Central bank considerations when pricing ASGM purchases

Central bank considerations when pricing ASGM purchases

Introduction

The strength of world gold prices has enhanced both the level and the value of Artisanal and Small-Scale Gold Mining (ASGM) in countries around the world.1 This presents challenges to societies and governments on a range of issues related to ASGM mining, such as environmental, societal, legal, regulatory and economic. Several papers exist that cover these issues, the government response to which may be a State Gold Buying Program (SGBP).2 The purpose of this paper – whilst acknowledging the issues outlined above – is to examine the price-setting process for central banks in a SGBP.3

With growing frequency central banks are acting as an agent in a SGBP, purchasing the growing volume of ASGM output. As legal and tax laws are country specific, this paper cannot provide specific advice in these areas. Rather it discusses issues central banks may consider around pricing their ASGM purchases. It does not consider questions arising from central bank purchases from mid- or large-scale local gold mining.

The paper discusses:

The rationale for central bank ASGM gold purchases

Related issues for any gold purchase program

Considerations when setting the price for ASGM purchases

Factors affecting gold price setting

Configurations for central bank gold purchases

Accounting issues for ASGM purchases.

This paper is provided for informational purposes only and does not constitute legal or tax advice. Readers should consult their own legal, tax and financial advisors before making any decisions based on the information contained herein.

Rationale for central bank ASGM gold purchases

Central bank foreign exchange reserves may include monetary gold as an element within their portfolios.4 Traditional practice has been for central banks to acquire their gold as allocations from their own treasuries or through purchases on international markets.5 Such practices have ensured a transparent pricing mechanism that has protected central banks from accusations of improper pricing or transfers in favour of a preferred domestic party. Central banks that undertake local ASGM purchases should, however, address related pricing issues both within the SGBP and the broader framework of central bank mandates.

A credible rationale exists for central banks to undertake gold purchases within the standard framework of core central bank functions. These include the maintenance of foreign exchange reserves, financial stability, and the encouragement of economic growth. Central banks and governments need to consider a number of factors before deciding whether the rationale applies in their situation.6 These include:

Existing dynamics in the gold industry

The cost of operating a gold purchase program

The distribution of gold producing areas

Existing legal and regulatory frameworks

The ability of the central bank to manage gold purchases and sale activities as part of its operations

The need for the central bank to accumulate monetary gold holdings.

Situations exist where it is more appropriate for a separate agency, unrelated to the bank, to operate the gold purchase program, or for the country to rely on existing markets.

Related issues for any gold purchase program

Definition of a gold buying mandate

A central bank requires a mandate to purchase ASGM gold as part of its core roles to manage the country's monetary policy and foreign exchange reserves, and to promote financial stability. Countries may express ASGM mandates in different ways:

To buy domestic gold to meet requirements in its foreign reserves strategic asset allocation benchmark

To buy a specific amount of gold, as defined by the government approved SGBP7

To take responsibility for the purchase and resale of all domestic gold production

To buy domestic gold production to achieve objectives beyond the scope of its core functions.

The scope of the mandate will affect central bank participation in any ASGM purchase program, along with other factors such as the existence of alternative markets or buyers, and any legal requirements for local producers to sell gold to the central bank.

Legal authority

In any ASGM purchase program the central bank uses public resources under its control to fund the purchases. This requires the bank to demonstrate that it has the legal authority to use these resources and that it has used them prudently, or at least within its empowering framework. Hence, any central bank involvement in a SGBP requires legislation, either in the national minerals law, central bank law, or other relevant legislation. Central banks should have appropriate legal counsel in any drafting of such legislation.

As stated, this paper cannot offer any legal or tax advice, but rather identifies issues central banks should consider when developing legal provisions for gold purchases.

Any legal provisions should cover relevant aspects of a gold purchase program, be consistent with the bank’s stated mandate, and avoid any unintended consequences. This legislation should define the central bank’s role in the gold purchase program, while facilitating its gold pricing and purchases.

Depending on the government’s intentions and objectives, a central bank's involvement in a SGBP may extend beyond a narrow purchasing function. While the current orthodoxy favours limiting a central bank’s involvement to its core functions, the legal framework should specify and authorise the scope of all central bank involvement in the gold industry, including the incidence of associated costs. Examples of this extended involvement could include licensing, collection of mining royalties, granting export licenses, assaying standards, and other regulatory roles. Any proposal for central banks to provide finance to the ASGM sector generally falls under the gamut of quasi fiscal activities that most central bank laws prohibit.

