The conventional wisdom that stocks and bonds are negatively correlated is a central component of most asset allocation strategies. But the correlation hasn’t always been negative – far from it, in fact – and there are increasing signs of strain in the relationship, prompting investors to ask: could the stock-bond correlation flip? In this blog, we consider that possibility, what it might mean for the average portfolio, and how gold could help to protect portfolio performance.

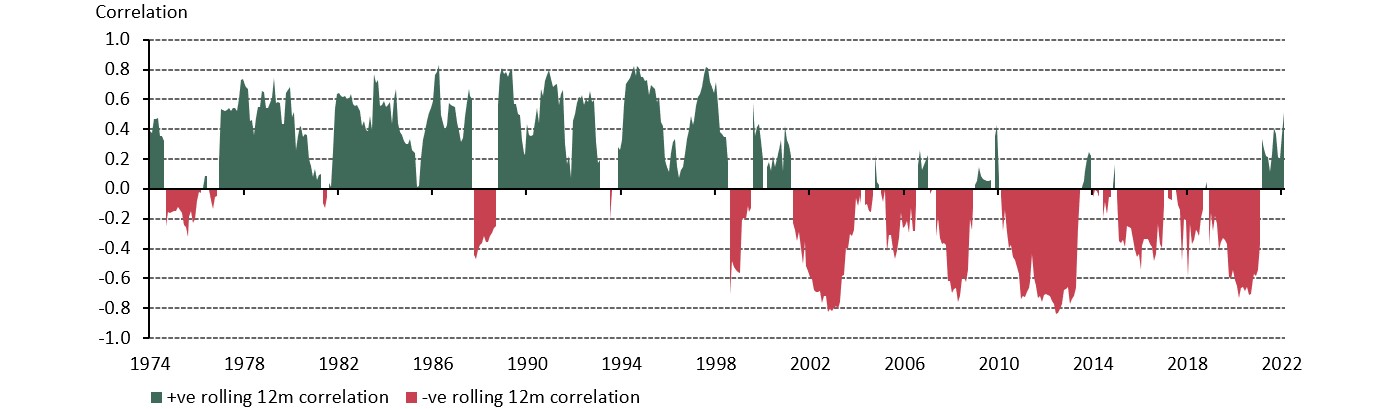

Much has been written about the origins of the negative correlation between equities and Treasuries [here, and here for example], an almost 25-year relationship which emerged in the wake of the 1997 Asian Financial Crisis (AFC) (Chart 1) and the low and stable inflation environment that resulted; an environment equally supportive to both bonds and equities.

The AFC saw inflation collapse in line with the cost of Asian-produced goods. At the same time, central banks began to introduce more explicit inflation targets, ushering in an era of benign, controlled, pro-cyclical inflation, in contrast to the counter-cyclical – often very high – inflation that had previously been the norm. This, among other factors, encouraged investors increasingly to use government bonds as a hedge against equities. And, for more than 20 years, the 60:40 portfolio became a widely-used illustrative standard in portfolio analysis.

Chart 1. Negative equity bond correlations weren't always a thing...

Notes: MSCI World Total Return index, ICE BofA Gov’t and Agency Total Return index, monthly data from January 1973 to December 2021

