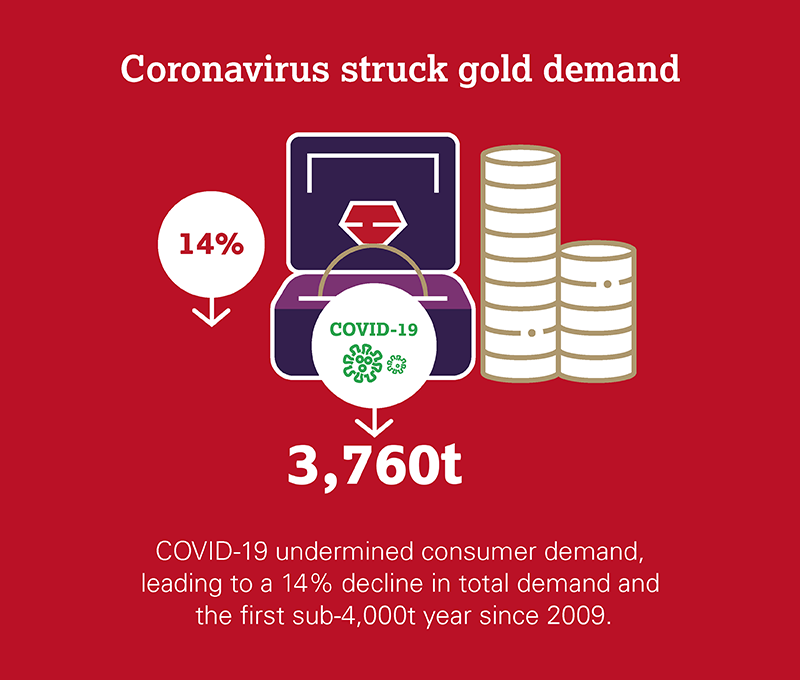

Fourth quarter gold demand of 783.4t (excluding over-the-counter – OTC – activity) was 28% lower y-o-y, making it the weakest quarter since the midst of the Global Financial Crisis in Q2 2008. The coronavirus pandemic, with its far-reaching effects, was the driving factor behind weakness in consumer demand throughout 2020, culminating in a 14% decline in annual demand to 3,759.6t, the first sub-4,000t year since 2009.

Gold jewellery demand in Q4 fell 13% y-o-y to 515.9t, resulting in a full-year total of 1,411.6t, 34% lower than in 2019 and a new annual low for our data series. While demand improved steadily from the severely depleted Q2 total, consumers across the world remained at the mercy of coronavirus lockdowns, economic weakness and high gold prices.

Bar and coin demand grew 10% y-o-y in Q4, pushing annual retail investment up 3% to 896.1t. Nevertheless, demand remained weak relative to the 10-year average (1,199.5t).

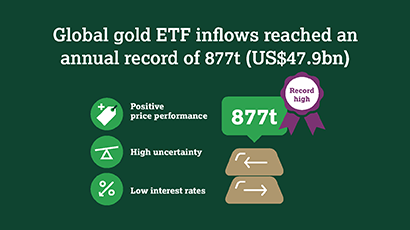

Despite 130t of outflows in Q4, gold backed exchange-traded funds (gold ETFs) saw record annual inflows: global holdings grew by 877.1t in 2020. In addition, evidence suggest that OTC activity, which is not directly captured in our data set, was also robust throughout the year.

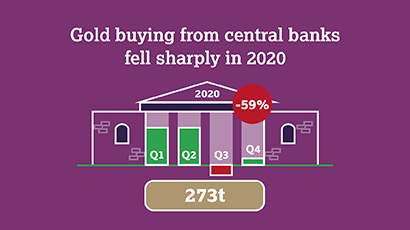

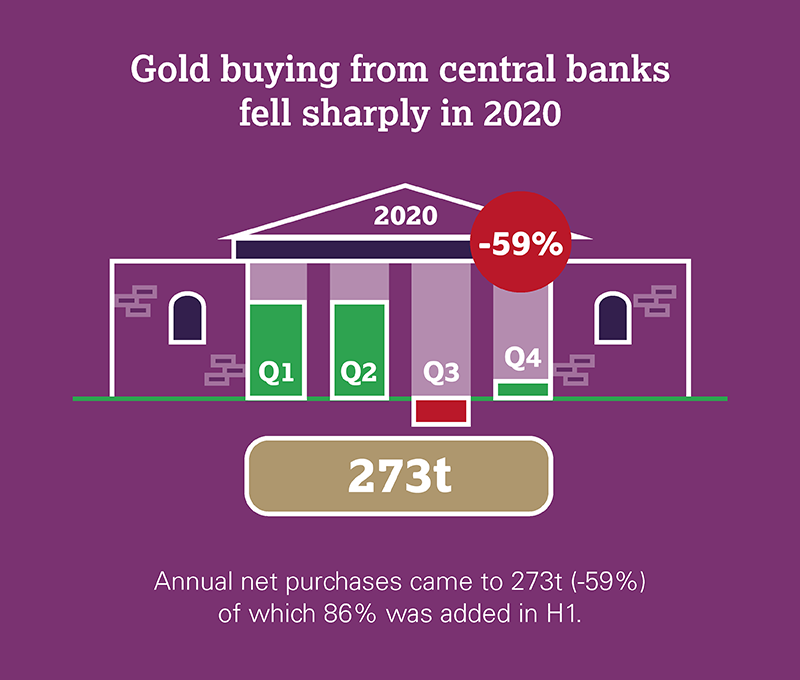

Central bank buying slowed sharply in 2020, particularly in the second half of the year. Q4 saw a return to modest net buying (44.8t) after the prior quarter’s small net sale. Annual central bank purchases came to 272.9t (-59%) of which 86% was added in H1.

The technology sector, impacted by disruption from COVID-19, saw gold usage decline 7% in 2020 to 301.9t. But the year ended on a relatively positive note, with Q4 seeing marginal y-o-y growth to 84t.

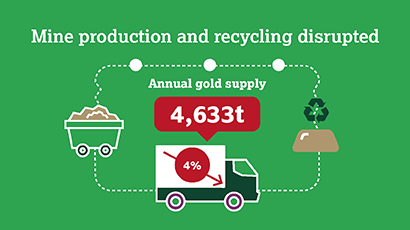

Total annual gold supply of 4,633t was 4% lower y-o-y, the largest annual fall since 2013. The drop was largely explained by coronavirus-related disruption to mine production, offset by a marginal 1% increase in recycling to 1,297.4t for 2020.

{kind=link}

{kind=link}

{kind=link}

{kind=link}