Highlights:

- International gold prices reached a new record high in early March, rising well above US$2,100/oz and increasing more than 6% m-t-d.1 Weaker economic data in the US, a decline in the USD, a fall in US Treasury yields, and geopolitical tensions all helped push up the price of gold

- Domestic gold prices also rose to all-time highs, reaching INR 66,529/10g2 in March, up 4% m-t-d- a slightly lower percentage increase than the USD counterpart due to INR strength

- The gold price surge has dented consumer demand; as a consequence the domestic gold price is now trading at a discount of around US$20/oz in relation to the international price

- The price surge presents headwinds for gold demand, even in the face of the ongoing wedding season

- The RBI added 4.7t of gold in February, taking its gold reserves to an all-time high of 817t

- Indian gold ETFs saw inflows of US$93.3mn in February, the strongest monthly inflow for six months

- February saw a sharp rise in gold imports

Looking ahead:

- During the general election period (April to June), there will be heightened scrutiny on the movement of gold and cash

- Gold jewellery demand will likely remain subdued, even if prices moderate over the coming months

- Meanwhile, higher prices could encourage investment into gold-linked financial products.

Upsurge in gold prices

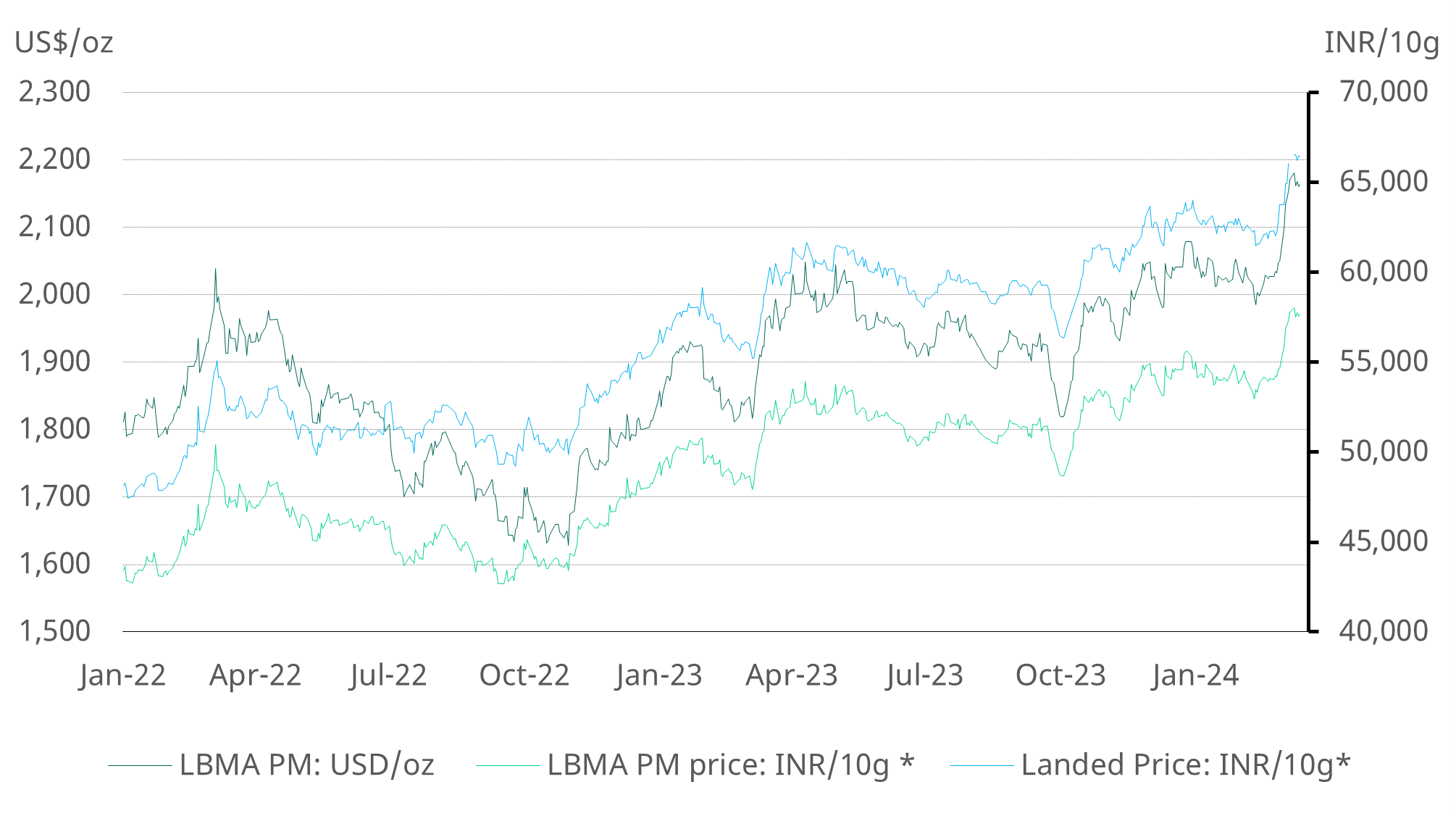

Following its 0.3% decline in February, gold reached a new all-time high in early March, rising by more than 6% in the first week of the month and at the time of writing is trading well above US$2,100/oz. The price increase can, in part, be explained by USD weakness, a decline in US Treasury yields, an increase in market volatility, weak US economic data print, and other factors such as ‘technicals’ and over-the-counter activity.

While the gold price touched record highs in USD and other major currencies, the INR included, the domestic landed price in India witnessed a smaller increase of 4% to INR66,529/10g due to the strength in the rupee (0.2% appreciation w/w).

Chart 1: Gold prices at record high

LBMA price and domestic landed price by month, US$ and INR*

Record prices choke demand

The recent gold price spike has added further pressure to gold jewellery demand, already depressed by the high prices of recent months. Anecdotal evidence and media reports suggest that both rural and urban centres have experienced a broad-based drop in demand despite the ongoing wedding season.3 It appears that jewellers and consumers alike are awaiting a price correction before they add to their stock or buy jewellery.

