Central Bank Gold Statistics: Central banks ramp up gold buying in October

2 December, 2025

Highlights

- Central banks bought a net 53t in October, 36% higher m/m and the largest monthly net demand y-t-d

- A familiar set of buyers – led by a resurgent National Bank of Poland – drove the gains

- Total y‑t‑d reported buying through October solidly positive at 254t, but slower than previous years.

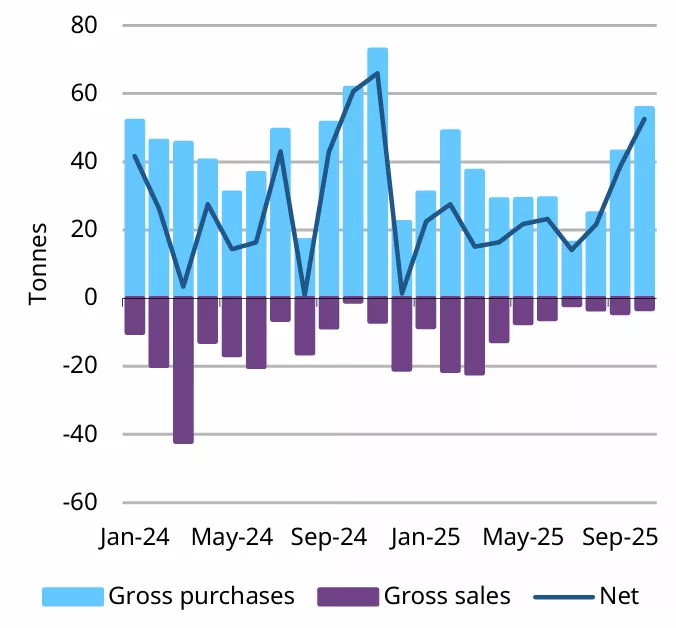

Central bank demand for gold remained robust in October, totalling 53t (+36% m/m) and continuing the strong trend seen throughout the year (Chart 1). Buying remained concentrated among a small number of central banks, led by the National Bank of Poland which became active again during the month.

Chart 1: Central bank gold buying has picked up pace in recent months

Monthly reported central banks activity, tonnes*

*Data to 31 October 2025, where available.

Source: IMF, respective central banks, World Gold Council

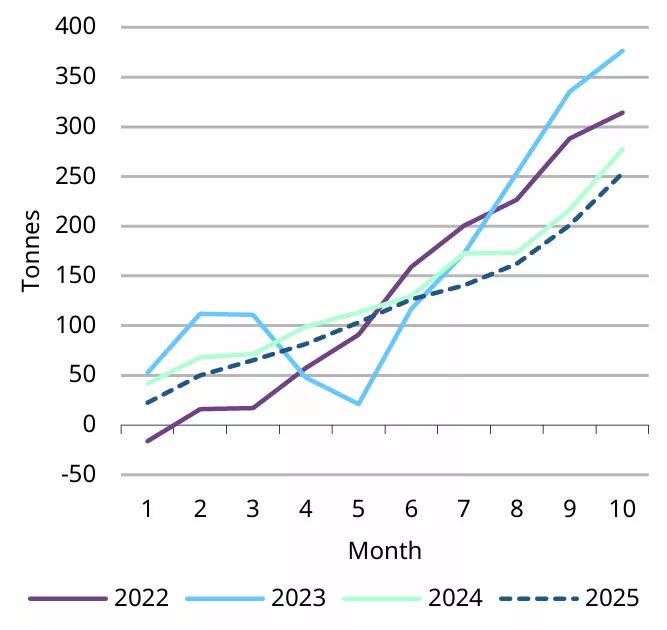

Y-t-d reported net purchases through October totalled 254t, a slower pace when compared with the previous three years (Chart 2). This possibly reflects the impact of higher prices. Even so, sustained activity from emerging-market central banks – supported by the findings from our annual survey – strongly suggests that these purchases are strategic rather than opportunistic, reinforcing gold’s importance amid persistent macroeconomic uncertainty.

Chart 2: Y-t-d reported buying trails the previous three years

Cumulative reported gold buying, tonnes*

*Data to 31 October 2025, where available.

Source: IMF, respective central banks, World Gold Council

The buyer cohort in October was dominated by names we’ve seen throughout the year, with a handful of central banks accounting for the bulk of additions:

- The National Bank of Poland re-entered the market in October, having paused its buying since May. After recently increasing its target gold allocation to 30%,1 the purchase of 16t in the month lifted its gold reserves to 531t, 26% of total reserves at end-October prices.

- The Central Bank of Brazil bought gold for the second consecutive month, adding 16t in October following its 15t purchase in September. Its gold reserves now stand at 161t, accounting for 6% of total reserves.