Legislation defining the calculation of the ASGM gold’s purchase price should reflect the program’s objectives and operating environment. Most gold purchase programs have an element of market normalisation that seeks to ensure that ASGM producers receive full value for their gold sales. This might be interpreted as a need for purchase program regulations to specify that the bank purchases the gold at international prices. However, ASGM doré is not in a form or location where it can demand quoted prices for fully refined, London Good Delivery (LGD) gold. As discussed later, the law should allow the central bank to make provision for costs involved in converting the doré to a monetary gold standard.8 While ensuring a market-based price for ASGM agents is a legitimate objective, any wording referencing international prices should include a clause allowing the central bank to adjust prices for costs incurred.

The legal right to undertake gold purchases becomes very important for a central bank's defence in the event of losses on gold purchases. The paper discusses this later.

The following are examples of legal mandates for central bank gold purchases:

Ecuador

The Central Bank of Ecuador (BCE) uses Article 36 of the Fundamental Monetary and Financial Code to authorise its purchases of ASGM gold. This enables it to fulfil its obligations to sell gold authorised in Article 49 of the Mineral Act.9

Philippines

The Bangko Sentral ng Pilipinas, (BSP) has the authority to purchase ASGM gold via The Republic Act No. 7653, also known as the New Central Bank Act. The BSP purchases gold as part of its mandate to build up the country's international reserves and to support the stability of the Philippine peso.10 It is important to note that producers are bound by regulations and procedures that govern these transactions. Individuals or entities selling gold to the BSP must comply with these regulations, which include requirements for proper documentation and verification of the origin of the gold being sold.

Columbia

The Bank of the Republic of Columbia derives its authority to purchase gold from Colombian law, particularly under the Statute of the Bank of the Republic (Ley 31 de 1992) and other relevant regulations.11

Infrastructure

Any central bank ASGM program requires an infrastructure within which the purchasing program will operate. The scope and nature of that infrastructure will vary across each economy, with the costs accruing differently to producers, aggregators, government agencies and the central bank.

In the Philippines, the BSP operates five buying stations in gold producing areas. In addition, it is developing contractual buying arrangements with pawn shops. In Mongolia, commercial banks function as purchasing agents for the central bank and carry the costs of providing the service. Each configuration brings different levels of infrastructure costs for the central bank to consider.

Accounting standards exclude these infrastructure costs when calculating the value of a gold inventory as they are fixed, indirect costs. Examples of such infrastructure costs include, but are not limited to, assay costs, buying costs, storage, and security costs at each point of the gold’s journey. Depending on the scope of the central bank’s involvement, infrastructure costs may also include licensing, inspection and regulation, if these are central bank responsibilities. The central bank should include these expenses when determining a purchase price, though not the value of the eventual inventory, as they impact the overall return on any gold purchase program.

An important consideration is that the broader the central bank’s ASGM infrastructure costs, the greater the non-financial risks and challenges it assumes. The central bank should include this broader range of costs and risks when assessing the viability of any ASGM program.

Considerations when price setting for ASGM purchases

Issues beyond acquisition of foreign reserve assets

The central bank mandate regarding ASGM gold purchases may have a range of objectives, such as to:

Integrate the ASGM sector into formal markets

Achieve specific environmental or social objectives

Address regional or national economic issues

Establish higher standards in gold markets

Take account of government policy and regulatory factors.

Ensuring market neutrality

Setting aside that these objectives may be beyond a central bank’s core mandates, the above factors may be in conflict with the key objective of avoiding a loss on recognition as monetary gold. Considering such factors may exert pressure on the central bank to pay above market prices for gold, and although that may not be inconsistent with their gold buying mandate, it could conflict with normalisation of the local gold market.

Internationally recognised accounting standards require the recognition of non-monetary gold at the lower of cost or net realisable value (NRV). A consequence of paying above market prices may be that the central bank reports the excess of purchase over NRV as losses in its financial statements. This highlights how important it is for central banks to explain their mandate, including associated costs and their impact on achievement of the bank’s other objectives.

A statutory obligation for the central bank to purchase 100% of ASGM production may limit its pricing discretion on two grounds. The existence of parallel markets or smuggling activity may force the central bank to pay a premium to neutralise such activities. Conversely, the existence of such monopsony power risks producers perceiving the central bank’s pricing to be discriminatory and thus seeking alternative distribution channels. The presence of an efficient market at the gold fields and an absence of any quantity targets for central bank purchases lessens any potential conflict.