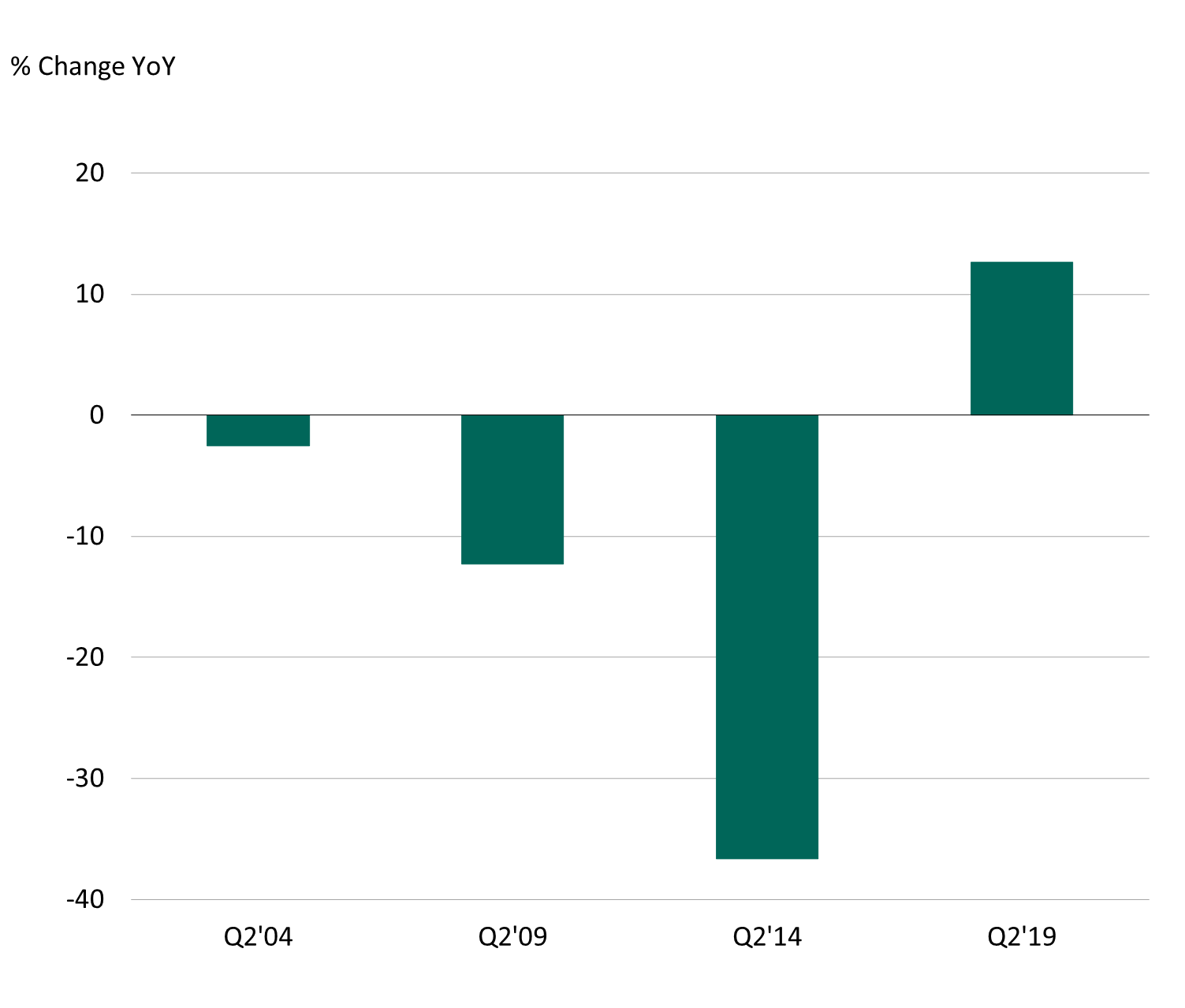

Demand is unlikely to see a notable uptick in the next couple of months, even should prices moderate, as the country’s impending general elections (April to June), will see the movement of gold and cash closely monitored.4 Data shows that gold consumption fallen during three of the last four general election periods (Chart 2). Some improvement in demand could be expected around the time of Akshaya Tritiya (10 May), as this is traditionally considered to be an auspicious time to buy gold.

