We’re delighted to contribute another thought-leader article published in Financial Investigator’s highly regarded magazine. In their September issue, we review the notion that whilst bonds may be en vogue, gold never goes out of style. The article supports our ongoing belief that gold has a key role to play as a strategic long-term investment and mainstay allocation within a well-diversified portfolio.

Summary

- Amid economic uncertainty, European investors have been, so far this year, reallocating to fixed income assets

- While fixed income assets may seem attractive currently, persistent inflationary pressures can bring risks to both the growth outlook and bond returns

- Gold should be considered as a long-term strategic asset alongside bonds as it provides excellent returns in a wide range of economic conditions

Macroeconomic outlook

Reassured by the resilience in macro data, and frustrated that inflation isn’t falling fast enough, major central banks have continued with the monetary tightening exercise, in some cases coming back to it after a brief pause. And as the lagging impact of their aggressive rate hikes ripples through the economy, the broad trend remains for slowing growth in the back half of the year.

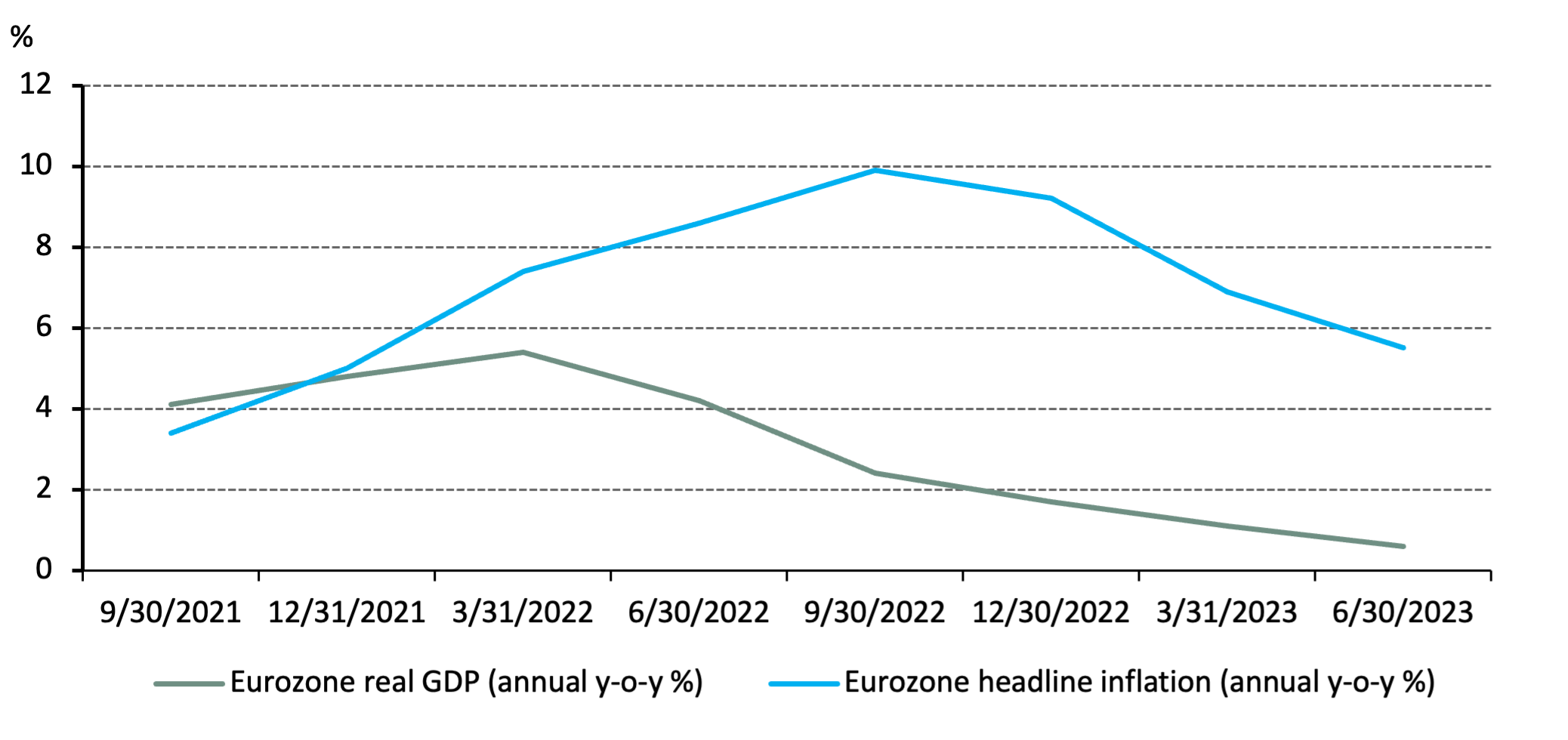

