This week, LGIM announced that it would be reopening its UK commercial property fund in October.1 Investors in UK commercial property funds – those available to retail investors have close to £13bn in AUM – have seen their investment stuck, or “gated” since March. And, so far at least, most UK property remain closed to investor withdrawals, highlighting the liquidity risk that comes with investments such as these. Questions have also been raised on whether such illiquid funds should be marketed to retail investors at all.

Material uncertainty

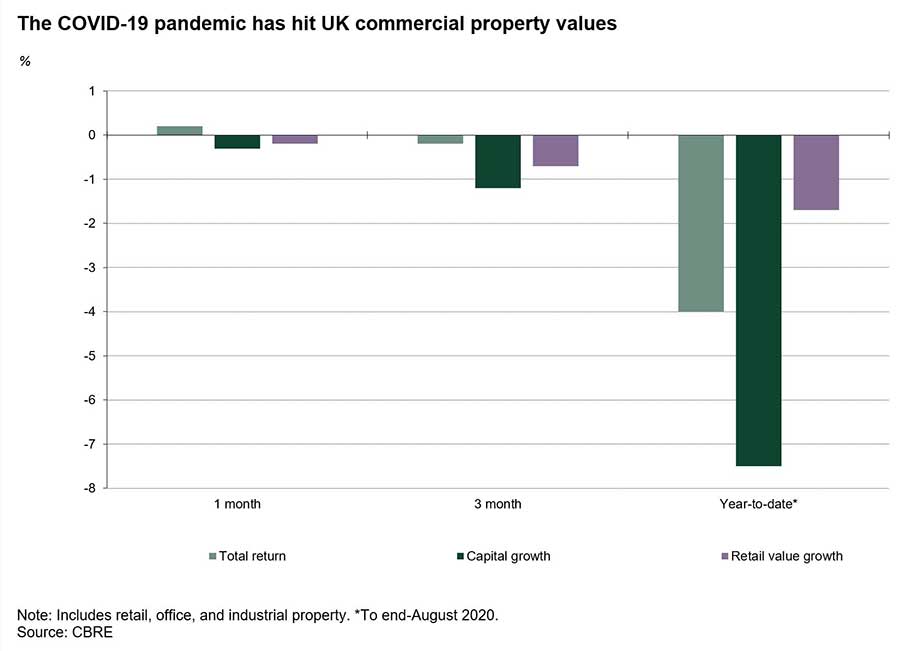

After the upheaval caused by the COVID-19 pandemic, uncertainty has become the norm for investors and fund managers. As the UK property market – both residential, commercial – came to a standstill earlier this year, the absence of activity led to challenges in valuing property investments with the certainty required. As a result, property funds suspended withdrawals by investors. And until more normal levels of property market activity are seen, investors may continue to struggle to access their capital.

There is also uncertainty on the future of the commercial property market, even after the pandemic has passed. Working from home has become established practice over the last six months, leading to questions around the long-run role of offices. In August, Schroders announced that working from home and flexible working for its employees would become permanent.2 Decisions such as this will likely have significant implications on the value of property investments going forward.

Illiquidity risk

This highlights the illiquidity inherent in some investments. Commercial property funds have been a mainstay in many investment portfolios over the last 25 years, providing a steady income distribution stream and capital appreciation. However, during times of severe economic stress, demand for commercial property is negatively affected. As increasing numbers of investors try to withdraw their holdings, it is often difficult to sell the underlying assets to meet demand thus leading to property fund managers "gating" the fund. In the meantime, the asset values of the fund may fall further without the individual investor being able to liquidate their position.

An opportunity for gold?

We feel this could present an opportunity for gold. As we highlight in our strategic case for gold, there are three key attributes which could help investors who have an exposure to for illiquid investments:

- Return: gold has been shown to generate returns in both good times and bad. So, in times of economic expansion, gold will positively add to portfolio performance. But, crucially, in times of economic contraction, gold will act as a ballast and protect wealth.

- Correlation: real estate investments may be more positively correlated with other portfolio assets – such as equities. During the global financial crisis in 2008-2009, alternative assets such as real estate – often considered diversifiers – fell along with other assets, whereas gold did not.

- Liquidity: the gold market is large and highly liquid. We estimate that physical gold holdings by investors and central banks are worth approximately £2.7 trillion, with an additional £700 billion in financial market instruments such as derivatives. In stark contrast to many financial markets, gold’s liquidity does not dry up, even at times of acute financial stress.

Gold’s traditional role as a safe-haven asset means it comes into its own during times of high risk. In these instances, when liquidity may fall for other investments, gold can act as a genuine diversifier over the long term.