Chart 2: Gold consumption tends to drop ahead of general elections in India

Percentage y/y change in gold consumption during the general election quarter

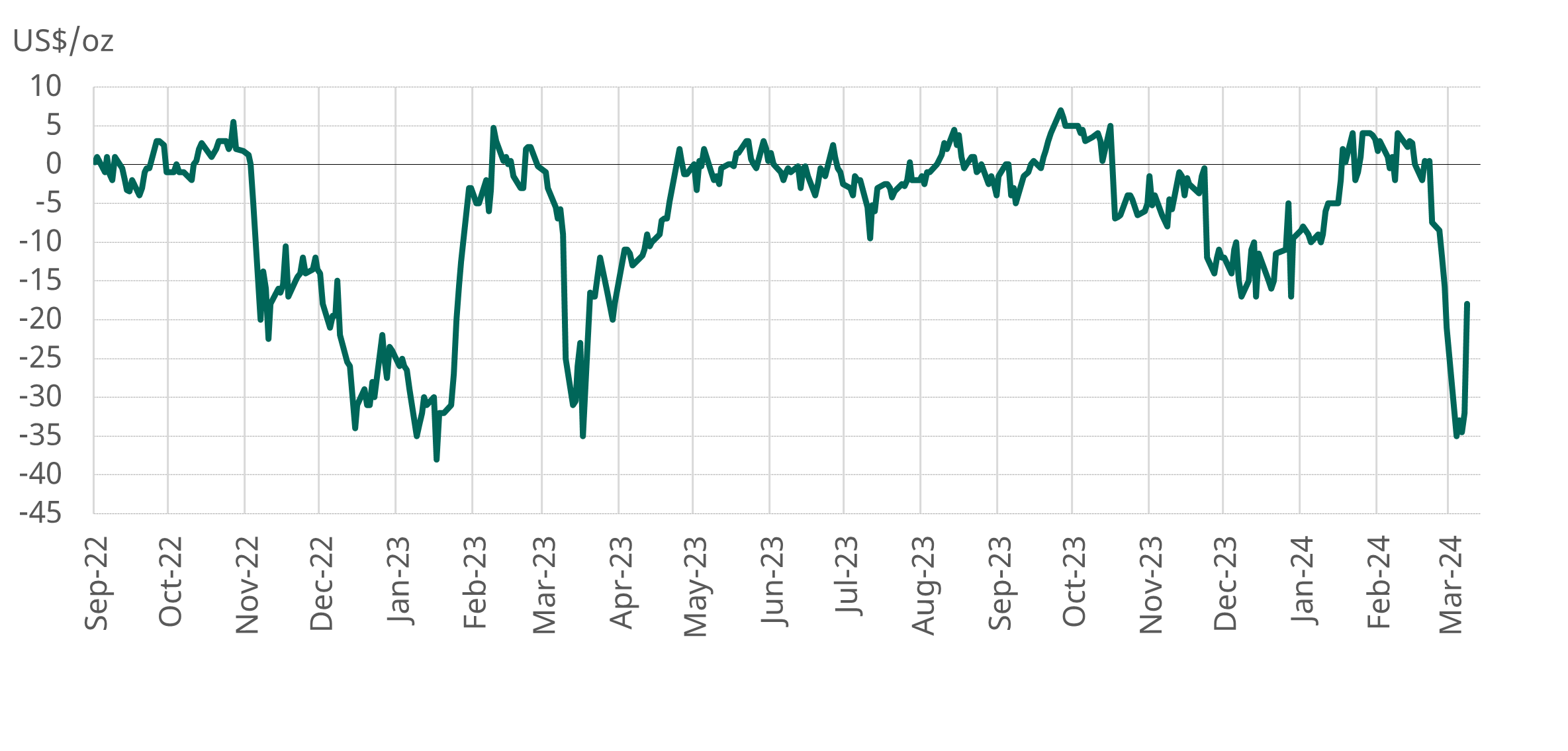

Gold trades at a discount in the domestic market

After trading for much of February at a small premium, domestic prices have reverted to a discount in relation to international prices. The local price is now trading around US$ 20/oz below the international price (as of 15 March) from a premium that ranged from US$0.25/oz to US$4/oz in February. The price rise has crimped demand and persuaded jewellers, likely carrying inventory bought before the surge, to sell below the current international gold price, as even in the face of weak demand they can still make a profit. In fact, our analysis shows that there is a small negative correlation (-0.2%)5 between the international gold price and the domestic premium/discount.

