Summary

- The domestic gold price ended 28% higher in 2020 at Rs50,005/10g

- The economic recovery momentum held up in December

- Retail gold demand was supported by a mix of jewellery and investment demand during the month

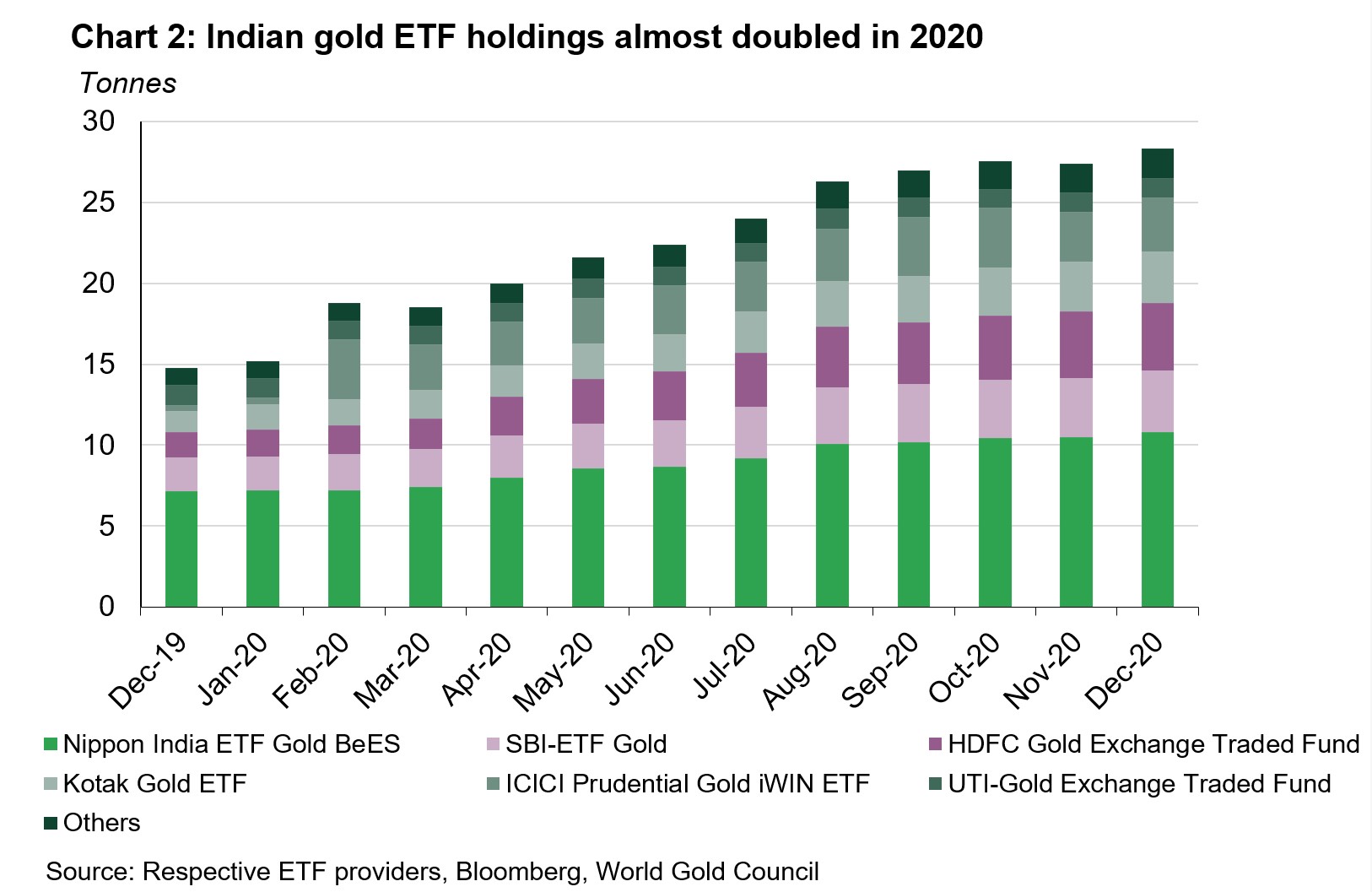

- The resurgence of a second wave of Covid-19 infections, as well as the emergence of the new strain of the virus and a higher gold price, led to ETF inflows in December. Total holdings for Indian gold ETFs reached 28.3t at the end of 2020; a net inflow of 1t in December and 13.5t in 2020

