Central bank gold statistics: Momentum eases in January while demand base broadens

3 March, 2026

January Highlights

- Broadening demand base: While we see continuation of gold buying from central bankers who purchased gold in the previous year, the broadening of the demand base could be an emerging theme. Bank Negara Malaysia (3t) made its first net purchase of gold since 2018 while the Bank of Korea looks to resume gold investments for the first time since 2013.

- Geopolitical uncertainty remains a persistent backdrop to central bank demand, with January’s high volatility being a notable exception.

Notable takeaways

- Central banks bought a net 5t in January, as momentum eased at the start of the year – this is compared to a monthly average of 27t in 2025.

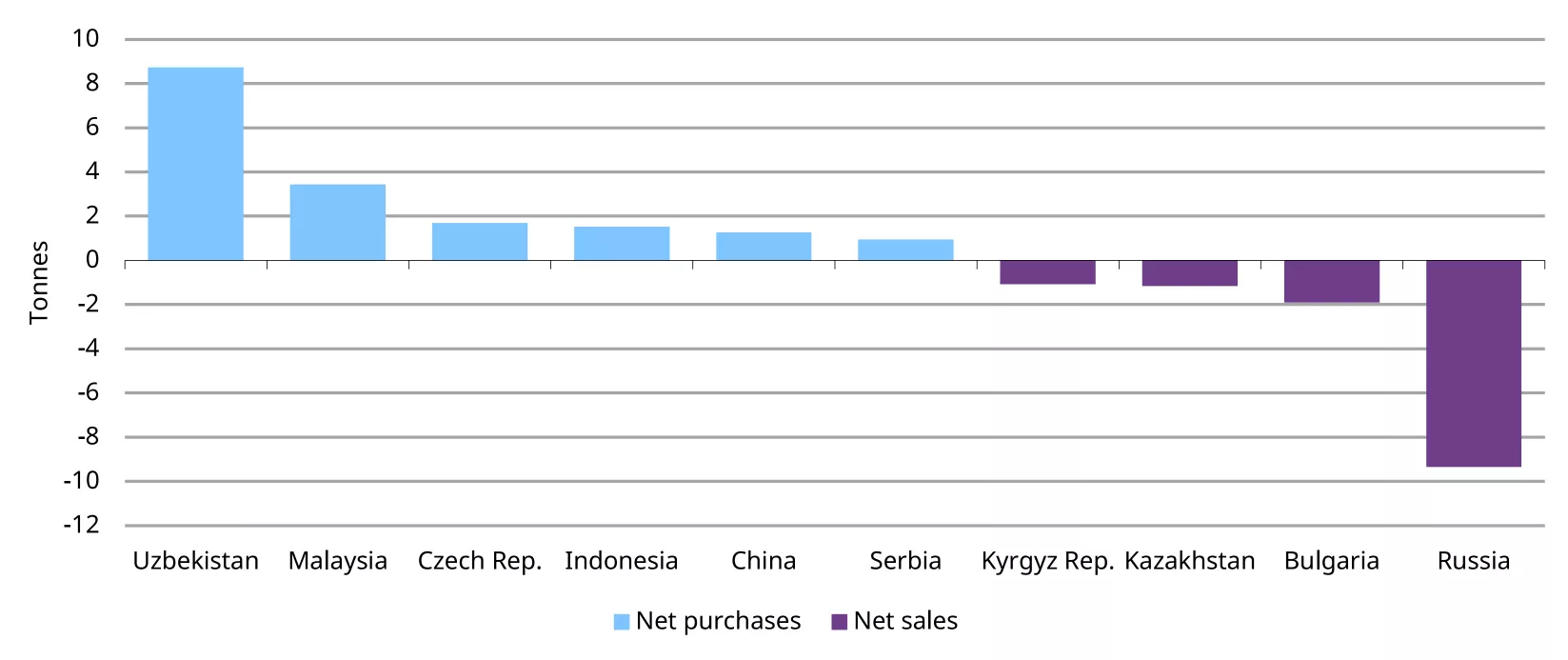

- Buying was led by Central and East Asian central banks, with Eastern European names also adding to reserves. Notably, Central Asia saw activity on both sides of the ledger — Uzbekistan (9t) among the top buyers while Kazakhstan (1t) was a net seller. Russia was the top seller this month (9t).

- The Bulgarian National Bank (BNB) sold 2t of gold in January. The 2t drop from the BNB corresponds to a 2t increase in the ECB gold reserves, as Bulgaria joins the European Union as its 21st member.