Chart 3: Domestic gold prices return to trading at a discount

NCDEX gold premium/discount relative to the international price

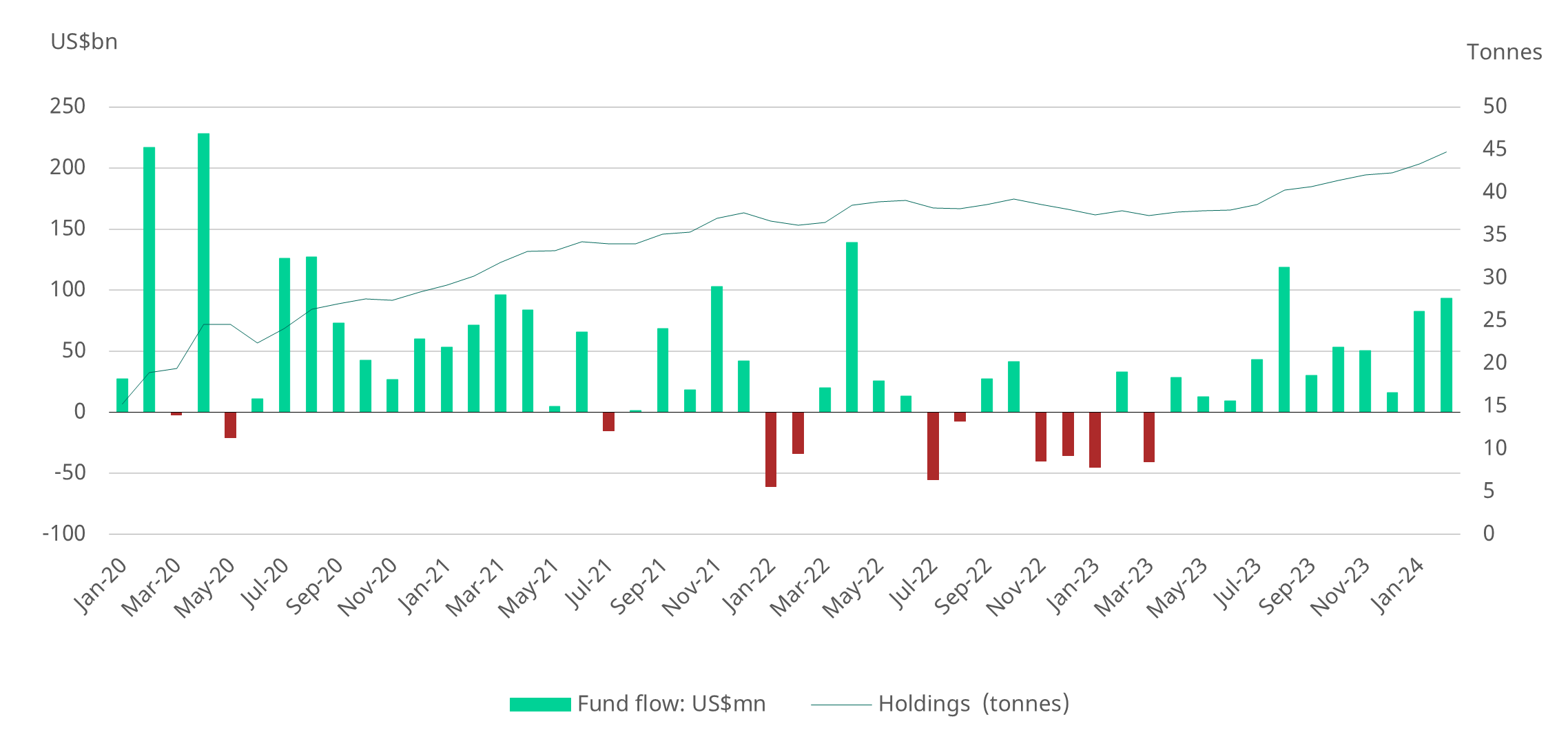

Indian gold ETFs maintained positive momentum

Inflows into Indian gold ETFs persisted in February, marking the eleventh consecutive month of inflows and reaching US$93.3mn, the highest for six months.

At the end of February, assets under management (AUM) in Indian gold ETFs stood at US$3.3bn (INR285.3bn, 33% y/y) with 44.7t of holdings, up 18% y/y. Inflows into these funds demonstrate the growing inclination of investors to include gold ETFs in their portfolios. Net inflows in these funds in the first two months of 2024 totalled US$176mn (INR16bn), a stark contrast to the net outflow of US$12.3mn (INR0.34mn) in the same period last year.

Gold ETF inflows have been fuelled by a number of factors, including the surge in gold prices, a growing appetite for tradeable financial products, a substantial increase in capital market investment6 and the need for diversification, and geo-political tensions. Despite the recent inflows, gold ETFs nevertheless account for only a small fraction (0.5%) of AUM in Indian Mutual Funds. The huge increase in capital market inflows holds potential for this segment, as evidenced by the recent spate of gold ETF launches. Four new gold ETFs have come to the market in just the last six months taking the tally of India’s gold ETFs to 17.