- The Reserve Bank of India (RBI) added 3.7t of gold in December and 41.6t in 2020

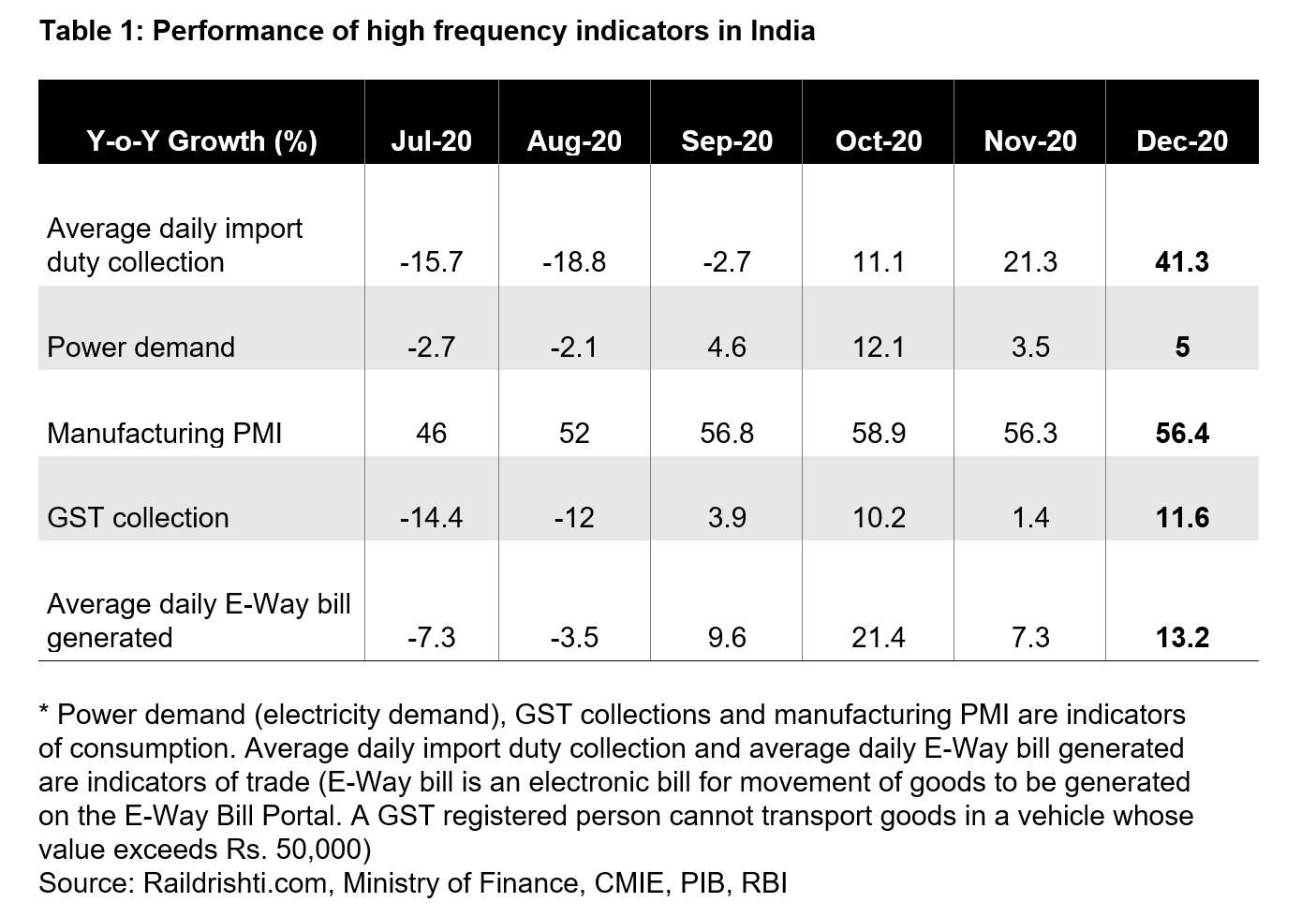

Economic recovery momentum held up in December

After making a strong recovery since COVID restrictions were eased in September, the pace began to moderate in November. High frequency indicators for December, however, signalled continued momentum in this economic recovery (Table 1).