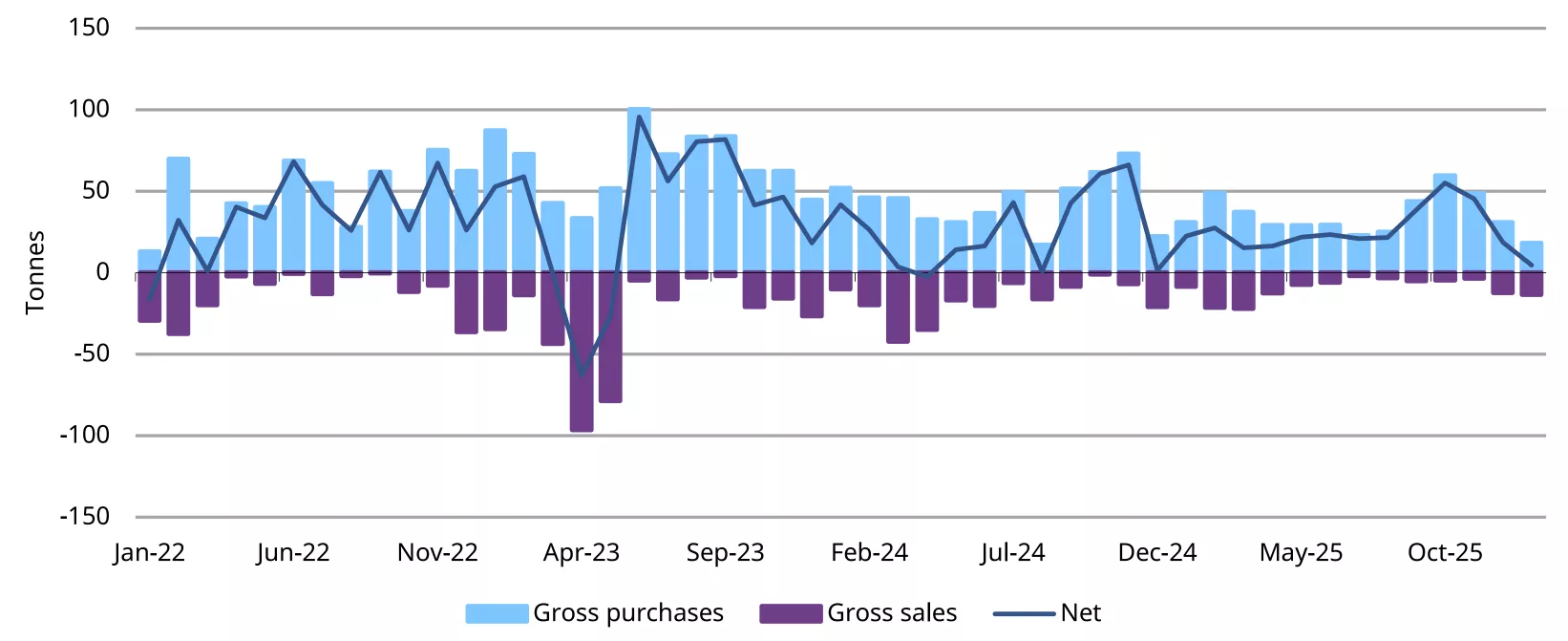

Central bank gold buying momentum eased at the start of the year, compared to the prior 12-month average of 27t. Net purchases for the month of January totalled 5t (Chart 1). Volatile gold prices and the holiday season may have given some central banks pause, though geopolitical tensions, which have shown little sign of abating, are likely to keep accumulation going through 2026 and beyond.

Chart 1: Central banks buying momentum intact even as gold prices climb

Monthly reported central banks activity, tonnes*

*Data to 30 January 2026, where available

Source: IMF, respective central banks, World Gold Council

Reported activity in January has been concentrated in:

- The Central Bank of Uzbekistan bought 9t the month, continuing its buying streak since October. The purchase lifted its gold reserves to 399t. The growth in Uzbekistan’s gold reserves has been quite precedented, it stood at 57% in the same period in 2020 and grew to 86% of its reserves as of January 2026.1

- Bank Negara Malaysia was a new name amongst the gold purchasers, having bought 3t in January – its first increase since 2018. The central bank lifted its gold reserves to 42t, or 5% of its total reserves as of the end of January.

- Other central banks that bought gold this month include Czech Republic (2t), Indonesia (2t) China and Serbia at 1t each. China’s 15 consecutive months of gold buying has lifted its gold reserves to nearly 10% of total reserves.

- Bank of Russia was the largest net seller this month (9t). This is followed by the Bulgarian National Bank (2t), which transferred the gold to the ECB as part of the country’s euro adoption which took place on 1st January 2026, making it the 21st member of the European Union.2 The Kazakhstan and the Kyrgyz Republic also decreased their gold reserves, each by one tonne.