In a prolonged period of rising gold prices – such as has been seen recently – some central banks have reported that gold traders are paying above the current spot for the quality of local doré in the expectation they will make a profit when they sell the refined gold. This creates challenges for central banks, especially where their mandate requires purchase of a set quantity or percentage of ASGM output. The central bank either misses its purchase targets or is forced to buy gold above spot thus running the risk of losses if future gold prices fail to cover the higher price.

These factors complicate a central bank’s efforts to ensure market neutrality in its pricing policy. It is important that the central bank’s pricing does not distort the market in such a manner that excludes other legitimate buyers, creates conflict with other policy mandates – such as financial system stability – or provides sector specific subsidies that could also distort the market.

Cooperation with other government entities

Central banks need to reconcile any pricing mechanisms with the objectives of other government authorities in the sector. Conversely, other entities should work in conjunction with the central bank to optimise the outcomes of all policy initiatives. Environmental, health and safety, industry normalisation and social equality are just some of the competing objectives that require consideration when setting prices, but which are not normally covered by central bank mandates.

Effect of royalties and taxes

The imposition of royalties and taxes on gold production can conflict with central bank mandate objectives. As the Bangko Sentral ng Pilipinas (BSP) discovered, the imposition of taxes on ASGM production materially impaired the bank’s ASGM purchases, until rescinded. Rather than pay the taxes, the sector turned to parallel markets to dispose of their gold or discontinued operations due to reduced profit margins. To avoid these issues, the relevant government authorities need to agree a common framework regarding the AGSM sector. Article 149 of the Ecuador Mining Act, which applies zero rate VAT to central bank ASGM purchases, is an example of such cooperation. The central bank’s pricing strategy is a critical element of this framework.

Considerations when setting gold price

A central bank requires a pricing strategy to enable it to achieve its domestic gold buying mandate. The bank could:

Pay the spot market price

Pay a percentage discount from the current LBMA price

Pay a price based on an analysis of the actual processing costs

Pay a premium on the spot price.

A central bank may need to pay above the local spot price as part of meeting the quantity or policy requirements of its mandate or the objectives of the local SGBP. Pressure to pay above spot is likely to be more common than paying below spot as several factors exist to limit a bank’s ability in this area. These include the efficiency of markets at local gold fields, the existence of parallel markets and the potential for smuggling.

Where the local spot price exceeds the additional costs of bringing the gold up to a monetary gold standard, the central bank will need to decide how to manage and explain its additional costs – and possible losses – within its accounting framework and the terms of its mandate.

This paper assumes that central banks will have an objective to recognise the gold in its balance sheet as monetary gold at a break even value after processing, with no material gains or losses over time. It also assumes that the central bank’s mandate and the country’s economic situation allows the central bank to have some influence on the price that it pays for the gold, though specific market situations may limit this influence. Some market imperfections may arise where the local spot price is below the bank’s break even purchase price. In such situations the bank’s mandate may guide how it distributes this profit between itself and the ASGM sector.

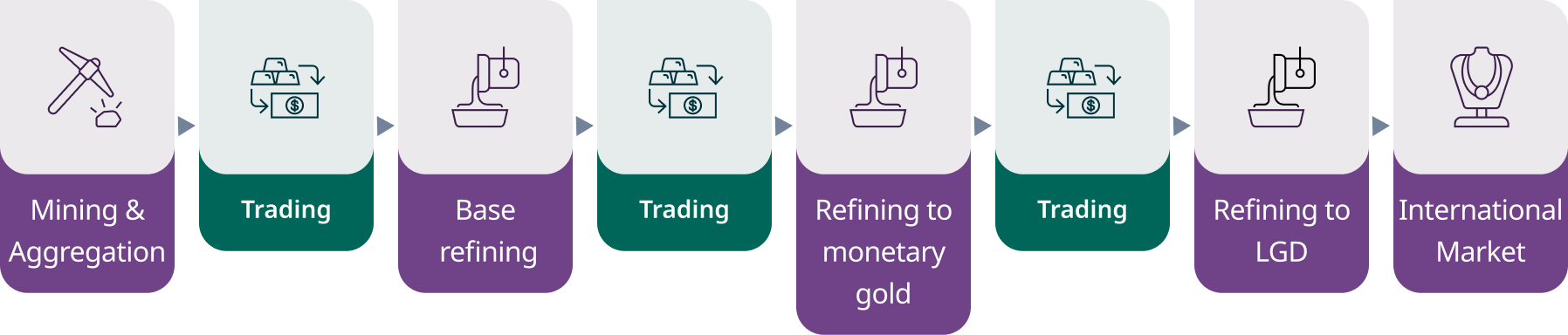

Point of purchase

Central banks buy gold at some point of doré aggregation rather than at the mine shaft. Hence, when setting the purchase price, the central bank needs to understand the stage in the processing chain at which it is making its purchase. The further along the aggregation and processing chain the lower the subsequent processing costs, and hence the higher the possible purchase price.

