Cryptocurrencies may become an established part of the financial system. But, in our view, gold is very different from cryptocurrencies, as gold:

- is less volatile

- has a more liquid market

- trades in an established regulatory framework

- has a well understood role in an investment portfolio

- has little overlap with cryptocurrencies on many sources of demand and supply.

These characteristics underpin gold’s role as a mainstream financial asset that will likely continue to resonate in today’s digital world.

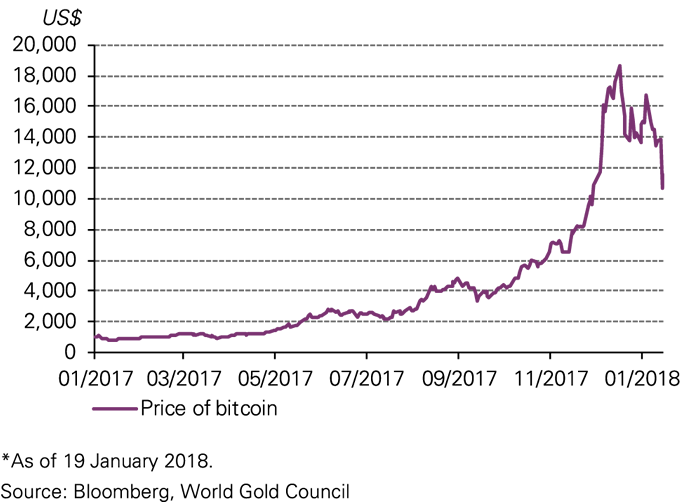

Chart 1: Bitcoin’s price saw a parabolic rise in 2017*

Cryptocurrencies and gold – competitors or complements?

Despite anecdotal comments from some well-regarded financial commentators that gold prices and demand are suffering from the rally in cryptocurrencies, there isn’t any quantifiable evidence to support this. The weakness in physical demand in 2017 – for example, the paltry sales of US Eagles – is largely explained by the steady march higher of the S&P 500. Other established gold markets – such as China – saw healthy levels of demand. Overall, the level of the gold price in 2017 appears to be consistent with drivers of the past few years and is showing no signs of suffering from crypto-competition.

Another factor to consider is competition within cryptocurrencies themselves. There are currently over 1,400 cryptocurrencies available and, while bitcoin is the largest by far, new technology could have devastating effects on the value and supply of any of the cryptocurrencies, including bitcoin.

Blockchain technology, the distributed ledger mechanism that underpins cryptocurrencies such as bitcoin, is genuinely innovative and could have wide-ranging applications across financial services and beyond. In the gold market, various players are exploring blockchain in the context of transforming gold into a ‘digital asset’, tracking gold provenance across the supply chain, and introducing efficiencies into post-trade settlement processes. Such applications are typically built on private blockchains operated by trusted parties rather than using bitcoin or other ‘public blockchains’.

Chart 2: Bitcoin’s price volatility is very high

Gold and Bitcoin supply

At a high level, there are some similarities between the supply profile of gold and cryptocurrencies. The stock of bitcoins, for example, increases in number at a rate of approximately 4% per annum, and is engineered to slowly decline to zero growth around the year 2140. While gold can be mined without a date limit, its production rate has been quite small and steady. Approximately 3,200 tonnes of gold have been mined on average, each year, adding about 1.7% to the total stock of gold ever mined. Bitcoin’s future diminishing growth rate and ultimate finite quantity are clearly attractive attributes, as is gold’s scarcity and marginal annual growth