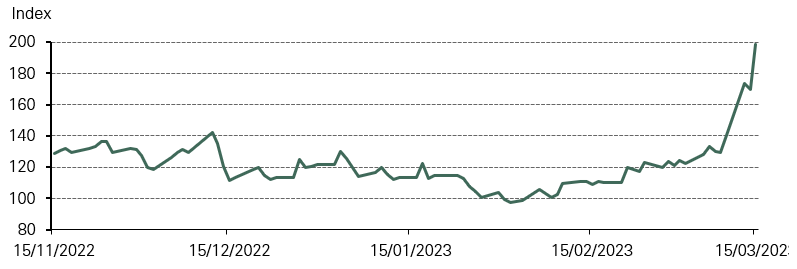

Faced with banking troubles on both sides of the Atlantic as well as uncertainty surrounding inflation and central banks, markets have gone through a brutal few weeks in terms of interest rate volatility (Chart 1).

Faced with banking troubles on both sides of the Atlantic as well as uncertainty surrounding inflation and central banks, markets have gone through a brutal few weeks in terms of interest rate volatility (Chart 1).

*As of 15 March 2023.

Source: Bloomberg, ICE BofA Move index, World Gold Council

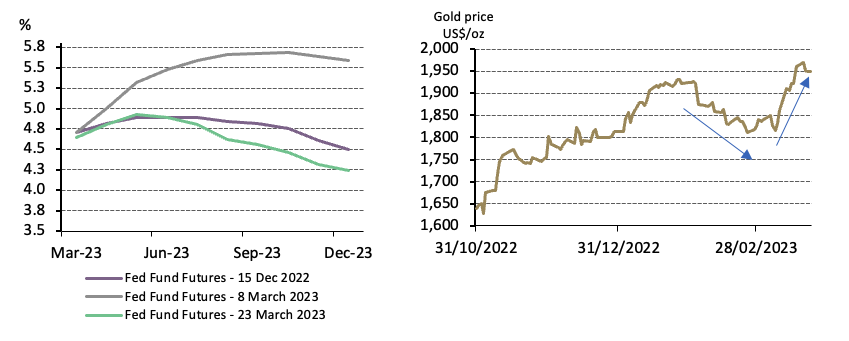

Gold has been directly impacted by these recent moves in interest rates (Chart 2). First, a sequence of stronger-than-expected US economic data prints (payrolls and retail sales in particular) and a barrage of hawkish comments from US Federal Reserve speakers generated a meaningful repricing up of the Fed Funds rate trajectory, negatively impacting gold. Next, a sharp risk-off move – triggered by mounting financial stability fears after the collapse of Silicon Valley Bank, Signature Bank and Credit Suisse – sent peak Fed rates down again, propelling gold higher. In this process, the implicit peak of the rate cycle has shifted from October back to May 2023, which means that the market is now expecting the tightening cycle to end much sooner.

*As of 23 March 2023.

Source: Bloomberg, World Gold Council

As it currently stands, how long the Fed will hold rates at elevated levels remains unknown. What is clear is that the Federal Open Market Committee is determined to avoid a replay of the 1970s and is under a lot of pressure to display an unwavering commitment to fighting inflation, even if, as some investors have suggested, its actions push the US economy into recession.

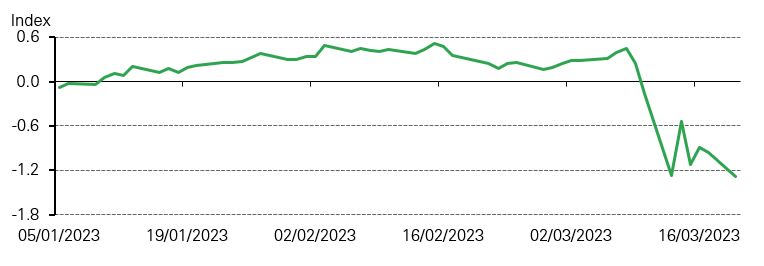

What is also clear is that getting inflation down to central banks’ 2% target is causing both economic and financial damage. The failure of two US regional banks and a major Swiss bank and the surge in UK government borrowing costs last year show that the effects of monetary tightening take time to filter through the economy and that the vulnerabilities associated with an aggressive tightening phase often show up in unexpected places. This will probably warrant caution on the part of the Fed, reinforcing our view that we may be closer to the peak of central bank hawkishness. This scenario would support gold particularly if accompanied by a mild recession – after all, a key issue over the coming months will be the extent to which the crisis of the past week causes banks to tighten credit (Chart 3). This in turn would weigh on consumer demand and business investment and therefore hurt growth.