Chart 4: Steady stream of inflows into Indian gold ETFs

Monthly gold ETF fund flows in US$bn, and total holdings in tonnes*

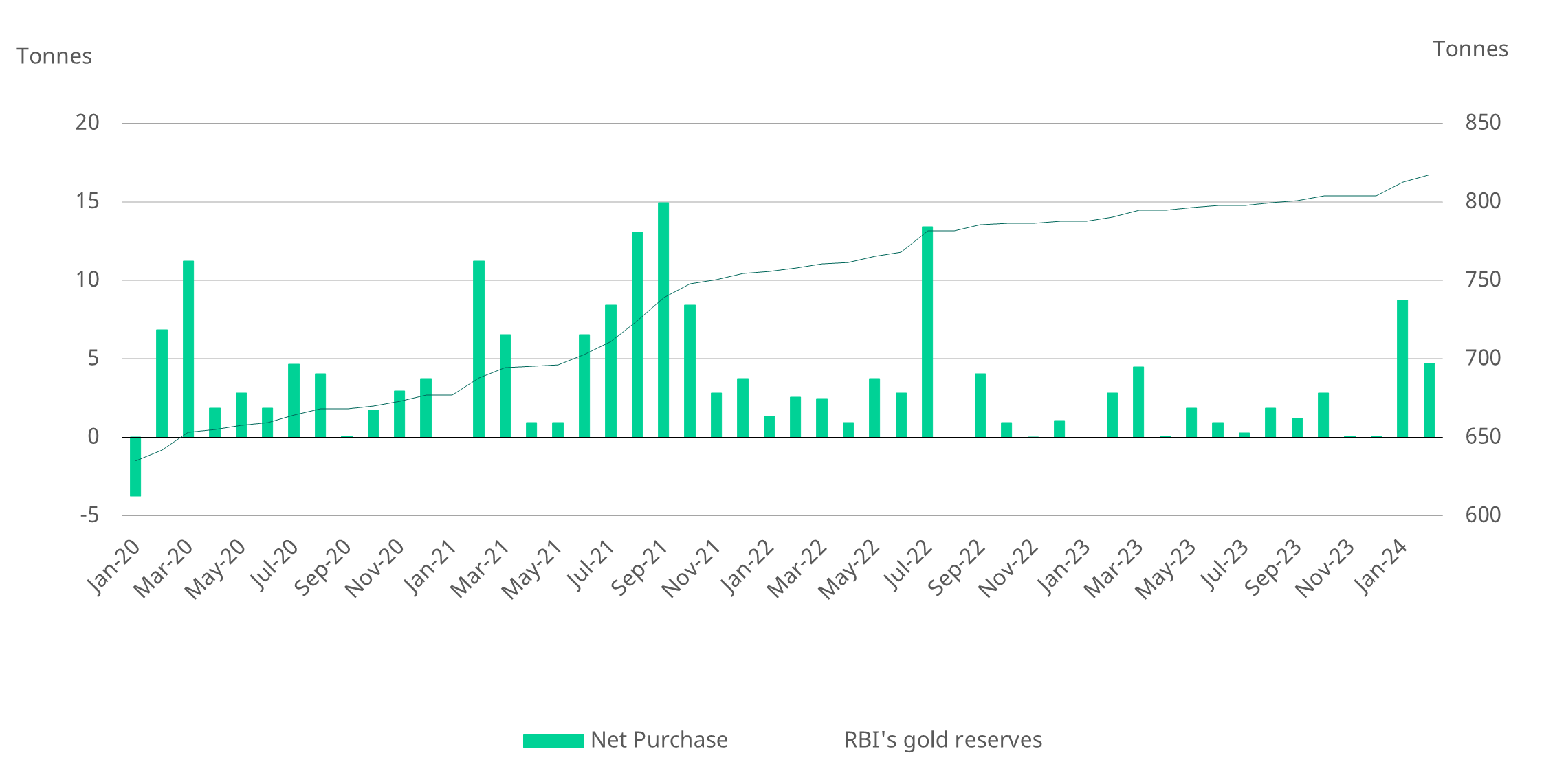

RBI builds its gold reserves

The RBI added to its gold holdings in February. RBI data and our own estimates indicate that the central bank was a net buyer of 4.7t of gold during the month.7 This follows 8.7t of gold acquired in January and brings the RBI’s gold holdings to an all-time high of 817t at the start of March.8 As a percentage of forex reserves, gold accounted for 7.7% at the end of February.

The RBI’s net gold buying in the first two months of 2024 (13.4t) already amounts to more than 80% of its 2023 annual net purchase (16.2t) and represents the largest purchase for the period since 2015. The RBI is among several central banks that have been accumulating gold at a steady clip. . Its annual net gold purchases averaged 42t (2018 to 2023).

