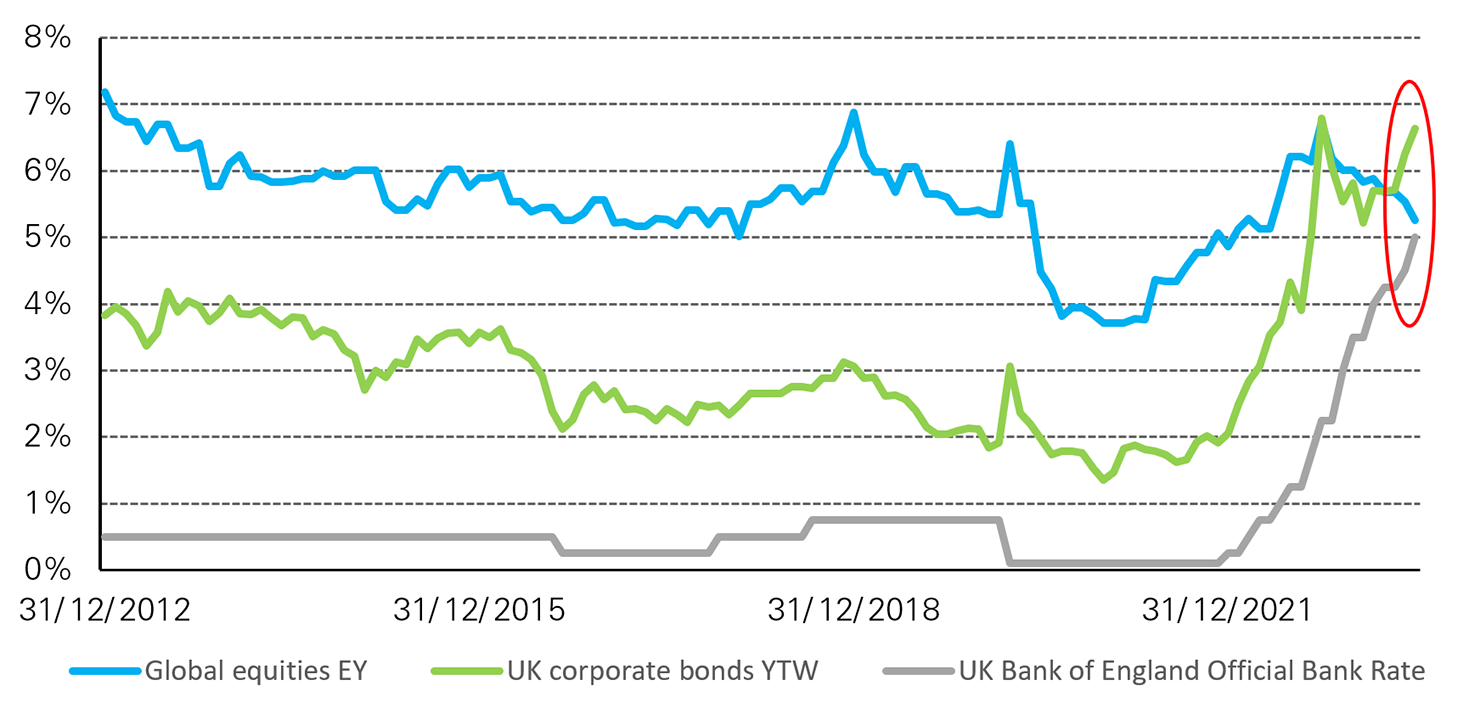

A lot has been made of the convergence of yields for cash, bonds and equities (on an earnings yield basis), with the higher yield on offer in the cash space leading many investors to reassess their portfolio exposures (Chart 1).

A lot has been made of the convergence of yields for cash, bonds and equities (on an earnings yield basis), with the higher yield on offer in the cash space leading many investors to reassess their portfolio exposures (Chart 1).

Source: Bloomberg, World Gold Council. Global equities is MSCI World Index, UK corporate is Bloomberg Sterling Aggregate Corporate Index, and cash is UK Bank of England (BoE) Official Bank rate.

*Data from 31 December 2012 to 30 June 2023.

