Summary

- The domestic gold price ended 0.4% lower in January at Rs47,706/10g1

- Retail demand remained soft due to the reintroduction of COVID restrictions, a lack of auspicious wedding dates and a higher gold price in the second half of the month2

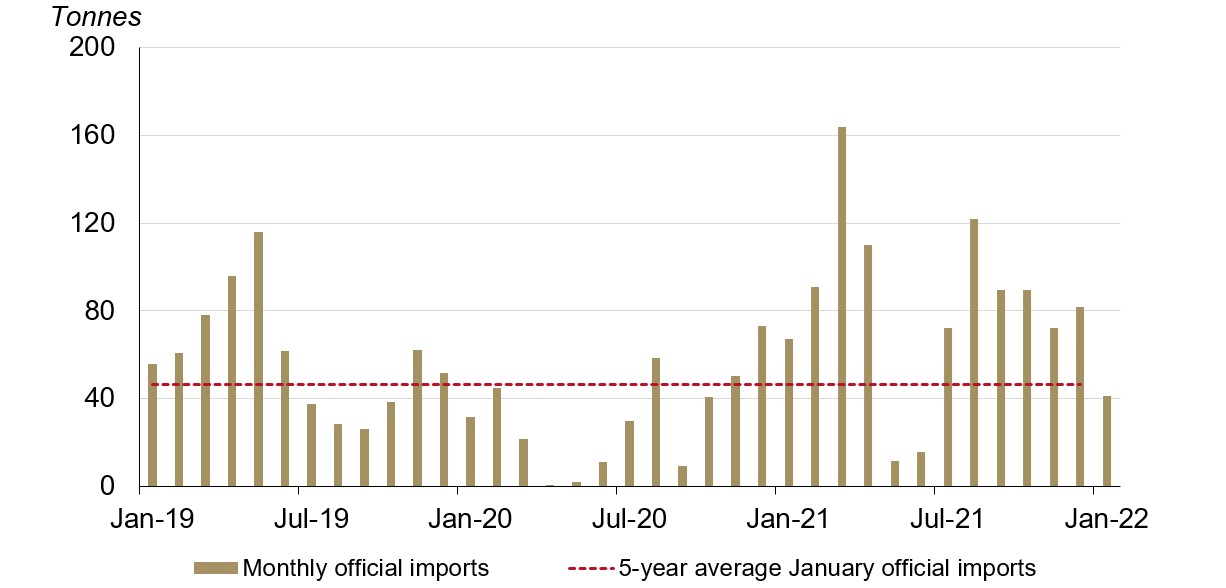

- Official imports declined 50% m-o-m due to soft retail demand, postponement of purchases awaiting the Union Budget on 1 February and anticipated tax changes – which did not materialise – and ample stocks

- Weak retail demand pushed the local market into a discount of US$1-2/oz during the first two weeks of the month, which widened to US$2-3/oz by month-end