The example below (Figure 1) illustrates the possible buying points.

Potential buying points in ASGM distribution and processing flow.

Purchase at the first trading point would require a discount for the costs and risks incurred during subsequent processing while purchase at the second trading point would need to compensate the seller for these costs. For example, the Bank of Mongolia uses local commercial banks as its point of purchase; the banks carry all the costs up to their vaults, thus reducing the Bank of Mongolia’s overheads. The Philippines Central Bank, on the other hand, buys from aggregators close to the gold fields.

What to include in the purchase price

This section assumes that the bank’s ASGM purchase program has a single objective of buying gold to add to its foreign reserves with a break even position (no profit or loss objective) over time. This strategy applies to paying a percentage discount on spot or paying a price based on actual costs (options 2 and 3 above).12

To determine the purchase price the central bank will refer to requirements set out in its accounting standards; these will specify the costs the bank should consider when calculating the value of its ASGM purchases. Included will be direct inventory costs and indirect costs related to purchases that the profit and loss statement reports as operating costs.

The central bank may undertake a project, or contract with a third party, to help identify all the costs incurred in operating its purchase program. This will distinguish between indirect costs that can be included in the profit and loss as operating costs, and direct costs for inclusion in the value of the inventory asset. This exercise will identify not only costs but also their quantity, the expected volume of sales and some estimate of the potential volatility of each. This is important for apportioning indirect costs in the pricing formula.

For indirect costs that the central bank cannot directly attribute to each purchase – and which cannot therefore be included in the inventory – the pricing formula will allocate them across the expected volume of purchases and include that amount when determining the purchase price.

In parallel, the pricing mechanism needs to develop a process that allocates the identified direct costs of each purchase to the value of the inventory asset.

Assuming a break-even scenario, the price paid to the producer will equal the market value of monetary gold, less the value of direct costs inventoried with each purchase, less the allocation of indirect costs per purchase the bank needs to recover for the program to break even.

During 2023 and much of 2024 gold prices rose steeply. This situation disguises the risks involved in paying a fraction of the current international price without reference to the underlying cost structure and volatilities. Such an approach carries a high risk of criticism should subsequent price corrections create losses in the central bank’s ASGM program. Consequently, a central bank may wish to consider including a risk discount to cover possible price volatility, especially if any review of the pricing mechanism is infrequent. This highlights the need for a monitoring program that justifies the purchase price and related discounts/premiums.

If the central bank is acting as a fiscal agent for the government in the gold market, the determination of royalties, vendor taxes or licensing costs should not form part of the purchase price.13 As discussed, such costs can complicate the bank’s gold buying operations and have the potential to conflict with other objectives.

Paying a discount on the current LBMA price

Currently, the most common pricing policy is to pay at a discount to the current LBMA price.

Gold is a mineral where processing costs from doré to monetary gold are a small percentage of the mineral’s inherent value, so miners receive a high proportion of the LBMA value. The discount may be for a set percentage (such as in Ecuador), or a fixed amount (as in Mongolia) or for variable rates reflecting doré quality and related processing costs (as in the Philippines). Regardless of how a bank specifies its discount it should have a framework to justify it.

When setting a discount rate, the central bank applies the process described in the section What to include in the purchase price to determine purchase price, and converts this to the percentage discount needed to recover costs. For example, the Bank of Ecuador breaks its price setting into several stages that include shipping the gold from purchase point to the bank and the subsequent processing stages where it is refined as monetary gold. This is set out in the BCE Pricing Framework (Table 1) below.

The Ecuador example shows how the bank applies a discount for gold price sensitivity.14 Such a discount may serve several purposes. First, it may provide a buffer to cover gold price fluctuations between the time the doré is purchased and its recognition as monetary gold at market value. Second, it may allow the bank to bring its offered gold price to a level that ensures market neutrality.

Another refinement of this approach, illustrated in Table 2, is for central banks to vary their prices according to the finesse of the gold. This approach may be appropriate in situations where there is wide variability in the quality of gold offered to the central bank purchase program.