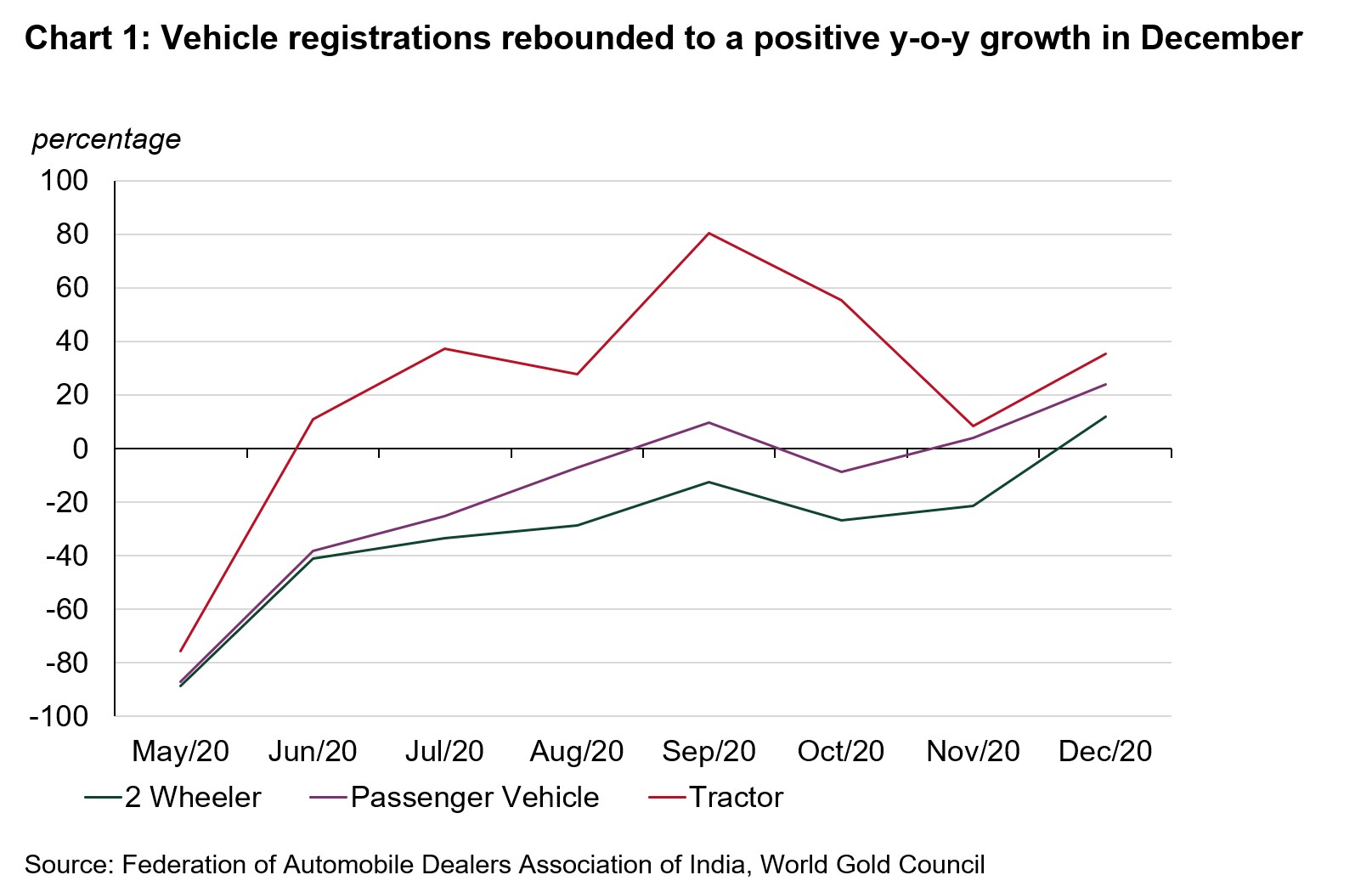

Vehicle registrations among various categories rebounded to a positive y-o-y growth in the month after some moderation in November (Chart 1). This shows momentum in the economic recovery holding up in December.