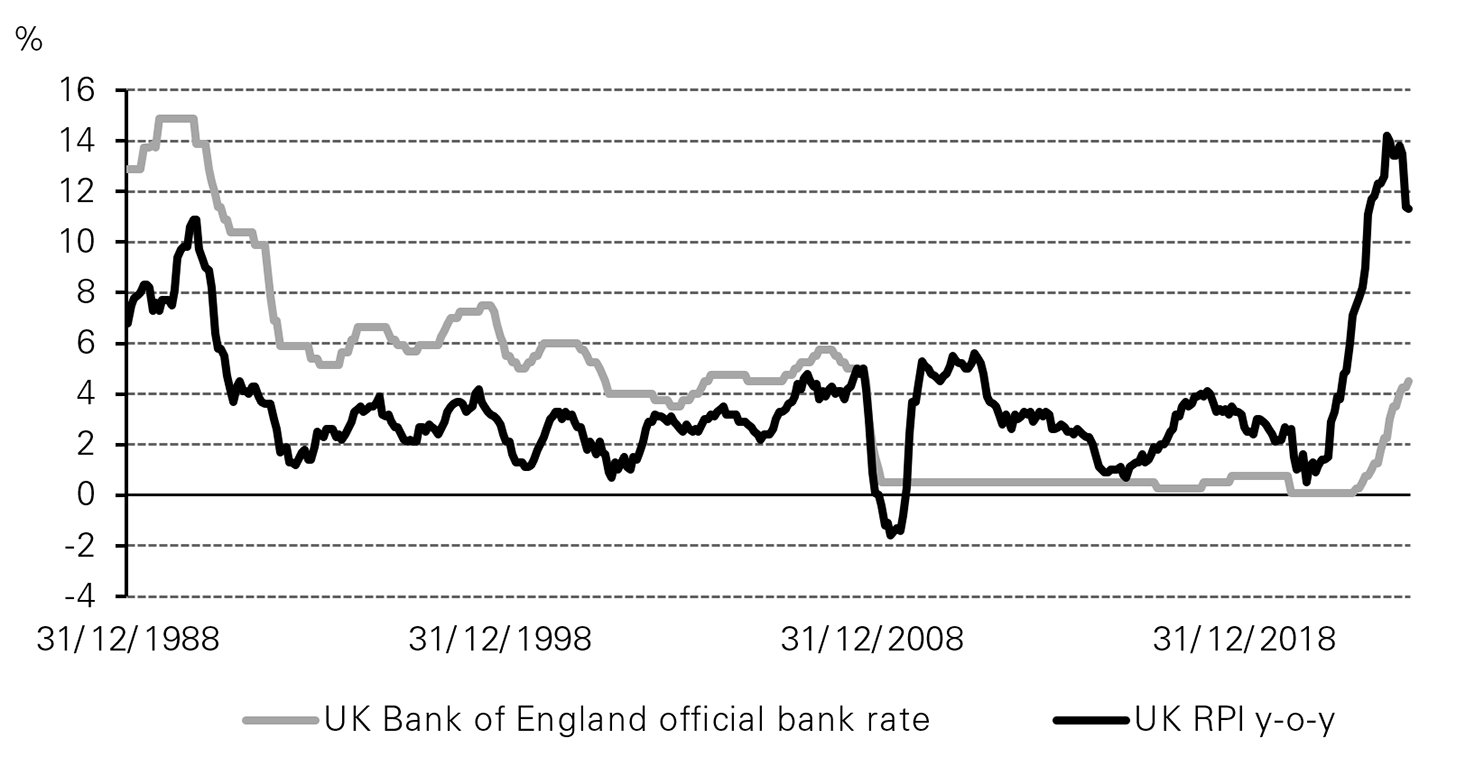

In fact, with cash yields offering compelling reward with little risk and with the balance of economic forces still appearing to be tilted against global capital markets, investors have been rushing into cash over recent months. And after years of unattractive yields, it is of course a welcome change to get some interest on defensive positions. That, however, is different to saying that holding cash today – on a long-term basis – is a no-brainer. Why? Cash yields still aren’t positive in real terms (Chart 2). In the late ’80s, ’90s and pre-Global Financial Crisis, high cash rates were associated with growing spending power. Today it’s not the case.

Source: Bloomberg, World Gold Council

*Data from 31 December 1988 to 30 June 2023.