Chart 2: Central bank gold purchases off to a slower start in 2026

Central bank net purchases and sales, tonnes*

*Data to 30 January 2026, where available.

Source: IMF, respective central banks, World Gold Council

Bank of Korea

The Bank of Korea (BOK) announced plans to incorporate overseas-listed physical gold ETFs into its foreign reserve portfolio from Q1 2026, marking its first gold-related investment since 2013. The BOK cited liquidity and ease of tradability as key advantages of the ETF structure over physical gold. The BOK currently holds 104t of physical gold (roughly 4% of its total reserves), placing it 41st in ranking among global peers. Our Central Bank Gold Reserves Survey 2025 found that accessing gold via ETFs is rather uncommon amongst central banks: none of the respondents whom we surveyed had opted for it as a method to purchase gold.

Conclusion

The broadening of demand from central bankers might be an emerging key theme in 2026. As we have seen in January, both Malaysian and Korean central banks have resumed interest in increasing gold exposure after prolonged absences. The next 10-15 days could prove crucial in shaping the geopolitical backdrop this year, as US-Iran tensions continue to escalate with little indication of diplomatic resolution in sight. The strong pace of gold accumulation by central bankers since 2022 has been intertwined with how nations position themselves in a shifting world order.

Footnotes

1Based on LBMA Gold Price PM in USD on 30 January 2026.

Disclaimer

Important information and disclaimers

© 2026 World Gold Council. All rights reserved. World Gold Council and the Circle device are trademarks of the World Gold Council or its affiliates.

All references to LBMA Gold Price are used with the permission of ICE Benchmark Administration Limited and have been provided for informational purposes only. ICE Benchmark Administration Limited accepts no liability or responsibility for the accuracy of the prices or the underlying product to which the prices may be referenced. Other content is the intellectual property of the respective third party and all rights are reserved to them.

Reproduction or redistribution of any of this information is expressly prohibited without the prior written consent of World Gold Council or the appropriate copyright owners, except as specifically provided below. Information and statistics are copyright © and/or other intellectual property of the World Gold Council or its affiliates or third-party providers identified herein. All rights of the respective owners are reserved.

The use of the statistics in this information is permitted for the purposes of review and commentary (including media commentary) in line with fair industry practice, subject to the following two pre-conditions: (i) only limited extracts of data or analysis be used; and (ii) any and all use of these statistics is accompanied by a citation to World Gold Council and, where appropriate, to Metals Focus or other identified copyright owners as their source. World Gold Council is affiliated with Metals Focus.

The World Gold Council and its affiliates do not guarantee the accuracy or completeness of any information nor accept responsibility for any losses or damages arising directly or indirectly from the use of this information.

This information is for educational purposes only and by receiving this information, you agree with its intended purpose. Nothing contained herein is intended to constitute a recommendation, investment advice, or offer for the purchase or sale of gold, any gold-related products or services or any other products, services, securities or financial instruments (collectively, “Services”). This information does not take into account any investment objectives, financial situation or particular needs of any particular person.

Diversification does not guarantee any investment returns and does not eliminate the risk of loss. Past performance is not necessarily indicative of future results. The resulting performance of any investment outcomes that can be generated through allocation to gold are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. The World Gold Council and its affiliates do not guarantee or warranty any calculations and models used in any hypothetical portfolios or any outcomes resulting from any such use. Investors should discuss their individual circumstances with their appropriate investment professionals before making any decision regarding any Services or investments.

This information may contain forward-looking statements, such as statements which use the words “believes”, “expects”, “may”, or “suggests”, or similar terminology, which are based on current expectations and are subject to change. Forward-looking statements involve a number of risks and uncertainties. There can be no assurance that any forward-looking statements will be achieved. World Gold Council and its affiliates assume no responsibility for updating any forward-looking statements.

Information regarding the LBMA Gold Price

The LBMA Gold Price is used by the World Gold Council with permission under license by ICE Benchmark Administration Limited and is subject to the restrictions set forth here (www.gold.org/terms-and-conditions).

Information regarding QaurumSM and the Gold Valuation Framework

Note that the resulting performance of various investment outcomes that can be generated through use of Qaurum, the Gold Valuation Framework and other information are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. Neither World Gold Council (including its affiliates) nor Oxford Economics provides any warranty or guarantee regarding the functionality of the tool, including without limitation any projections, estimates or calculations.

Information from ICRA Analytics Limited

All information obtained from ICRA Analytics Limited contained in this document is subject to the disclaimer set forth here (www.icraanalytics.com/terms-of-use/disclaimer).