Foreign Institutional Investor (FII) inflows into Indian equities remained strong throughout 2020. Several factors fuelled these inflows, such as rising hopes of a strong economic recovery in the coming years, a significant decline in COVID-19 cases in India from the highs in September, the weak dollar index and the announcement of vaccines. In December, FIIs bought equities worth Rs620.2bn (US$8.4bn) – the highest net inflows into Indian equities on record. Net FII inflows in 2020 stood at US$23bn against US$14.4 in 2019. With strong inflows into the stock market and a gradual revival in economic activity, the BSE SENSEX gained 8.1% during the month.

A mix of both jewellery and investment demand supported retail demand in December

December was a month of two halves for retail demand in India. In the first two weeks jewellery demand was supported by wedding purchases and helped by the stable gold price, which averaged ~Rs49,500/10gm through the month. With the onset of Kharmas, jewellery demand tapered off.1 But this weakness was offset by investment demand. The stability of December’s gold price – averaging ~Rs49,500/10gm from a high of Rs52,280/10gm in early November – supported investment demand. The lower price level was seen as a buying opportunity and, with higher gold prices anticipated over the long term, investment demand was strong in the last two weeks of the month.

Gold ETFs attracted inflows in December

A second wave of COVID-19 infections and the emergence of a new strain of the virus fuelled pessimism around the economic recovery, supporting gold prices. This, in turn, supported inflows into gold ETFs, with a net inflow of 1t in December. Through 2020, interest in Indian gold ETFs has picked up significantly. The rising gold price, increased equity market volatility, and economic uncertainty due to COVID-19 has fuelled safe-haven demand for these products. The return on gold (+28%) vastly outperformed the BSE Sensex (+17.2%) and the 10-year government bond (+11.9%), supporting gold’s appeal as an asset class.2 As a result, inflows into Indian gold ETFs almost doubled in the year, taking total holdings to 28.3t by the end of 2020, compared to 14.8t at the end of 2019 (Chart 2).