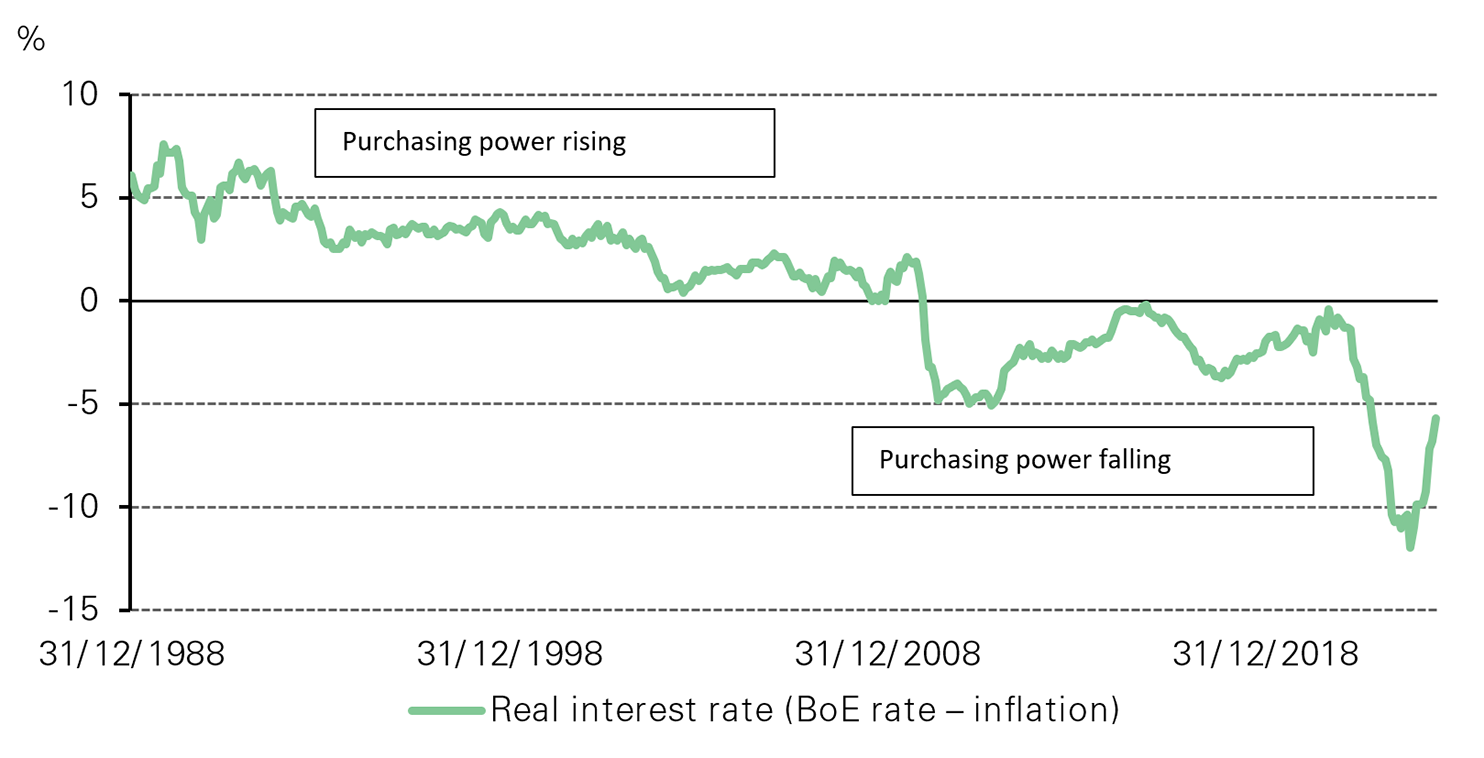

Considering the above, rushing back to cash today – other than for tactical reasons – is not the obviously good idea it might at first appear to be. There is no certainty its purchasing power will actually hold up. So the key question of where to make long-term investments that can deliver positive real returns remains as relevant as ever, given the inflation outlook.