Table 1: BCE Pricing Framework

Component

Description

Contribution rate

Operational cost rate (a)

The accumulated operational costs of the BCE from January up to the calculation month, divided by the accumulated purchases from January up to the calculation month

1.38%

Certification or sale cost rate (b)

The cost of refining services, including reception, storage, weighting, melting, laboratory analysis by the refinery, refining the gold, and transportation

0.38%

Gold price sensitivity (c)

A calculation of the bootstrap standard deviation of the gold price, which is performed monthly (allowance for volatility)

0.11%

Discount rate (d) = (a+b+c)

The sum of:

operation cost rate

certification or sales cost rate and

gold price sensitivity

1.87%

Table 2: Discount for ASGM finesse

% gold assay

Metal recovery factor

Processing cost

(Philippine peso/troy oz.

of material received)

Four main reasons explain how banks may incur ASGM losses:

It has paid above spot for the original gold

It paid spot but its processing costs are excessive

The national currency has appreciated since purchase

The price of gold has declined.

Each cause of loss produces different challenges for the central bank to manage and explain.

The time between purchasing the gold and its recognition as monetary gold can be considerable. The central bank may employ a policy whereby it accumulates gold for reasons of economy of scale, i.e. until it accumulates sufficient volume to efficiently ship to a refinery for final processing. During this holding period the central bank may face losses from appreciation of the national currency and/or declines in the international price of gold. Beyond including a risk allowance in the pricing formula, there is limited scope for managing such unknown costs and the central bank should treat the losses on gold as realised.

Recognising ASGM gold as a reserve asset

Recognition of ASGM purchases as monetary gold occurs once the gold reaches monetary gold standard.15 The normal practice is to value monetary gold at fair value in conformity with the practice for the broader foreign reserve assets portfolio and with IMF reserves template reporting.16

When determining its pricing policy, a central bank needs to consider two sets of costs. The first is the initial purchase and the cost of aggregating the gold and processing it to the monetary gold finesse of 0.995. The second relates to any further refining of the gold to the higher LGD standard for use in international gold markets. The availability of refineries in each country will influence a central bank’s decision on its final refining standard. If a country has a LBMA refinery close by, it could combine the two sets of costs. Otherwise, it is likely to choose to split these two steps and just refine the gold to monetary gold standard, deferring any future refining to LGD standard. Anecdotal evidence suggests that, at this time, central banks choose not to smelt over 90 percent of ASGM gold to LGD form.

Related pricing considerations

Reviewing and reporting the pricing framework

To avoid losses from running its ASGM program, the central bank needs to continually manage its purchase and processing arrangements to ensure optimal efficiency within its mandate. This should include a competitive tendering process for any third-party services and active monitoring of ASGM related contracts that will satisfy independent review.

An integral feature of any central bank ASGM gold purchase program is a process of frequent and ongoing review of how it sets its purchase price. The review will ensure that the price continues to meet the objectives defined in the gold purchasing mandate while managing the level of risk associated with the program. The maintenance of a gold purchasing system in the accounts will allow the monitoring of costs and the level of over/under recovery.

When establishing the purchase program the bank should consider financial outcomes alongside other objectives. That could be break even, to never run at a loss, or to always achieve a return on revenue after expenses. This consideration may lead the bank to the conclusion that its pricing mechanism is working against its other objectives. To help avoid this, the bank will need a mechanism to ensure that:

Its model captures all costs and revenues

The allocation of direct costs to inventory operates correctly

The system captures all the relevant indirect operating expenses

It effectively estimates purchase volumes as a denominator in order to allocate indirect costs

The bank treats over or under recovery of its costs according to its policies

The frequency at which the bank resets the purchase price is effective.

The design of the monitoring program will depend on whether the bank adjusts its discount rate on a regular basis or sets an annual rate to be reviewed at year end. It is important that the central bank develops a system that can meet the pricing and transparency required under its mandate.

In the event of operating at a loss the bank should reconcile the costs against its delegated mandates and provisions with the law covering the event of the losses. This need not require compensation for losses but should allow the bank to incur losses while achieving its specified objectives in the gold buying mandate. Good governance requires a central bank to report on the objectives and outcomes of any gold purchase program. This will include the basis for determining the ASGM purchase, and how closely the pricing matches the program’s financial objectives. In-depth information does not need to be disclosed but there should be sufficient detail to demonstrate that the bank is actively monitoring its performance and can explain its outcomes.