In the eurozone, the European Central Bank (ECB) has lifted interest rates by 4.5% since July last year, back to the highest ever level of 4%, to tame inflation. And while headline inflation is now well off October’s 10.6% year-on-year (y-o-y) peak, dropping to 5.2% y-o-y in August, there is no denying that the pace of growth is decelerating (Chart 1). Indeed, the cost-of-living pressures and the rise in interest rates are weighing on domestic demand.

Chart 1: inflation is cooling, but still above target, and growth is slowing

With the balance of economic forces tilted against capital markets, investors have been reallocating into safer assets recently. According to Refinitiv’s European Fund Flow Report, fixed income funds saw the largest inflows (€18bn) in June while equity and multi-asset funds faced outflows. The flow pattern for June has cemented the year-to-date trend; i.e. fixed income funds were the asset type with the highest estimated net inflows overall for 2023 so far.

Bonds are attractive, gold looks good as a complementary asset

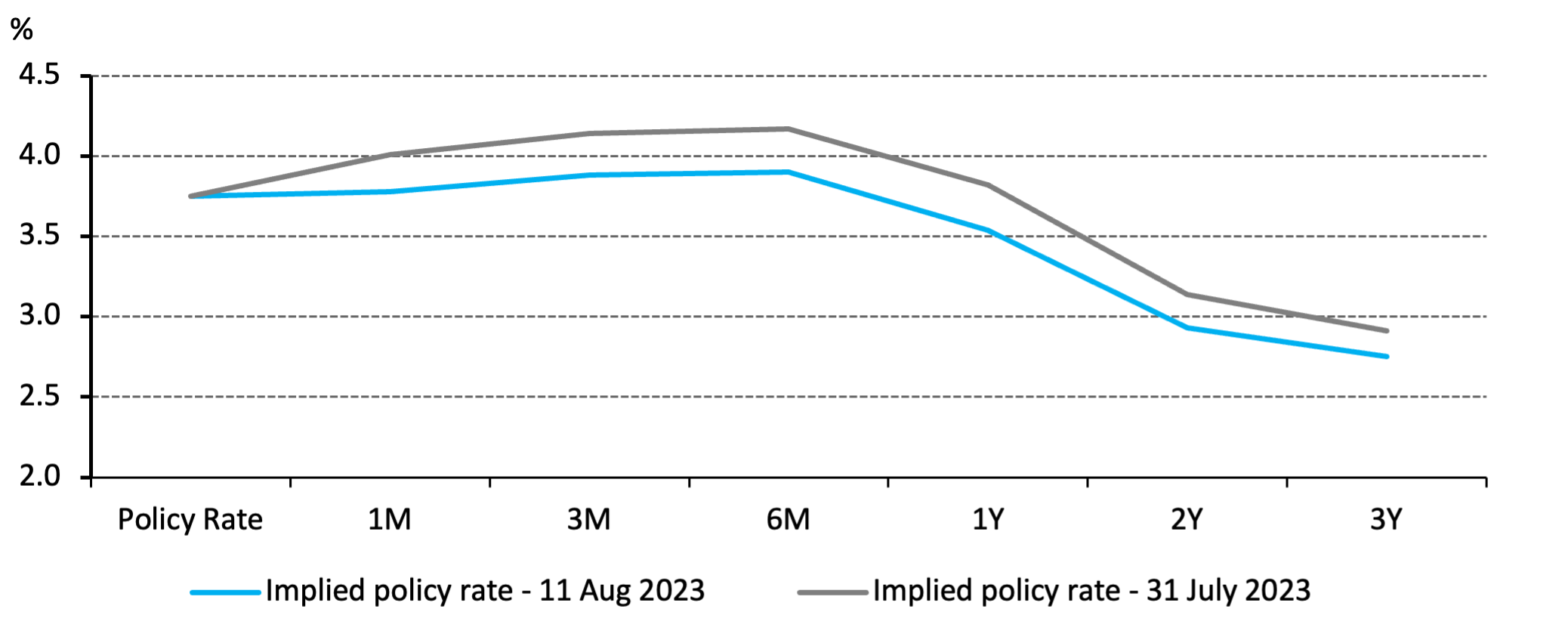

Fixed income assets do seem like an attractive choice for investors currently. The sharp rise in bond yields since early 2022 and the possibility of rates peaking soon (Chart 2) have improved the return potential in many fixed income sectors. And while inverted yield curves make it less compelling to extend duration, a modest increase in duration could be prudent for investors seeking to hedge against a growth shock.