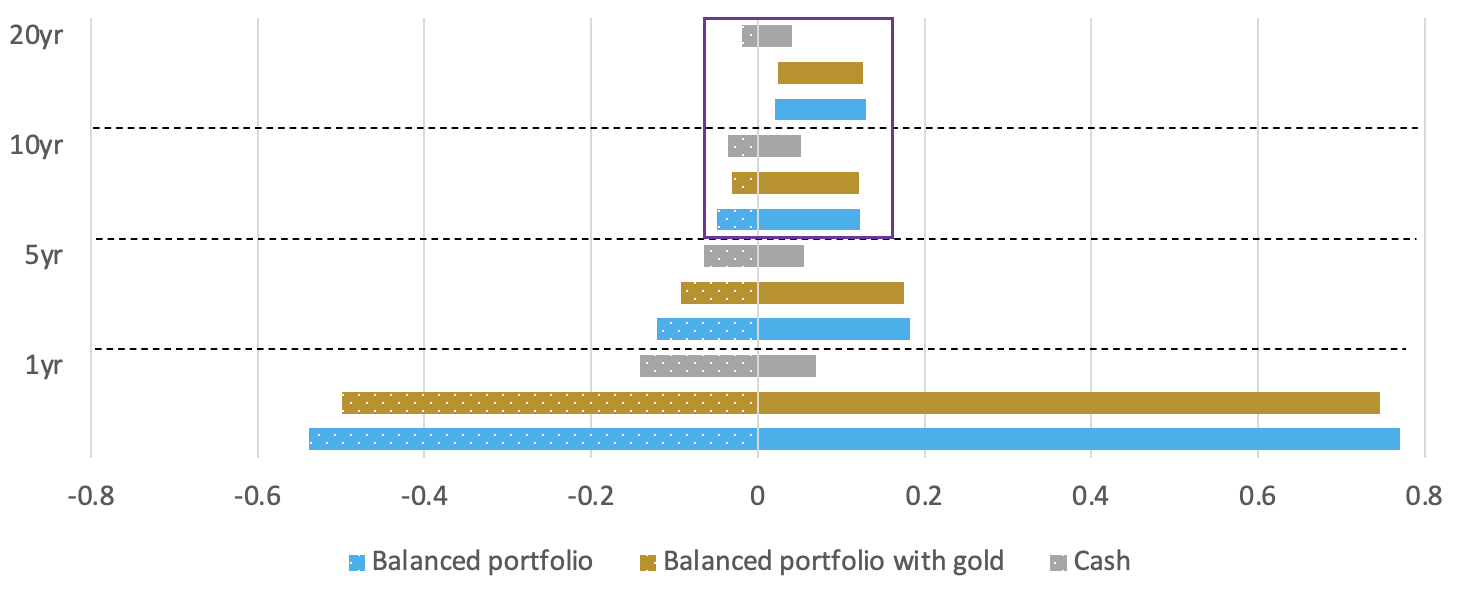

From an asset allocation perspective, investors should remember the longer-term historical record of equities, bonds and gold. Moreover, looking for historical guidance on which assets to hold shows the advantages of stretching your time horizon to increase certainty of achieving real returns (Chart 3).

Best and worst performance based on annualised real returns over a rolling 1-year, 5-year, 10-year and 20-year basis*

Source: Bloomberg, World Gold Council

*Data from 1972 to 2022. Computations based on y-o-y returns for each rolling window. Cash: Bank of England official bank rate. Hypothetical balanced portfolio: 60% equities (FTSE 100 Total Return index), 40% bonds (ICE BofA UK gilts Index). Hypothetical balanced portfolio with gold: 60% equities (FTSE 100 Total Return index), 35% bonds (ICE BofA UK gilts Index), and 5% gold (LBMA gold price).

Retrospectively, as one moves up the investment horizon, the range of outcomes narrows – even for a balanced portfolio, which is traditionally categorised as riskier than cash. In fact, our analysis shows that the risk-reward profile of a balanced portfolio with gold starts to look attractive relative to cash (as well as a balanced portfolio without gold) after five years. And over any single rolling 10-year period between 1972 and 2022, the worst real return for a balanced portfolio with gold is better compared to both cash and a balanced portfolio without gold. This demonstrates the advantages of focusing on long-term investments and gold’s diversification and return attributes.

If one stretches the investment horizon further, both balanced portfolios (with and without gold) have the added benefit of always delivering positive real returns over any single 20-year period over the past five decades. By contrast, cash does not, highlighting that long-term overweight cash allocations may come with opportunity costs.

In summary, our analysis shows that good investment outcomes over a medium- to long-term horizon come from good strategic decisions. Chart 3 underscores why we believe gold has a key role as a strategic long-term investment and as a mainstay allocation in a well-diversified portfolio, alongside equities and bonds.

More on market perspectives: Gold Mid-year outlook 2023: Between a soft and a hard place

使用微信扫一扫登录

[世界黄金协会]