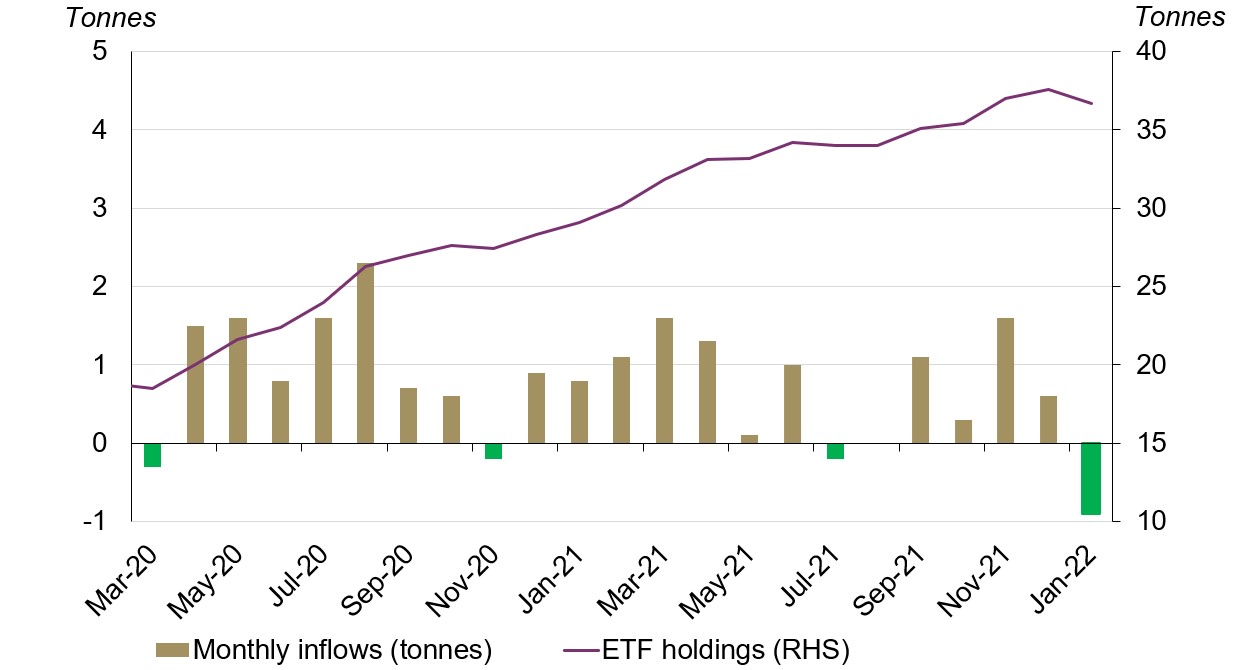

- Indian gold ETFs saw 0.9t of net outflows, primarily driven by rising 10-year Indian government bond yields and expectations of a more hawkish Fed stance. Holdings of gold ETFs totalled 36.7t3

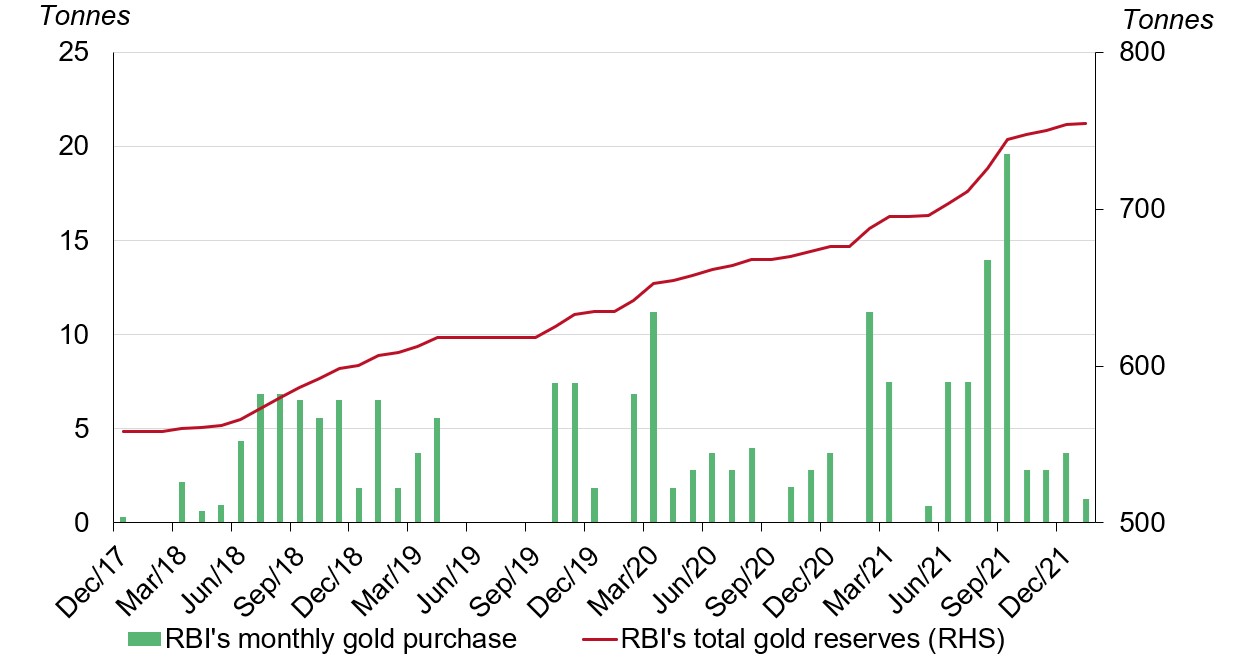

- The Reserve Bank of India (RBI) added 1.3t of gold in January, increasing its total gold reserves to 755.4t.

Looking ahead

- Retail demand in February is expected to improve on the back of falling COVID cases and the expectation of a stable gold price

- With no change to the tax rate on gold imports and the easing of restrictions, we anticipate that official imports should bounce back in February.

