Gold has gained more than 3% this week largely attributed to an escalation of geopolitical tensions linked to the Israeli-Palestinian conflict. 1

As a crisis hedge, gold has a solid history, driven by its lack of credit risk and negative correlation to risk assets. But it is likely that geopolitical tensions on their own might influence gold returns, even when accounting for the change in other factors. We set out to test this idea.

Capturing the transmission channels of geopolitical risk can be challenging. Political context, geographical concentration and the likelihood of proliferation all matter, as does whether the increase in risk comes from a perceived threat or an actual act of aggression.

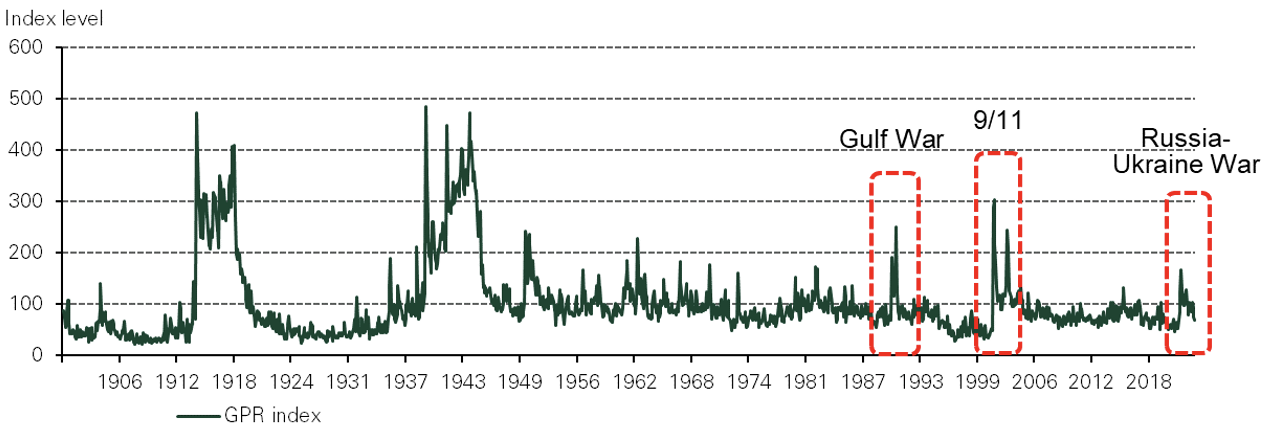

Also, many historical episodes are too idiosyncratic to act as useful guides. Fortunately, a number of indices exist to quantify geopolitical risk. Arguably the most well-known is the Geopolitical Risk (GPR) index by Matteo Iacoviello that measures both actual and perceived geopolitical tension.2 The GPR index has a reliable track record of reflecting observed impacts to underlying economic variables at a global level (Chart 1).

Chart 1. The Iacoviello GPR index consistently captures historical acts and threats of geopolitical tension

We use our Gold Return Attribution Model (GRAM) to quantify the impact of key drivers on gold returns, both on monthly and weekly frequencies.3 It is an invaluable and historically accurate guide. But from time to time, the model produces a more noticeable residual. When this occurs, the likely culprit is either a missing factor or a change in the sensitivity of gold to the existing factors.

In 2022, for example, there were at least two instances of these more sizeable residuals: in Q2 and Q3. We know subsequently that there was considerable central bank buying during these quarters, and the Russian invasion of Ukraine occurred in late February – two factors that are not explicitly included in our model and are likely candidates for missing variables. We don’t currently have a reliable series to capture non-reported monthly central bank buying, but the GPR could conceivably capture the additional impact of geopolitics on gold.

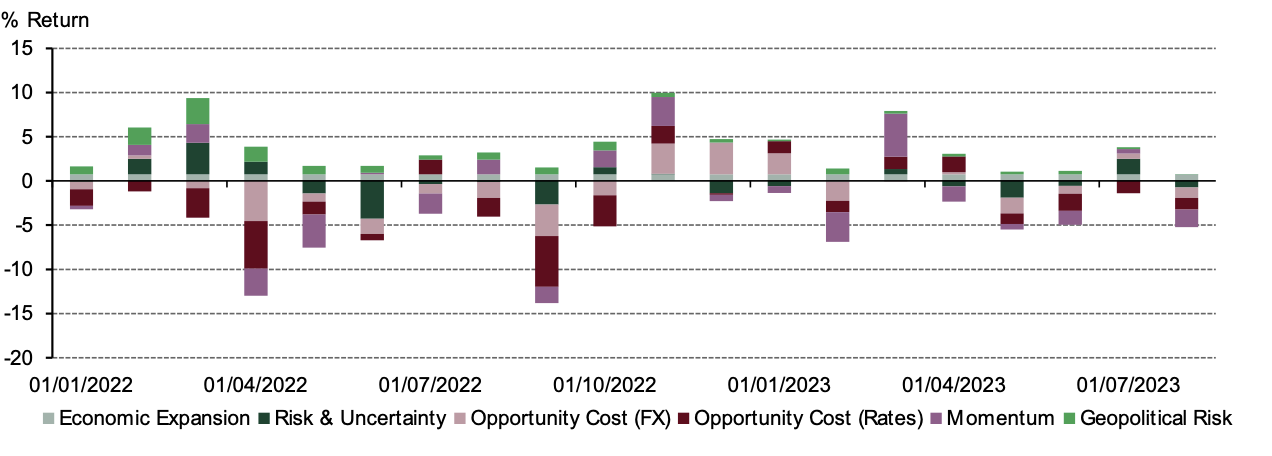

This is what our analysis shows. Even though the model already includes inflation, bond yields, currencies, crude oil and implied gold volatility – variables likely to respond to a rise in geopolitical tension – the impact of the GPR index is visible,4 and it adds to the model’s explanatory power (Chart 2).

Chart 2: By adding the GPR index to GRAM, we can quantify gold’s geopolitical risk premium

The conclusion we can draw from this is that gold – likely via investor flows – responds to elevated geopolitical risk even when controlling for the movement in the existing variables in the model. And we can attach a number to this response: an increase in the GPR index by 100 units holding all else constant, has a c.2.5% positive impact on gold’s return. For example, the GPR index rose from under 100 to over 250 at the start of the Russia-Ukraine conflict last year, while 9/11 saw it spike above 450 from under 50.

GPR index spikes have in recent times been short-lived, however. This partly reflects a shorter news cycle than in the past. It does not suggest that gold’s reaction is short-lived, as the follow-through from a spike to other variables and sentiment can potentially last longer. But there is also a slight medium-term risk for gold from a rise in tensions, via higher inflation for example, which could potentially delay a gold-friendly monetary pivot by the Fed and other central banks.

In summary, gold’s performance this week is not a coincidence and can be measurably attributed to the Israeli-Palestinian conflict. How long this effect will last will depend on the wider ramifications the conflict may have on the global economy. And, in either case, given the increased frequency and unpredictability of geopolitical risks, it further supports the case for a consistent, strategic allocation to gold.