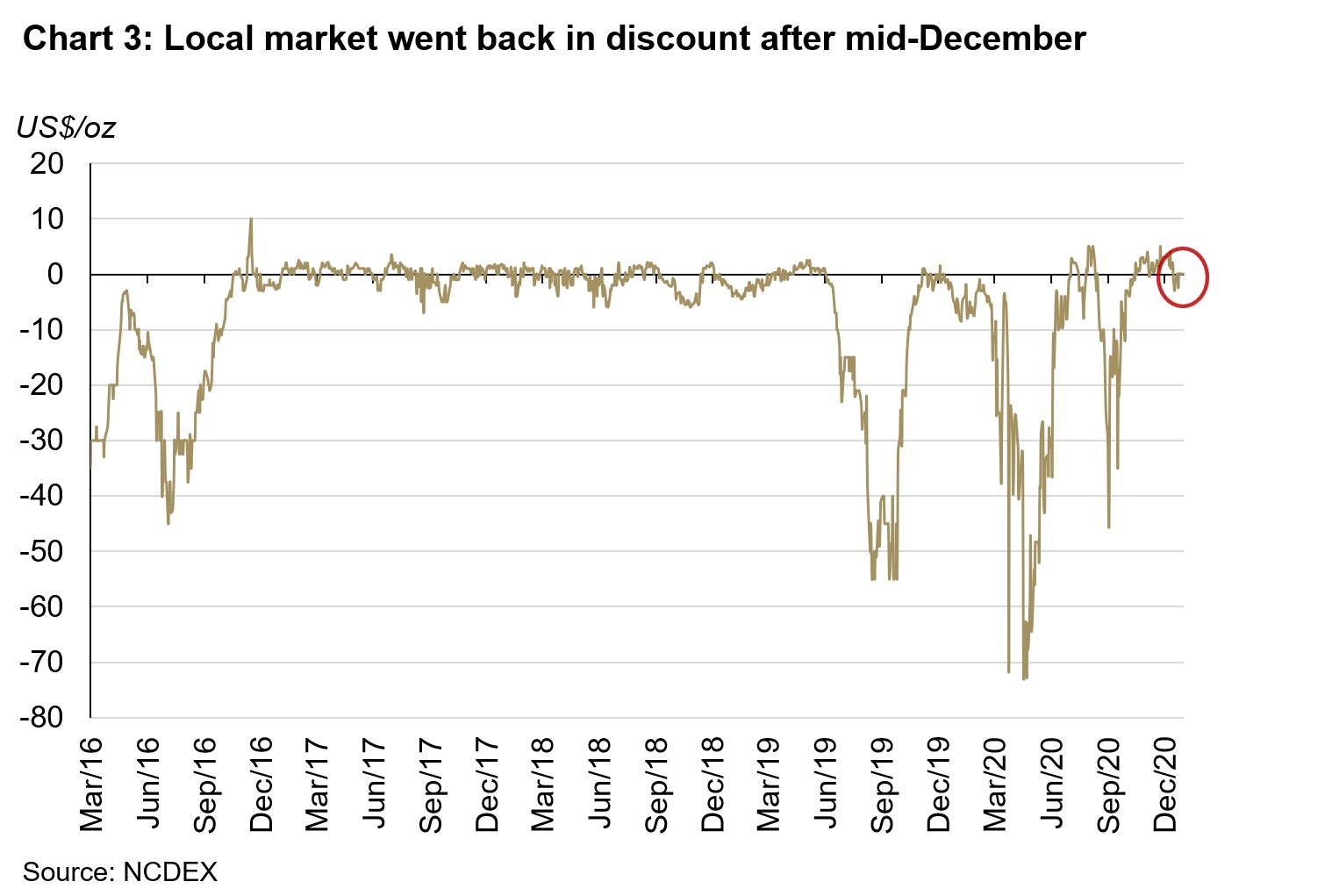

Local market back in discount from mid-December

With jewellery demand tapering off at the start of Kharmas, the local gold price was back in discount for the last two weeks of December. The average discount remained at ~ US$1/oz during the last two weeks of the month (Chart 3).