- The Central Bank of Uzbekistan (9t), Bank Indonesia (4t), Central Bank of Turkey (3t), Czech National Bank (2t), National Bank of the Kyrgyz Republic (2t), Bank of Ghana (>1t), People’s Bank of China (>1t), National Bank of Kazakhstan (>1t) and the Central Bank of the Philippines (>1t) were also buyers in October.

At the time of writing, the Central Bank of Russia was the only bank to report a decline in gold reserves in the month – falling by 3t to 2,327t.

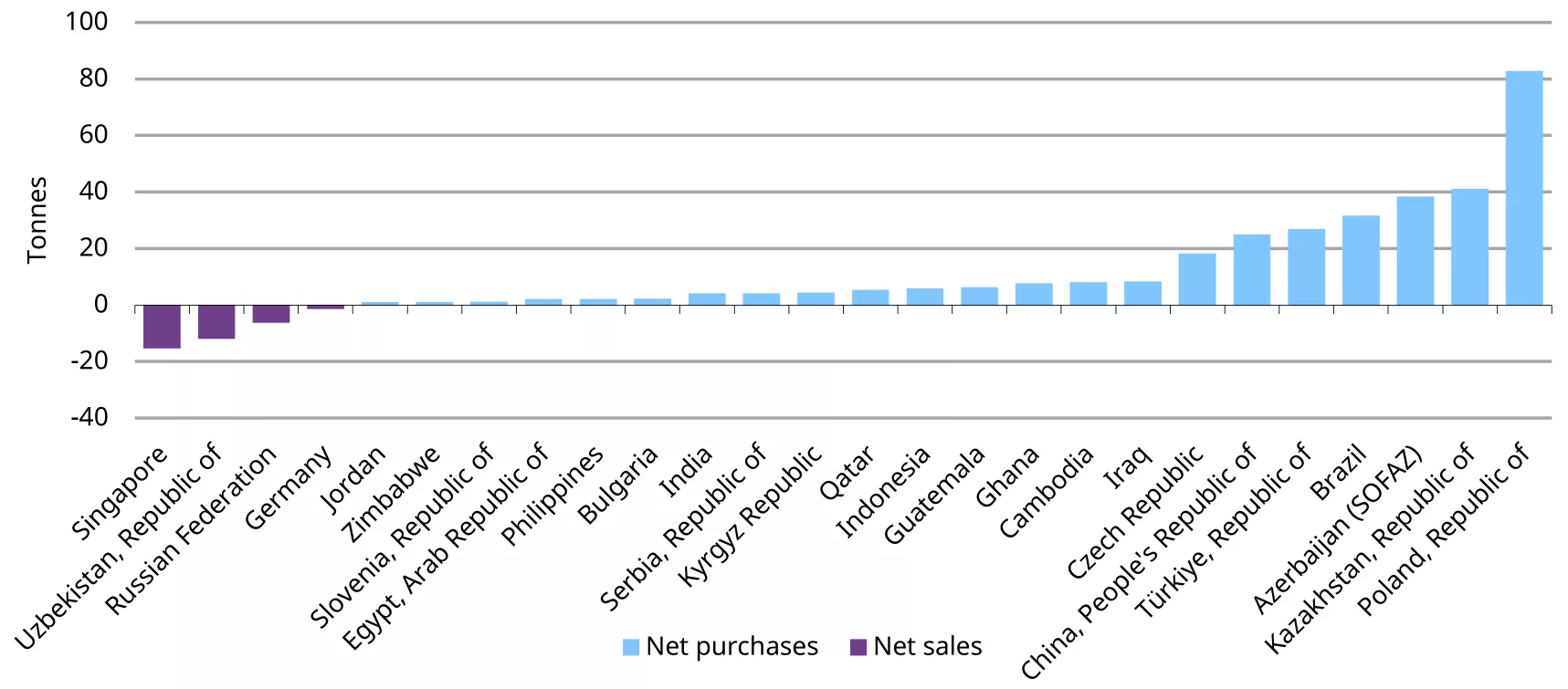

Year-to-date, the National Bank of Poland (83t) continues to be largest official-sector gold buyer, with double the purchases of the next largest buyer, Kazakhstan (41t) (Chart 3). While buying continues to be concentrated among emerging-market central banks, the list of buyers – old and new – remains broad.

Chart 3: The National Bank of Poland extends y-t-d buying in October

Y-t-d central bank net purchases and sales, tonnes*

*Data to 31 October 2025, where available.