Options to defer refining and recognition as monetary gold

Situations exist where central banks wish to defer recognising gold as monetary gold as they believe this also defers accounting for losses. There is, however, limited scope for this. As the accounting section explains, the bank records ASGM gold as inventory valued at the lower of cost or NRV, while it records processed monetary gold as a foreign currency asset at fair value.

If the fair value of gold declines, the bank may defer processing the gold to avoid recognising refining expenses and any fair value revaluation losses; holding costs are an infrastructure cost that do not impact the value of the gold. This is only possible until the value of the gold – the major component of the gold price – falls below the doré’s original inventory valuation. At this point, the bank should revalue the gold inventory at its lower NRV and recognise the loss in its profit and loss statement as a realised loss.

Treatment of gains and losses on recognition as monetary gold

On converting ASGM gold to monetary gold the bank recognises the monetary gold at market value rather than at cost. Best practice requires the bank to recognise any gain or loss arising from this change as a realised gain or loss in its profit and loss statement. Generally accepted accounting practices treat such gains and losses as realised, thus placing them beyond the scope of the bank’s policies for realised and unrealised revaluation gains and losses.

Responses to reporting losses on ASGM gold purchases

A central bank should recognise losses on its ASGM program either through a decrease in the holding value of ASGM doré inventory or on its conversion to monetary gold. Either way, the consequences of reporting a loss can invoke criticisms that central banks should be prepared to counter. For example, they may be accused of providing an internal subsidy to domestic miners; of fraud; of a breach of mandate; of wasting public resources; or simply of incompetence. Bank critics will not hesitate to use such losses as an opportunity to attack the central bank in any area where it can find leverage.

Central bank critics often demand efficiency audits by the government, or via a third-party audit, in a search for errors upon which to base broader attacks regarding central bank independence. Unless actively managed, weaknesses in the ASGM program potentially present an Achilles heel.

To counter criticisms the bank needs to be proactive in the following:

Publish its gold purchasing mandate

Publish its performance in achieving its mandate

Explain its gold pricing framework in relation to its mandate

Identify the cause(s) of any losses.

In some situations the bank’s mandate may include the achievement of certain positive social objectives as part of a government’s broader reform initiative for the ASGM sector. This can be useful in explaining any losses, and it highlights the importance of having a clear and well documented mandate to support the bank’s domestic gold buying activities.

A common assumption when accounting for the purchase of ASGM doré is that the value of the gold classified as inventory is equal to the purchase price. The situation is more complicated and the following discussion, which covers the accounting of non-monetary gold, adopts the requirements of International Financial Reporting Standards.

The relevant standard covering accounting for non-monetary gold is IAS 2 inventory. As the common practice is for central banks to hold doré as a resource to produce monetary gold it is appropriate to treat doré as a non-financial asset, rather than as a financial asset. The default situation is that doré does not meet monetary gold definitions and so banks exclude it from foreign reserves portfolio accounting and reporting.

IAS 2 requires the recognition of doré at the lower of cost or NRV. This raises two relevant issues in determining the pricing policy for central bank purchases. First, which costs should the bank include in the cost of the inventory asset and, second, what happens if the total cost is greater than the NRV?

Costs to recognise for inclusion as inventory

As discussed, the accounting standard splits costs into indirect and direct and requires the inclusion of direct costs in the inventory value. In addition to costs paid at the point of purchase, IAS 2 requires an entity to recognise costs that are directly related to transforming the asset to the state where it can be used to produce the final product (monetary gold). These include:

Tax-related duties (note these are not taxes on vendors that the central bank may collect as a fiscal agent)

Transportation costs

Insurance during transportation

Handling costs

Other costs that are directly attributable to the acquisition.

The costs of purchase, as well as the price paid, are reduced by trade discounts, rebates and similar items.

Any discounts received should be included, as should any government subsidy received for achieving elements identified in the mandate for which the government has undertaken to reimburse the bank.

The standard allows the exclusion of abnormal costs from the value of inventory arising from:

Material waste

Labour

Other production conversion inputs

All administrative overhead and selling costs.

The bank will need to develop a policy for the treatment of these irregular costs. Does it include allocation for these when it calculates the purchase price or does it wish to carry the costs as part of its operating expenses?

Costs excluded from inventory but relevant when calculating the purchase price

The standard allows the producer to classify indirect items as operating costs, so the bank excludes them from the cost of the doré. For the central bank these arise from the establishment and operation of the SGBP infrastructure and include:

Assay costs

Buying office costs

Bidding costs

Security costs

Storage costs.