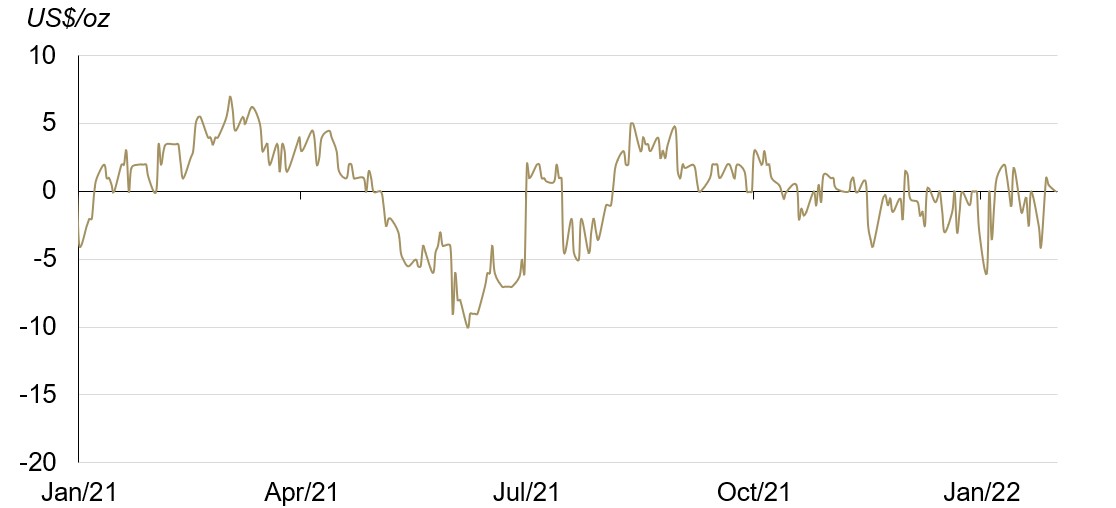

The local gold price traded mostly at discount during the month

The international gold price fell in January following a more hawkish than expected monetary stance by the FOMC, a strong dollar and rising bond yields. The LBMA Gold Price AM in USD and the MCX Gold Spot in rupees (INR) fell by 1.6% and 0.4% respectively over the month.4 The strong Indian local gold price performance was largely due to a weak INR, which depreciated by 0.9% over the month relative to the dollar.

Weak retail demand pushed the local market into a discount of US$1-2/oz during the first two weeks of January, and this widened to US$2-3/oz by month-end (Chart 1).5 A sideways local gold price during the last two weeks and expectations of tax changes for gold in the Union budget on 1 February (there was subsequently no change in the tax rate for gold) kept bullion offtake depressed.

With a moderation in the domestic gold price, an unchanged tax rate on gold, and an uptick in retail demand, bullion offtake gained momentum and the local market flipped back to an average premium of US$2-3/oz in the first week of February.

Chart 1: The local gold price traded mostly at discount during January

National Commodity & Derivatives Exchange Limited (NCDEX) polled premia/discount for domestic gold spot price vs landed gold price in India

Source: NCDEX, World Gold Council

Retail demand remained soft and imports declined

Retail demand remained soft in January due to the reintroduction of COVID restrictions and a lack of auspicious wedding dates. The higher gold price during most of the second half of the month created a further headwind for gold demand.6

Indian official gold imports totalled 41.2t in January, 39% lower y-o-y and 50% lower m-o-m. This was also ~12% lower than the five-year monthly average (Chart 2). Lower official imports in the month were driven by the following factors:

- soft retail demand amid restrictions imposed to curb the spread of the pandemic’s third wave

- postponed trade imports due to the anticipation of possible tax changes in the Union Budget on 1 February

- sufficient bullion stocks in the market.

Outlook for retail demand and official imports in February

Looking ahead to February, retail demand is expected to improve on the back of falling COVID cases and the expectation of a stable gold price.

With no change in the rate of tax on gold imports and the easing of restrictions, official imports are expected to bounce back.

Chart 2: Indian gold official imports were below five-year average

Indian monthly official imports from January 2019 - January 2022

Source: Metals Focus, IHS Markit, World Gold Council

Gold ETF holdings saw 0.9t of inflows during the month

Indian gold ETFs saw outflows of 0.9t (Rs5.7bn, US$76mn) in January, the first monthly outflows since July (0.2t). This was primarily driven by rising 10-year Indian government bond yields and expectations of a more hawkish Fed stance. Net January outflows took total gold holdings to 36.7t by the end of the month (Chart 3).

Chart 3: Indian gold ETF holdings saw 0.9t of outflows in January

Source: Bloomberg, Respective ETF providers, World Gold Council

The RBI added 1.3t to its gold reserves

The RBI’s gold purchases slowed to an eight month low of 1.3t in January, taking its gold reserves to 755.4t or 6.9% of total reserves (Chart 4).7 No purchases were made in the same month of 2021 or 2020, although 6.5t was purchased in January 2019. The RBI did not recommence its purchase of gold reserves until December 2017.8

Chart 4: RBI added 1.3t to its gold reserves in January

Source: IMF, RBI, World Gold Council

Based on the MCX Gold Spot price in INR as of 31 January 2021.

Kharmas is an inauspicious month in the Hindu calendar. Kharmas started on 16 December 2021 and ended on 14 January 2022. The month is considered inauspicious for weddings particularly in North and East India.

Indian 10-year government bond yield rose to 6.68% on 31 January 2022 from 6.45% on 31 December 2021.

We compare the LBMA Gold Price AM with the MCX Gold Spot price as their trading hours are closer to each other than the most commonly referenced LBMA Gold Price PM.

The premium/discount data is based on the gold premium polled spot price from National Commodity & Derivatives Exchange Ltd.

The Indian domestic gold price rose by 1.7% between 14 January and 25 January 2022.

Central bank data is taken from IMF-IFS: IFS up until November and weekly statistics from the RBI for December and January. January’s purchases are as of the week ending 28 January 2022. Please refer to our latest central bank statistics: https://www.gold.org/goldhub/data/monthly-central-bank-statistics.

RBI’s gold reserves were unchanged at 557.8t between November 2009 and November 2017.