*As of 20 March 2023.

Source: Bloomberg, Bloomberg United States Financial Conditions Index, World Gold Council

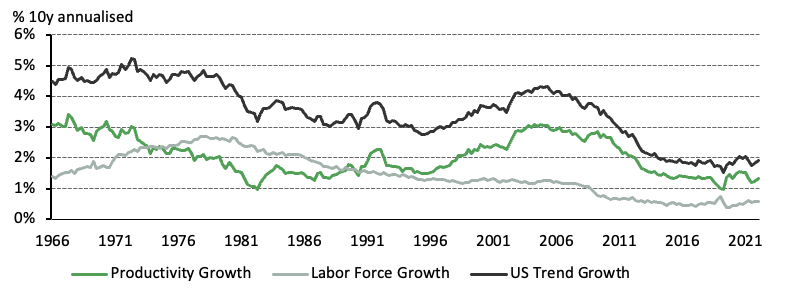

Looking along the investment horizon, it is also unlikely that gold will be met by headwinds from higher interest rates. There are risks to this outlook, of course, notably sticky inflation or bouts of inflation – due to long-term shifts in dynamics such as the clean energy transition or potential deglobalisation – which would keep Fed policy tight. That said, long-term structural indicators do continue to point to a low-growth, low-yield environment anchored by slow labour force growth and weak productivity growth (Chart 4).

*Data from March 1957 to December 2022. Trend growth is the sum of long-term labour force growth and productivity growth. Labour force and productivity growth rates are 10-year annualised numbers.

Source: Bloomberg, Bureau of Labor Statistics, World Gold Council.

Moreover, debt levels also continue to be high, further constraining a strong growth environment. In fact, businesses, consumers and governments face increasing interest costs as a percentage of income, reducing expenditure and growth potential in the economy.

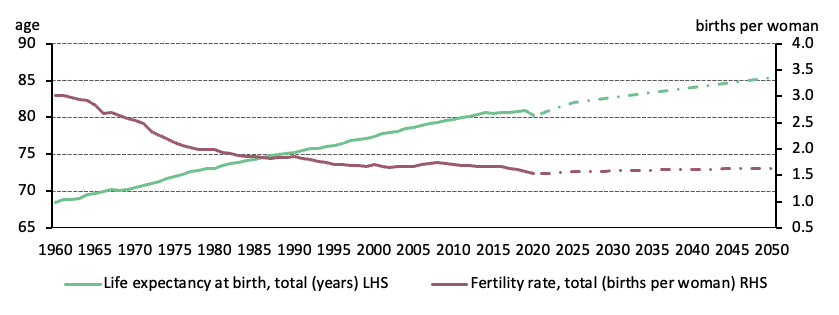

Demographics have also been trending downward for several decades and are expected to continue to do so in high-income countries (Chart 5). This is important as it determines the relative number of (net) savers and borrowers in the population of a country. Young people are generally borrowers. Middle-aged and elderly people are generally savers. An ageing population means that there are fewer opportunities for savers to deploy their savings. This creates a borrower’s market in which interest rates are pushed lower to encourage more borrowing.

* Data from 1960 to 2020. 2021 to 2050 are forecasts.

Source: The World Bank, World Gold Council.

Cyclical developments in growth and inflation will dominate the short-term outlook. And while it is likely that the Fed pricing moves back up again, especially if recent financial sector fears can be put in the rear-view mirror, investors should keep an eye out for a hint from the Fed that it is close to done. This could provide more support for gold.

Longer term, gold has a key role as a strategic long term investment and as a mainstay allocation in a well-diversified portfolio. While investors have been able to recognise much of gold’s value during times of market stress, the structural dynamics pointing towards a low-growth, low-yield environment should also be supportive for the precious metal.

使用微信扫一扫登录

[世界黄金协会]