Source: Bloomberg, World Gold Council

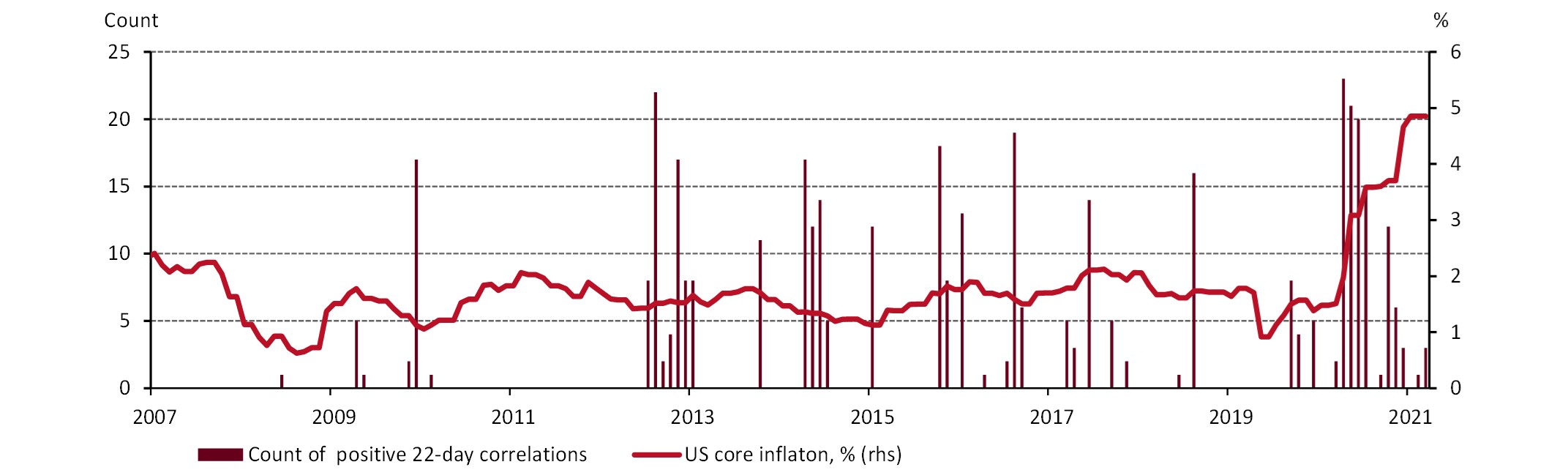

But change is afoot. The steep rise in inflation unleashed by the extraordinary monetary and fiscal stimulus of the last several years may yet prove to be stubbornly persistent or, perhaps worse, volatile – likely heralding a period of stop-start monetary policy. Analysis shows that the rise in core US CPI has been accompanied by increasingly frequent instances of positive equity-bond correlations (Chart 2). Could this be a pre-cursor to a return of the positive stock-bond relationship, arguably the most important input into asset allocation, that was largely in place for decades prior to 1997?

Chart 2. Positive equity and bond correlations are becoming more frequent

Notes: occurrences of positive correlations between the returns of equites and bonds in a calendar month. Equities represented by the MSCI world TR index, bonds by the ICE BofA Gov’t and Agency bond index

Source: Bloomberg, World Gold Council

Such a shift would place a considerable burden on the 60:40 portfolio.

As a thought experiment, we ran some analysis looking at portfolio performance (both actual and hypothetical) for two time periods: (A) 1973-1997, during which the stock:bond correlation was 42%, and (B) 1997-2021, with its -55% correlation. Table 1 shows the results, with the first column denoting the relevant periods/scenarios.

Period A saw higher portfolio returns accompanied by greater volatility and significantly larger maximum drawdown losses. The Sharpe ratio was similar in Period B, but that is because lower returns in this period were flattered by the negative correlations which restrained portfolio volatility.1 If we assign the same positive correlation experienced in period A to period B (Scenario C), the Sharpe ratio is reduced quite dramatically to .41 from .50.

Table 1. Actual and hypothetical equity and bond portfolio performance

A. The actual performance of MSCI world TR equities, US gov’t and Agency bond TR and a 60/40 combined portfolio between 1973 and 1997 – quarterly data

B. The actual performance of MSCI world TR equities, US gov’t and Agency bond TR and a 60/40 combined portfolio between 1997 and 2021 – quarterly data

C. The hypothetical return of a 60/40 portfolio between 1997 and 2021 assuming the correlation from the 1973 to 1997 period: 45.7%

D. The hypothetical return for a 60/40 going forward over 9 years (Years to maturity on bond index is c.9 years), assuming equity returns in line with A and Bond returns as per YTM of US Gov't and Agency bond Index

E. The hypothetical return for a 70/30 going forward over 9 years (Years to maturity on bond index is c.9 years) – weighting required to match Sharpe ratio from the last 25 years

Notes: Real returns from Dec 1973 to Dec 2021, deflated by US core CPI. Indices used are MSCI world TR index for equities and the ICE BofA Gov’t and Agency Total Return index for bonds. For scenarios, equity returns volatilities and bond volatilities from period A are used.

Source: Bloomberg, World Gold Council

Extending the thought experiment: what are the potential implications for asset allocation going forward if a positive correlation implies a significant drag on risk-adjusted portfolio performance from bonds? A 60:40 portfolio with lower expected bond returns only returns the Sharp ratio to .45 (Scenario D). In Scenario E, we see that a heftier allocation to equities is needed to bump up the Sharpe ratio to the higher levels seen in A and B. Our analysis suggests a split more like 70:30, with the added risk that a higher equity allocation would make the portfolio more vulnerable to stock market pullbacks.

Bonds will no doubt generate poorer returns going forward. They could also lose much of their diversification and risk-hedging capabilities if they increasingly, perhaps consistently, revert to a positive relationship with equities. And low yields may constrain their response to risk-off events, as investors may view cash as a viable hedging alternative.

Which is where gold enters the conversation. In previous research, we have thoroughly demonstrated the benefit of adding gold to a portfolio and its track-record of improving risk-adjusted returns, due to its uniquely effective role as a liquid diversifier and risk hedge.

In beefing up the equity allocation, the ‘standard’ portfolio would benefit from an allocation to gold given its asymmetric correlation to equities: close to zero when equities perform well, but significantly negative when they don’t. In our analysis, gold’s correlation to equities was largely unaffected by the regime shift in inflation before and after 1997 (scenarios A and B), and gold tends to perform well in a higher, or more volatile, inflation environment.

All of which suggests gold could play a pivotal role in delivering enhanced portfolio performance in the years ahead.

Footnotes

Sharpe ratio is a measure of the risk-adjusted return of a portfolio. A higher Sharpe ratio indicates higher portfolio returns relative to the level of risk in the portfolio (as measured by volatility).