Chart 5: RBI increases its gold holdings

RBI’s monthly net purchase and reserves, tonnes*

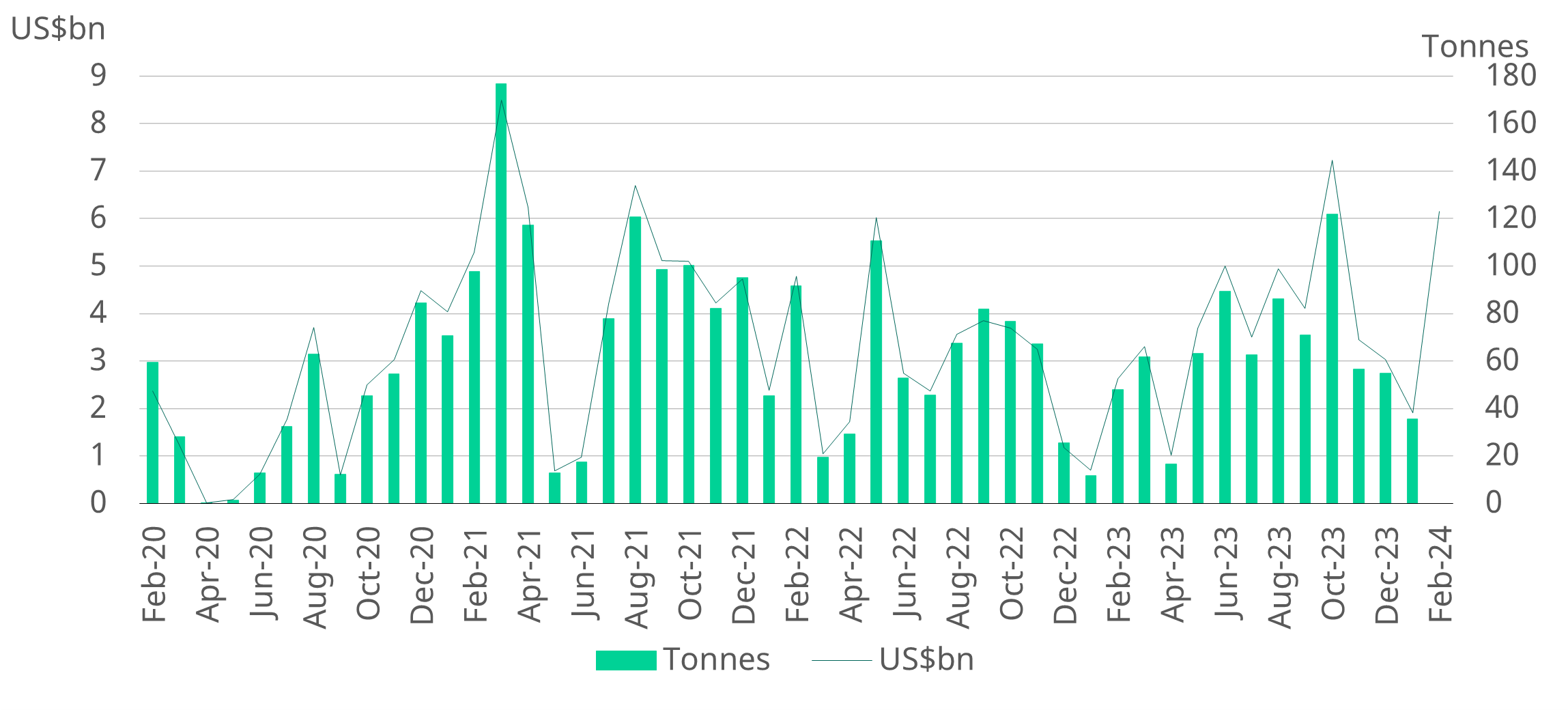

Gold imports surge appreciably

Despite elevated prices and soft jewellery demand, gold imports in February saw a substantial increase on an annual (134%) as well as sequential basis (222%). Imports during the month at US$6.1bn were the highest since October and follow three months during which they were repressed.

In volume terms, as per our estimates, gold imports in February were likely over 90t, notably higher than the average 49t imported in the preceding three months as well as a year ago. The rise may be due to an anticipated increase in demand during the wedding season, and bullion dealers, manufacturers front-loading inventories ahead of the general elections.

Gold imports fluctuated considerably during the current financial year. Monthly gold imports in the eleven months period (April-February) of the fiscal varied between 16.7t and 121.9t(US$1.0-7.2bn). This represents a rise of over 20% in volume y/y but remains 8% lower than the pre-pandemic average (FY15-19).

Chart 6: Gold imports surge

Monthly gold imports, tonnes and US$bn*

Footnotes

LBMA Gold Price PM as of 15 March 2024

Landed prices include import tax but excludes GST

Gold surge could dull Indian wedding season demand

The election commission imposes a code of conduct under which the limit for carrying cash is fixed and the transport of items such as gold and jewellery come under heightened scrutiny and can even be confiscated

Correlation between LBMA AM Fix and NCDEX polled gold premium/discount from 2 Jan 2020 to 15 March 2024

Net assets under management in Indian mutual funds as of end February 2024 stood at INR.54.5tr (45% y/y)

RBI weekly statistical supplements

Data to 1 March 2024