What happens if the value of the inventory is greater than the net realisable value?

If processing the doré results in costs greater than the amount that the bank could receive from sale (NRV), the standard requires the bank to expense the difference to reduce the asset to the lower of cost or NRV as a realised item and report it as an operating expense in the profit and loss section of its income statement.

Cost of conversion to London Good Delivery

A central bank faces a different situation if there is a LBMA refinery in close proximity. When this is the case, the final refining of ASGM doré would be to LGD bars that meet international market standards. If there is no LBMA refinery the central bank faces a choice as to when it recognises the doré as monetary gold. A local refinery can refine the gold to a .995 standard, at which stage the gold meets the IMF’s definition of monetary gold without the bank incurring the costs of shipping and final refining to LGD standard.

Such a solution will allow a central bank to exclude LGD refining expenses from its calculations of the ASGM purchase price. Should the central bank need to employ the two-stage LGD refining, it will include the cost of processing to LGD standard as a discount to fair value.

Recognition of gold as a reserve asset

The recognition of gold as a foreign reserve asset usually requires a change of valuation basis.18 Fair value, or market price, replaces the lower of cost or NRV. The change in classification requires the central bank to recognise any gains or losses arising from the reclassification as a realised revaluation profit or loss. The table below illustrates the accounting entries for a gain or a loss on reclassification for different values of inventory.

Gain on reclassification

DR

CR

Monetary gold

1,994.00

Inventory

1,899.00

Realised revaluation gain

95.00

Loss on reclassification

Monetary gold

1,994.00

Realised revaluation loss

6.00

Inventory

2,000.00

Inventory management considerations for ASGM purchases

Accounting conventions provide four options for managing the flow of inventory:

First in, first out method (FIFO)

Last in, first out method (LIFO)

Specific identification method

Weighted average method.

These are important as they allow central banks to assign the cost of the doré to the final monetary gold product. Each approach offers different paths for allocating inventory costs. IFRS prohibits LIFO, but FASB (US GAAP) allows it as at the date of publication.

For central banks managing their stock of non-monetary gold, specific identification offers the most flexible option for matching costs with processing. This method provides central banks with some scope to manage how they assign inventory costs to monetary gold. If gold prices are declining, the central bank can pick its lowest value items of doré to send for smelting, thus reducing potential losses where the processed gold value exceeds its fair value. While there is some flexibility there is a marginal benefit and the selection of doré to send for processing is better managed as part of a broader strategic plan.

Conclusion

In appropriate circumstances central bank purchases of ASGM gold production may help the central bank to achieve its core functions and contribute to improvements in the domestic ASGM sector. Any such program should be enabled in law, detailing the objectives and scope of operations consistent with central banking functions. A strategic plan should explain how the bank’s purchases comply with its legal mandate and should define its interactions with other government agencies who have an interest in the ASGM sector. As discussed, close cooperation with other parties in the ASGM sector is critical to achieve the range of outcomes identified by each party.

Central banks have a role to play in the ASGM sector and the bank’s policy on pricing forms a core element of this. When defining its role, it is important that engagement is consistent with other central bank functions and that its pricing is consistent with the legal and economic environment in which it operates. The bank’s pricing and purchasing should not involve hidden subsidies or market distortions, and its pricing policy should not leave the bank with losses that fall outside of its mandate.

Footnotes

1ASGM refers to gold mining conducted by individuals or small groups with limited capital investment. It covers all forms of extracting or recovering gold.

2For example, Central bank domestic ASGM purchase programs; World Gold Council: State gold buying programs – Effective instruments to reform the artisanal and small-scale goldmining sector.

3We refer herein to the semi-processed production purchased from the ASGM sector as both ‘gold’ and its technically appropriate name of ‘doré’.

4The International Monetary Fund (IMF) recognises monetary gold as a reserve asset class and provides for separate reporting and specific valuation for its disclosure in the International Reserves and Foreign Currency Liquidity template.

5The Federal Reserve holds gold certificates, while the US Treasury holds the physical gold that backs them.

6WGC has no specific policy stance on this issue but it will assist those central banks where the government and central bank agree that a SGBP is appropriate within the central bank’s mandate.

7Tanzania's mining regulator has ordered all mining firms and traders exporting gold to allocate at least 20% of the commodity for sale to the central bank to bolster the bank's move to diversify its foreign reserves (September 2024).

