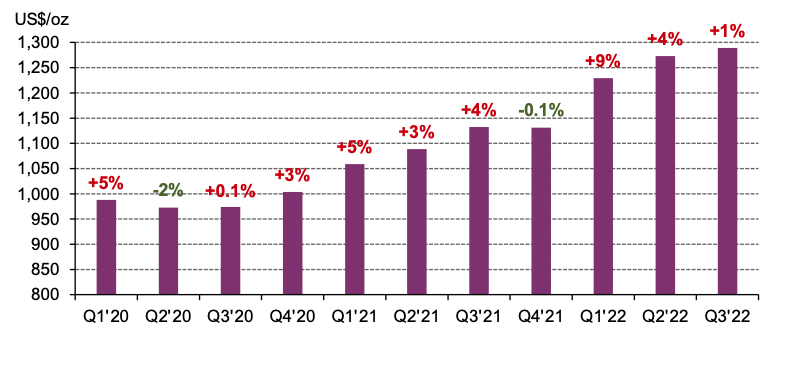

Average all-in sustaining costs (AISC) in the gold mining industry increased by 1% q-o-q in Q3’22, reaching a new record high of US$1,289/oz. This was the third consecutive quarter of rising costs, with the average AISC also reaching new record highs in both Q1’22 and Q2’22 before being surpassed in the latest quarter. The average gold AISC is now 14% higher than it was in the same quarter last year and 32% higher than in Q3’20.

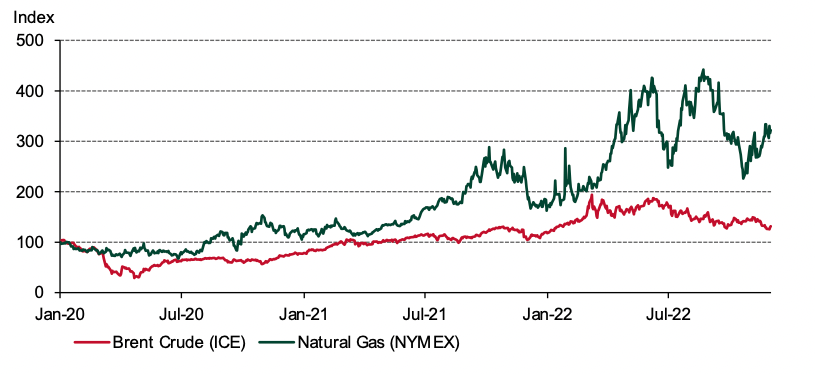

This significant rise in costs has largely been driven by inflation of almost all input costs for miners. In particular, a tight labour market in many major gold producing countries has led to increasing wage rates and therefore rising staff costs. Meanwhile, rising oil and gas prices, especially following Russia’s invasion of Ukraine, have pushed up the price of diesel and electricity. Higher prices for these commodities, alongside increased ammonium nitrate prices, has also had the knock-on effect of increasing the price of key consumables for miners, such as cyanide and explosives.

Average AISC and quarter-on-quarter percentage change

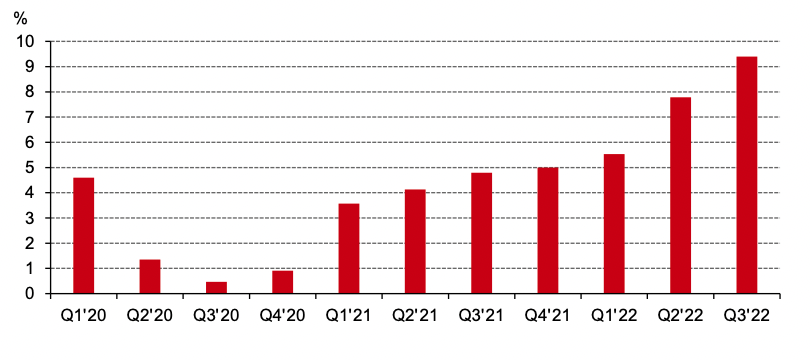

These rising costs have increasingly been putting higher cost gold production under pressure. In Q3’21 5% of gold production was operating with an AISC above the gold price, in Q3’22 this figure had increased to 9%. As a result, some higher cost mines, such as PureGold in Canada and Beatons Creek in Australia, have been placed into care and maintenance this year.

Despite another rise in industry average AISC in the last quarter, there now appears to be some respite from the relentless cost inflation gold miners have faced this year as the rate of increase has slowed. The 1% q-o-q rise in Q3’22, compares to a 4% rise in the previous quarter and 9% in Q1’22. This is largely the result of stabilising, although still high, oil and gas prices.

Looking ahead to Q4’22, we expect the industry average AISC to remain high, however falling oil and gas prices in the second half of 2022 could result in a flattening of costs or even a modest contraction.

Brent Crude and Natural Gas Futures Prices