Source: IMF, respective central banks, World Gold Council

Central banks eye bigger gold reserves

The National Bank of Serbia plans to boost its gold reserves to at least 100t by 2030, according to a recent statement from Serbian President Aleksandar Vucic.2 This long-term target represents a near-doubling of current holdings, which stood at 52t at the end of October, and signals a continued commitment to gold as a strategic asset in the country’s reserve portfolio.

At the recent LBMA conference in Kyoto, Madagascar and South Korea also signalled interest in increasing their gold reserves, though neither has provided a specific timeline for these plans.3

This reinforces the findings of our 2025 survey, which showed that 95% of respondents expected central bank gold reserves to increase in the year ahead.

Footnote:

1Central bank gold statistics: Central bank gold buying rebounds in August, World Gold Council.

2Bloomberg.

3Bloomberg.

Disclaimer

Important information and disclaimers

© 2025 World Gold Council. All rights reserved. World Gold Council and the Circle device are trademarks of the World Gold Council or its affiliates.

Reproduction or redistribution of any of this information is expressly prohibited without the prior written consent of World Gold Council or the appropriate copyright owners, except as specifically provided below. Information and statistics are copyright © and/or other intellectual property of the World Gold Council or its affiliates or third-party providers identified herein. All rights of the respective owners are reserved.

The use of the statistics in this information is permitted for the purposes of review and commentary (including media commentary) in line with fair industry practice, subject to the following two pre-conditions: (i) only limited extracts of data or analysis be used; and (ii) any and all use of these statistics is accompanied by a citation to World Gold Council and, where appropriate, to Metals Focus or other identified copyright owners as their source. World Gold Council is affiliated with Metals Focus.

The World Gold Council and its affiliates do not guarantee the accuracy or completeness of any information nor accept responsibility for any losses or damages arising directly or indirectly from the use of this information.

This information is for educational purposes only and by receiving this information, you agree with its intended purpose. Nothing contained herein is intended to constitute a recommendation, investment advice, or offer for the purchase or sale of gold, any gold-related products or services or any other products, services, securities or financial instruments (collectively, “Services”). This information does not take into account any investment objectives, financial situation or particular needs of any particular person.

Diversification does not guarantee any investment returns and does not eliminate the risk of loss. Past performance is not necessarily indicative of future results. The resulting performance of any investment outcomes that can be generated through allocation to gold are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. The World Gold Council and its affiliates do not guarantee or warranty any calculations and models used in any hypothetical portfolios or any outcomes resulting from any such use. Investors should discuss their individual circumstances with their appropriate investment professionals before making any decision regarding any Services or investments.

This information may contain forward-looking statements, such as statements which use the words “believes”, “expects”, “may”, or “suggests”, or similar terminology, which are based on current expectations and are subject to change. Forward-looking statements involve a number of risks and uncertainties. There can be no assurance that any forward-looking statements will be achieved. World Gold Council and its affiliates assume no responsibility for updating any forward-looking statements.

Information regarding the LBMA Gold Price

The LBMA Gold Price is administered and published by ICE Benchmark Administration Limited (IBA). The LBMA Gold Price is a trademark of Precious Metals Prices Limited and is licensed to IBA as administrator of the LBMA Gold Price. ICE and ICE Benchmark Administration are registered trademarks of IBA and/or its affiliates. The LBMA Gold Price is used by the World Gold Council with permission under license by IBA.

Published LBMA Gold Price information may not be indicative of future LBMA Gold Price information or performance. None of IBA, Intercontinental Exchange, Inc. (ICE) or any third party that provides data used to administer or determine the LBMA Gold Price (data providers), or any of its or their affiliates makes any claim, prediction, warranty or representation whatsoever as to the timeliness, accuracy or completeness of LBMA Gold Price information, the results to be obtained from any use of LBMA Gold Price information, or the appropriateness or suitability of using LBMA Gold Price information for any particular purpose. to the fullest extent permitted by applicable law, all implied terms, conditions and warranties, including, without limitation, as to quality, merchantability, fitness for purpose, title or non-infringement, in relation to LBMA Gold Price information, are hereby excluded, and none of IBA, ICE or any data provider, or any of its or their affiliates will be liable in contract or tort (including negligence), for breach of statutory duty or nuisance, or under antitrust laws, for misrepresentation or otherwise, in respect of any inaccuracies, errors, omissions, delays, failures, cessations or changes (material or otherwise) in LBMA Gold Price information, or for any damage, expense or other loss (whether direct or indirect) you may suffer arising out of or in connection with LBMA Gold Price information or any reliance you may place upon it.

LBMA Gold Price information provided by the World Gold Council may be used by you internally to review the analysis provided by the World Gold Council, but may not be used for any other purpose. LBMA Gold Price information provided by the World Gold Council may not be disclosed by you to anyone else.