8Monetary Gold includes gold of at least 995 finesse and includes gold in forms that fall short of London Good Delivery standards.

9Ecuador Mining Act states in Article 49, Right to Market Freely: “The holders of mining licenses can market their production freely, either within the country or abroad. Gold from legally authorised, small-scale mining, however, shall be marketed by the Central Bank of Ecuador, either directly, or through financial institutions duly authorised by the Central Bank to act as intermediaries.”

10Philippines - Republic Act No. 7653, Section 69, Purchases and Sales of Gold: “The Bangko Sentral Ng Pilipinas may buy and sell gold in any form, subject to such regulations as the Monetary Board may issue. “The purchases and sales of gold authorised by this section shall be made in the national currency at the prevailing international market price as determined by the Monetary Board.”

11Article 24: Precious Metals: “Banco de la República will perform operations of purchase, sale, processing, certification and exportation of precious metals. Without prejudice of the free competition provided in Article 13 of Law 9 of 1991, Banco de la República will purchase all nationally produced gold offered thereto. The Board of Directors will regulate the manner how Banco de la República will carry out the above operations.”.

12Paying spot or a premium involves a different strategy not covered in this paper.

13An exception to this would be a situation where the purchaser, rather than the vendor, is responsible for paying a sales tax.

14This is an optional feature that the BCE does not apply in all cases.

15The IMF definition for monetary gold is broader than that for LGD bars. A central bank may refine gold to the required .995 standard for recognition as monetary gold, although such gold incurs a discount when traded internationally. If a country contains a LBMA licensed refinery then it may get the doré refined to LGD form without shipment outside the country. A non-LBMA refinery will refine to monetary gold standard but not LGD form, which may be adequate for the central bank’s reserve management strategy.

16Note that international standards do not require the reporting of monetary gold at fair value. See www.gold.org/gold-standards/gold-accounting for a detailed discussion of central bank practices and the recommended accounting approach.

17This section is meant for informational purposes only and does not constitute financial, accounting, legal or tax advice. Readers should consult their own legal, tax, accounting and financial advisors before making any decisions based on the information contained herein.

18While IFRS does not require a change in valuation for monetary gold, the default approach, supported by the IMF, is for central banks to recognise monetary gold at fair value. See: www.gold.org/gold-standards/gold-accounting.

The use of the statistics in this information is permitted for the purposes of review and commentary (including media commentary) in line with fair industry practice, subject to the following two pre-conditions: (i) only limited extracts of data or analysis be used; and (ii) any and all use of these statistics is accompanied by a citation to World Gold Council and, where appropriate, to Metals Focus or other identified copyright owners as their source. World Gold Council is affiliated with Metals Focus.

The World Gold Council and its affiliates do not guarantee the accuracy or completeness of any information nor accept responsibility for any losses or damages arising directly or indirectly from the use of this information.

This information is for educational purposes only and by receiving this information, you agree with its intended purpose. Nothing contained herein is intended to constitute a recommendation, investment advice, or offer for the purchase or sale of gold, any gold-related products or services or any other products, services, securities or financial instruments (collectively, “Services”). This information does not take into account any investment objectives, financial situation or particular needs of any particular person.

Diversification does not guarantee any investment returns and does not eliminate the risk of loss. Past performance is not necessarily indicative of future results. The resulting performance of any investment outcomes that can be generated through allocation to gold are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. The World Gold Council and its affiliates do not guarantee or warranty any calculations and models used in any hypothetical portfolios or any outcomes resulting from any such use. Investors should discuss their individual circumstances with their appropriate investment professionals before making any decision regarding any Services or investments.

This information may contain forward-looking statements, such as statements which use the words “believes”, “expects”, “may”, or “suggests”, or similar terminology, which are based on current expectations and are subject to change. Forward-looking statements involve a number of risks and uncertainties. There can be no assurance that any forward-looking statements will be achieved. World Gold Council and its affiliates assume no responsibility for updating any forward-looking statements.

Information regarding the LBMA Gold Price

The LBMA Gold Price is administered and published by ICE Benchmark Administration Limited (IBA). The LBMA Gold Price is a trademark of Precious Metals Prices Limited and is licensed to IBA as administrator of the LBMA Gold Price. ICE and ICE Benchmark Administration are registered trademarks of IBA and/or its affiliates. The LBMA Gold Price is used by the World Gold Council with permission under license by IBA and is subject to the restrictions set forth here (http://www.gold.org/terms-and-conditions).