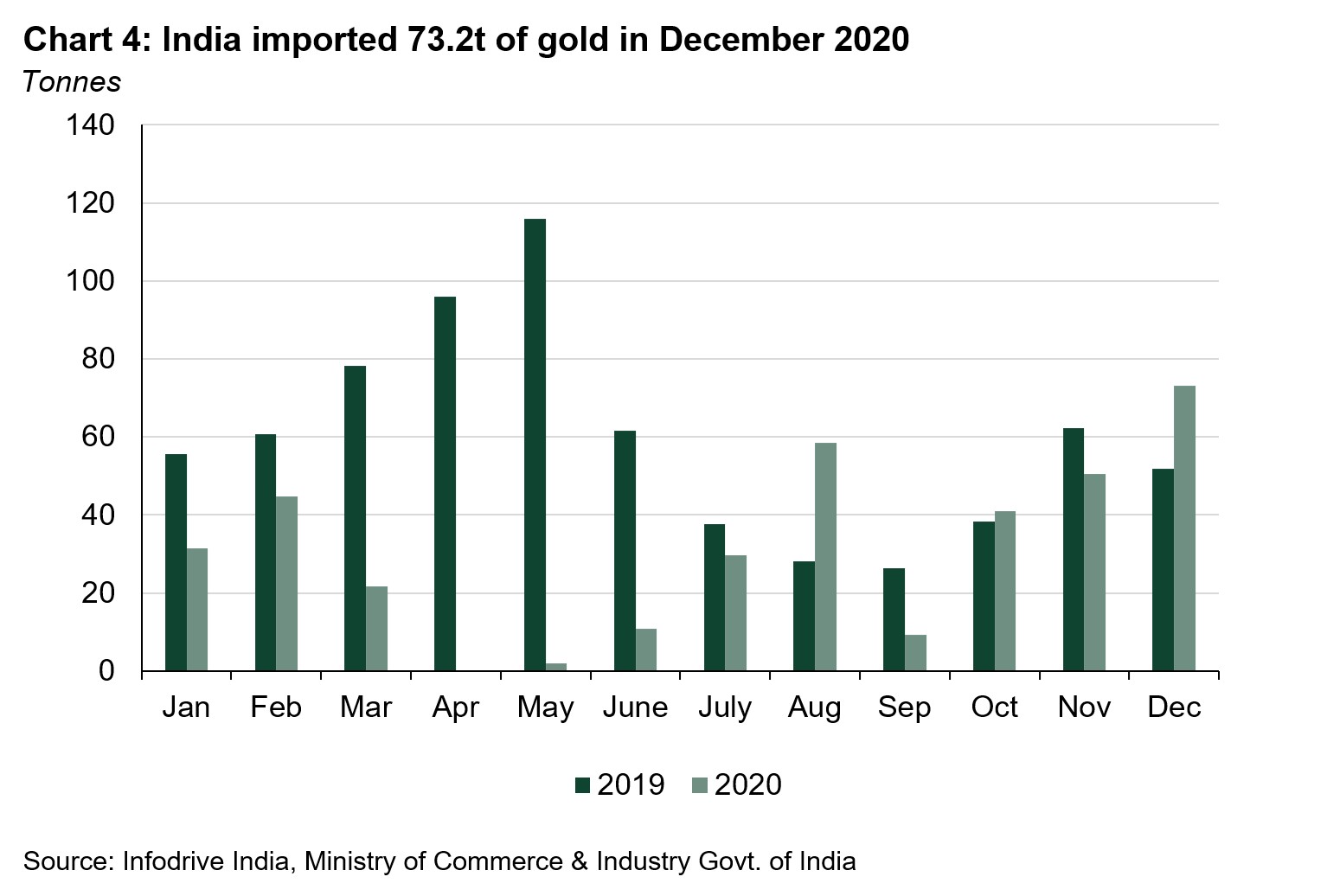

India imported 73.2t of gold in December

Indian official gold imports recovered to 73.2t in December – 45% higher m-o-m and 41% higher y-o-y. On a full year basis though, gold imports remained very weak – 48% lower than 2019 (Chart 4). A total of eleven banks, nominated agencies and exporters imported 54.8t of bullion during the month, and 18 refineries imported 18.4t of gold doré (fine gold content).

Further, of the total of 73.2t official imports, 28.3t were imported via Sri City Free Trade Warehousing Zone (FTWZ).3 Seven overseas banks accounted for these imports with JP Morgan, ANZ and Standard Chartered accounting for 83% of these imports. These imports landed in FTWZ with the delay caused due to automated custom assessment in the clearance of imports and demand created by the wedding season.

