Gold plays many roles within an investor’s portfolio. It serves as a portfolio diversifier: it tends to have low correlations to most assets usually held by institutional and individual investors. It preserves wealth: gold is typically considered a hedge against inflation, but it also acts as a currency hedge, in particular against the US dollar and other developed-market currencies with which gold correlates negatively. Particularly important to investors, gold also helps to manage risks more effectively by protecting against tail-risk events1 – namely, unpredictable events sometimes considered unlikely which cause considerable damage to investors’ capital. Notably, these events are likely not only to continue but also to increase their frequency as interconnected global economies raise the possibility of spill-over effects to other markets.

The advantages of gold’s role in portfolio risk management have, over the past decade, become better understood in Western markets. In Japan, the role of gold in a portfolio context has only recently gained recognition, yet has advanced substantially in the past 18 months. This is influenced by such developments as the continued weakness of the Japanese economy, deteriorating government finances, unfavourable public and corporate pension reforms, growing concern over event/tail risk, change of needs in pension management resulting from demographic shifts, adoption of international financial-reporting standards (IFRSs), and volatile performance of traditional assets. All these factors call for a stronger focus on wealth preservation and performance stability in pension fund management. Gold is increasingly considered by Japanese institutional investors as a solution that meets today’s needs.

The country has experienced a prolonged weak economy, described by many as the “lost 20 years of Japan”. Deflationary pressures, declining disposable income, reduced savings rates, and a dim corporate earnings outlook have prevailed. The government has not yet been able to turn the economy around. The national debt is now more than 200% of GDP, the worst among OECD countries.2 The fast-ageing population has put further structural strains on the country’s fiscal condition, forcing the government to cut back benefits owed under the universal public pension programme. Facing an uncertain operating environment, corporate pension sponsors have also reduced plan benefits, a significant move in a country known for its protective employment culture.

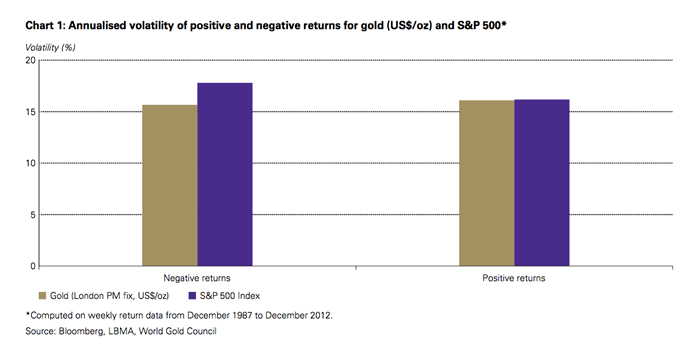

As in other markets, we believe gold’s role in Japan extends beyond affording protection in extreme circumstances. In previous studies, the World Gold Council has shown that including gold in a portfolio can reduce the volatility of a portfolio without necessarily sacrificing expected returns. However, a more detailed analysis on the effect gold allocations have during tail-risk events shows that portfolios including gold not only deliver better risk-adjusted returns, but that they can also help to reduce extreme losses.

This article discusses the benefits of including gold as a tail-risk hedge from an international perspective and compiles research findings from previous studies.3 We show that even modest allocations to gold between 2% and 10%– depending on the assets held by investors and their risk tolerance – can have a positive effect on portfolios. In particular, gold tends to reduce not only portfolio volatility but also losses that may be incurred during tail-risk events. Looking back at events including Black Monday, the LTCM crisis, and the recent global financial crisis of 2008 – 2009, our analysis shows that gold mitigated portfolio losses incurred by investors during almost all tail events under consideration. For example, investors in the US, Europe, and the UK who held a 5% allocation to gold, reduced losses by approximately 5% during eight tail risk events. Similarly, Japanese investors would have saved between 2.3% and 3.6% during nine tail-risk events by adding a 5% allocation to gold in a typical portfolio of foreign and domestic stocks and bonds.

Topics covered include:

- The case for gold in portfolio risk management

- How does gold act as a hedge against tail risks?

- Optimal allocations to gold

- The role of gold in reducing extreme losses for Western investors

- The role of gold for reducing extreme losses for

Japanese investors

- The role of gold during possible future tail risk events

- A sharp rise in Japanese government bond yields

- A Japanese-market selloff

- A global shock impacting primarily developed markets

- The role of gold during possible future tail risk events

- Portfolio impact stemming from potential tail-risk events