Chart 2: Investors are expecting lower rates compared to previous projections

Eurozone implied future cash rates*

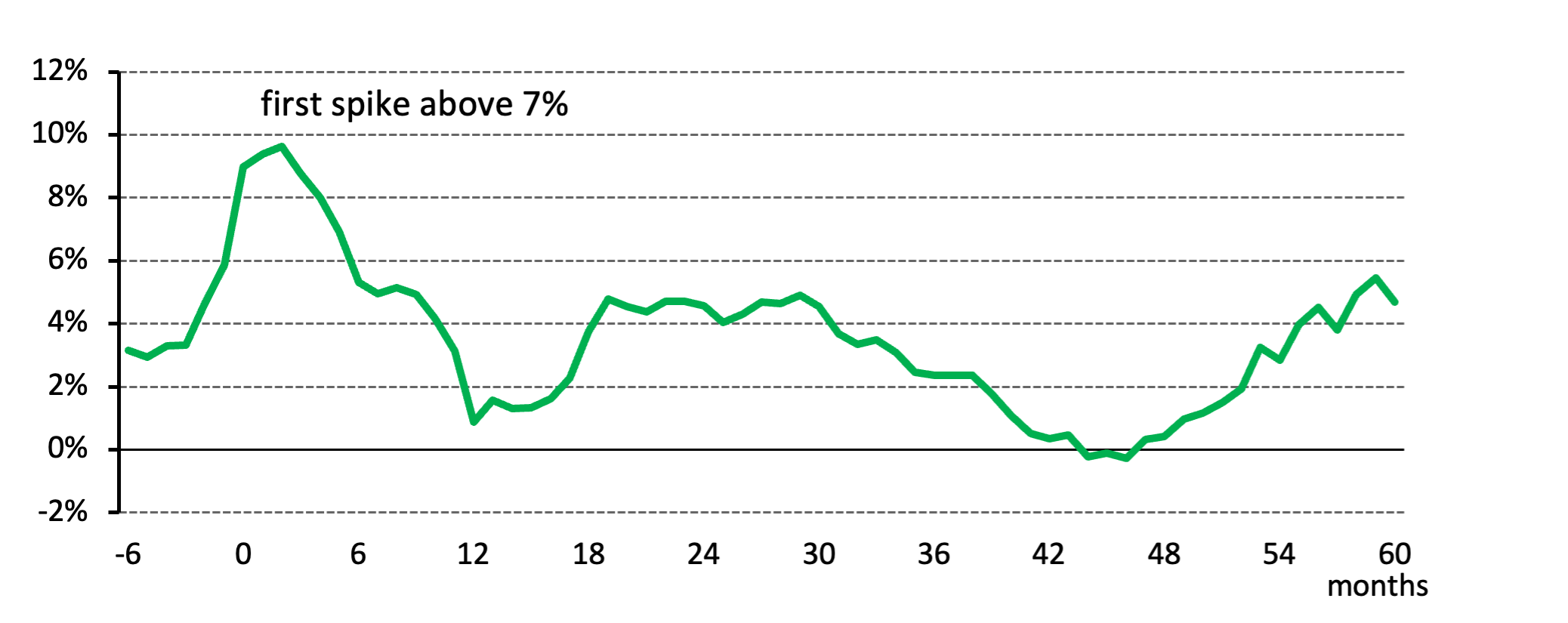

But there are risks associated with this view. Persistent inflationary pressures remain the primary obstacle to monetary easing and could result in further tightening. Moreover, inflation volatility may be part of the medium-term inflation story. In fact, looking at the US experience where we have data going back to 1870, inflation has tended to see echo waves two and five years after its first spike above 7% (Chart 3).

Chart 3: Inflation cycle in the US since the 1870’s

US inflation experienced, on average, multiple bounces after the first spike above 7%*

And the combination of high wage growth, the green transition, deglobalisation and geopolitical uncertainties speaks to an environment of more frequent potential shocks to inflation. Such an environment would require ongoing and fairly dramatic adjustments to monetary policy from the ECB, introducing volatility, potentially below trend growth and the possibility of negative returns in euro fixed income allocations.