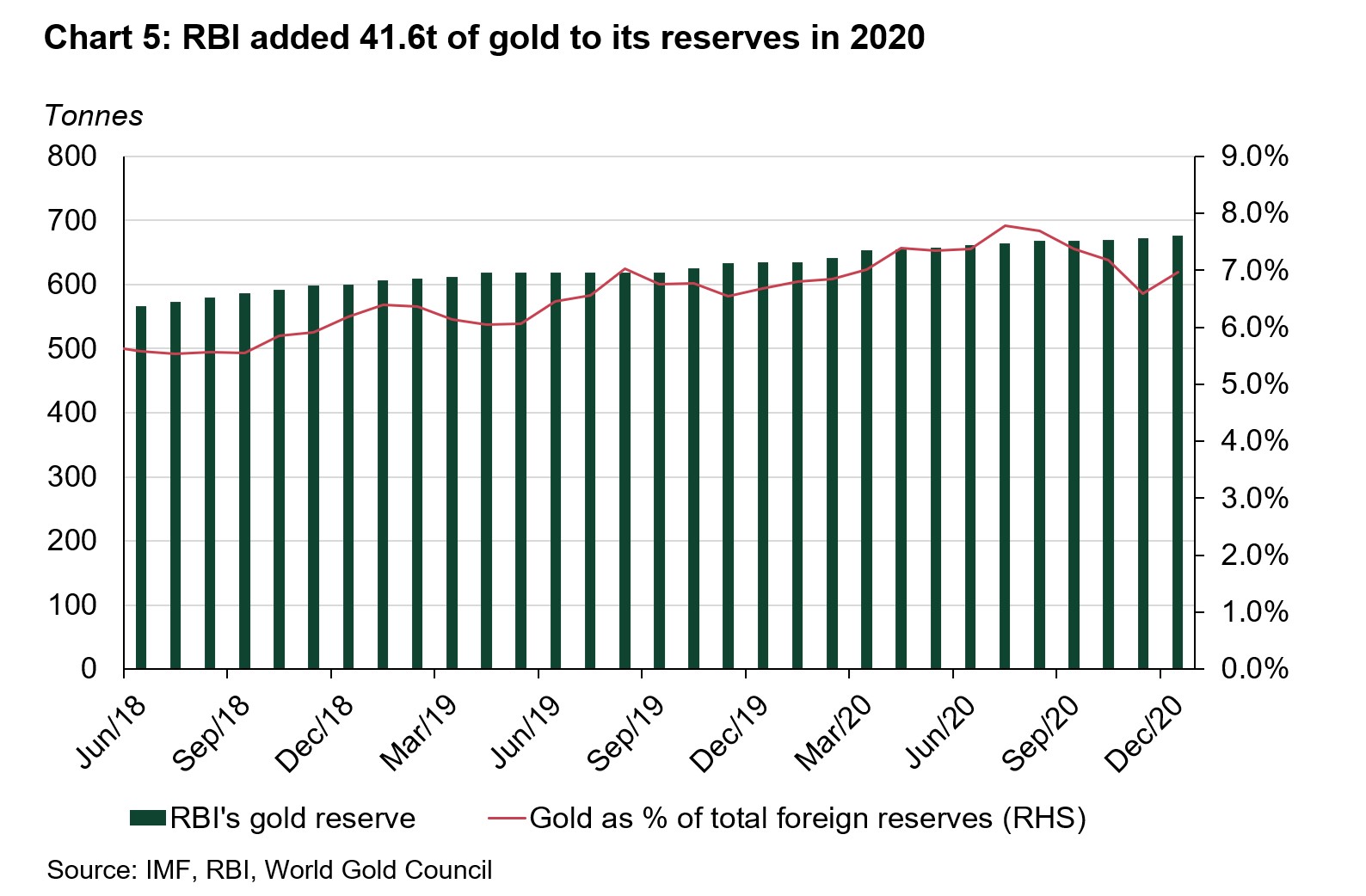

RBI added 41.6t of gold reserves in 2020

The RBI purchased an additional 3.7t in December, bringing y-t-d purchases to 41.6t and taking its gold reserves to 676.6t, or 7% of total reserves (Chart 5).4 The RBI has stepped up its gold purchases with the aim of diversifying its foreign reserves and maintaining the safety and liquidity of its forex reserves.

Footnotes

1 Kharmas is a one-month period from 15 December to 14 January. This period is considered inauspicious for buying any new property, starting a new venture, or for weddings.

2 As of 31 December 2020. Computations in Indian Rupee of total return indices for BSE Sensex and S&P BSE India Government Bond index. For domestic gold price MCX India Gold Spot Index is considered.

3 FTWZ offers a distinct advantage as overseas suppliers can import gold into the custom-bonded warehouse of FTWZ without paying customs duty for authorised operations. Imported gold can be stored in FTWZ for a long period – as long as the letter of approval (LOA) is valid – thus reducing the logistics time in supplying to the domestic market as compared to importing from the overseas market.

4 Central Bank data is taken from IMF-IFS, IFS up until November and weekly statistics from RBI for December. Please refer to our latest Central Bank Statistics https://www.gold.org/goldhub/data/monthly-central-bank-statistics