Against this backdrop, there are several advantages to diversifying the sources of safety in an investment portfolio beyond just high-quality government bonds. Indeed, gold is a global asset and its diverse sources of demand give it resilience and the potential to deliver solid returns in various market conditions. For instance, following a strong 2022 (+6% in EUR), in which gold outperformed both global equities and eurozone government bonds, the precious metal has delivered another gain of 4.4% during the first seven months of 2023, once again outperforming eurozone government bonds.

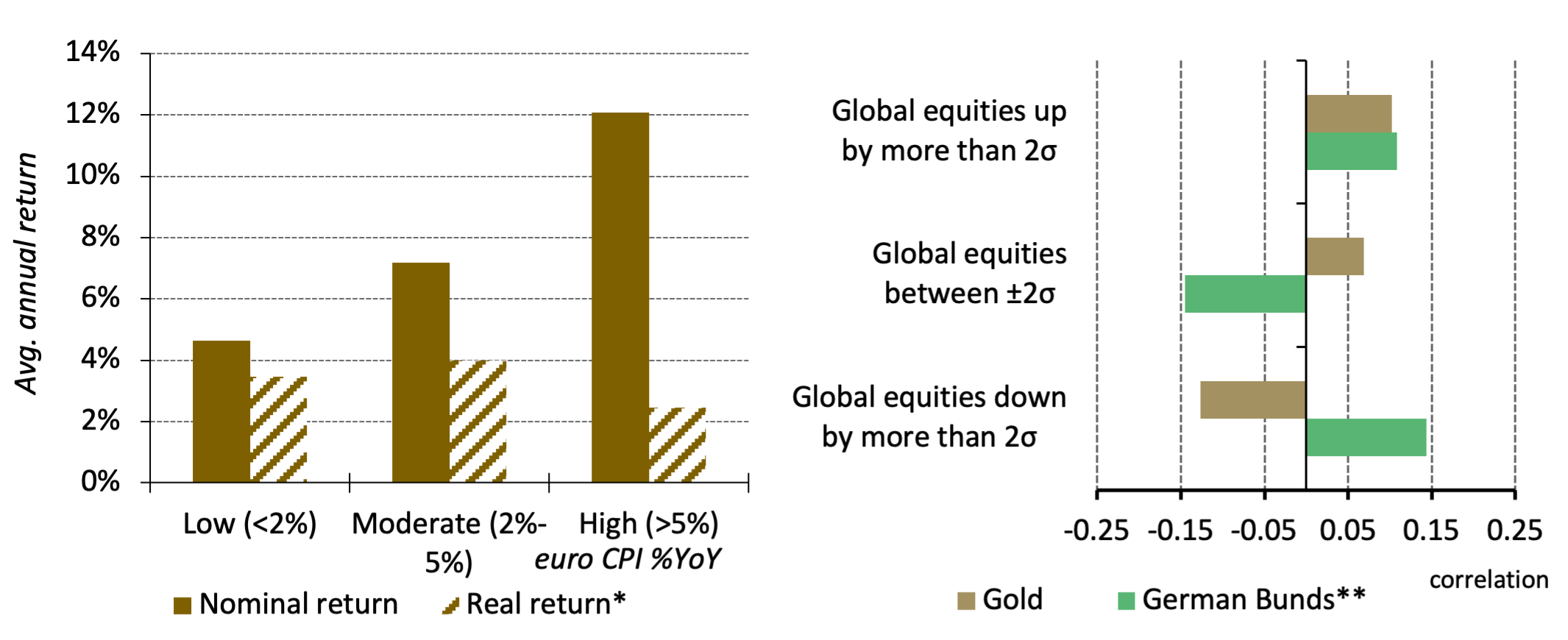

Furthermore, Chart 4 highlights that gold can not only be particularly effective in times of high inflation, it can also help during challenging equity markets. While effective diversifiers are sometimes hard to find, with many assets becoming increasingly correlated as market uncertainty rises, gold is different in that its negative correlation to equities and other risk assets, as seen in Chart 4, increases as these assets sell off.

Chart 4: Gold can be an effective addition to a portfolio

a. Gold historically performs well in periods of high inflation

b. Correlation of global equities vs gold and German Bunds in various market environments

These combined characteristics underscore why we believe gold has a key role as a strategic long-term investment and as a mainstay allocation in a well-diversified portfolio, alongside equities and bonds. Going forward, it is likely that gold and government bonds will perform differently from one another. This feature alone should appeal to investors tasked with managing the potential risks ahead.

More on market perspectives: Gold Mid-year outlook 2023: Between a soft and a hard place