Key highlights:

- The Shanghai Gold Benchmark PM (SHAUPM) in RMB stayed virtually unchanged in February while the LBMA Gold Price AM in USD saw a mild fall of 0.3%. Both RMB and USD gold prices gained momentum in early March, however, refreshing their record highs.

- Last month saw 127t gold leave the Shanghai Gold Exchange (SGE), above the ten-year February average (118t)

- The local gold price premium remained elevated, supported by robust gold consumption and possible declines in supply due to a shorter working month

- Chinese gold exchange traded funds (ETFs) saw their third consecutive monthly inflow, adding RMB778mn (+US$109mn) and pushing their total assets under management (AUM) to another record high of RMB31bn (US$4.3bn)

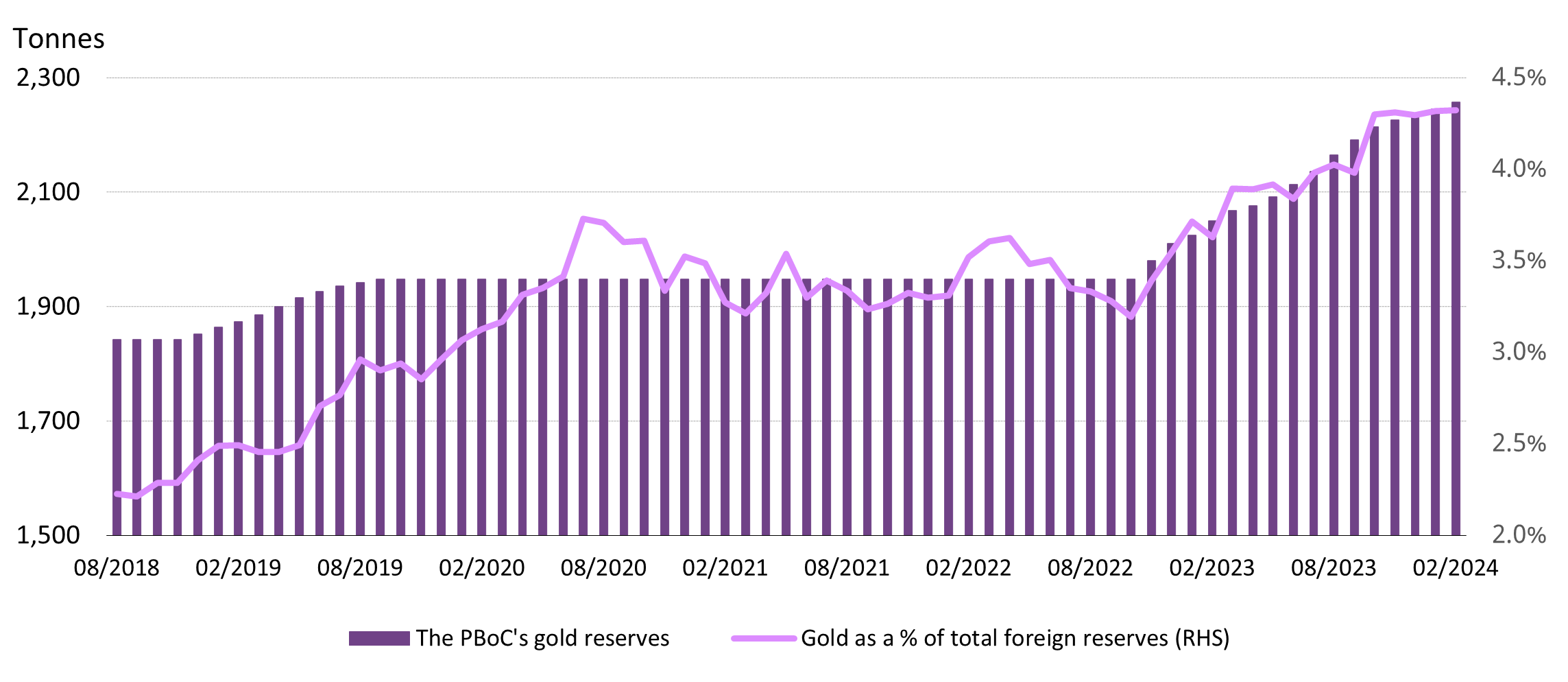

- Official gold reserves in China have now risen for 16 consecutive months; the addition of 12t in February pushed their total to 2,257t – 4.3% of the country’s foreign exchange reserves.

Looking ahead:

- In the near term, more working days in March and improved replenishing activities – as inventories stocked before the Chinese new year (CNY) holiday are depleted – should support a m/m rebound in wholesale gold demand

- But the gold price rally – especially as it reached new highs recently – combined with the fact that we are entering the off season for gold consumption may exert pressure on local gold consumption over the coming months.

- As a counterbalance, the same price action may continue to support investment demand for gold

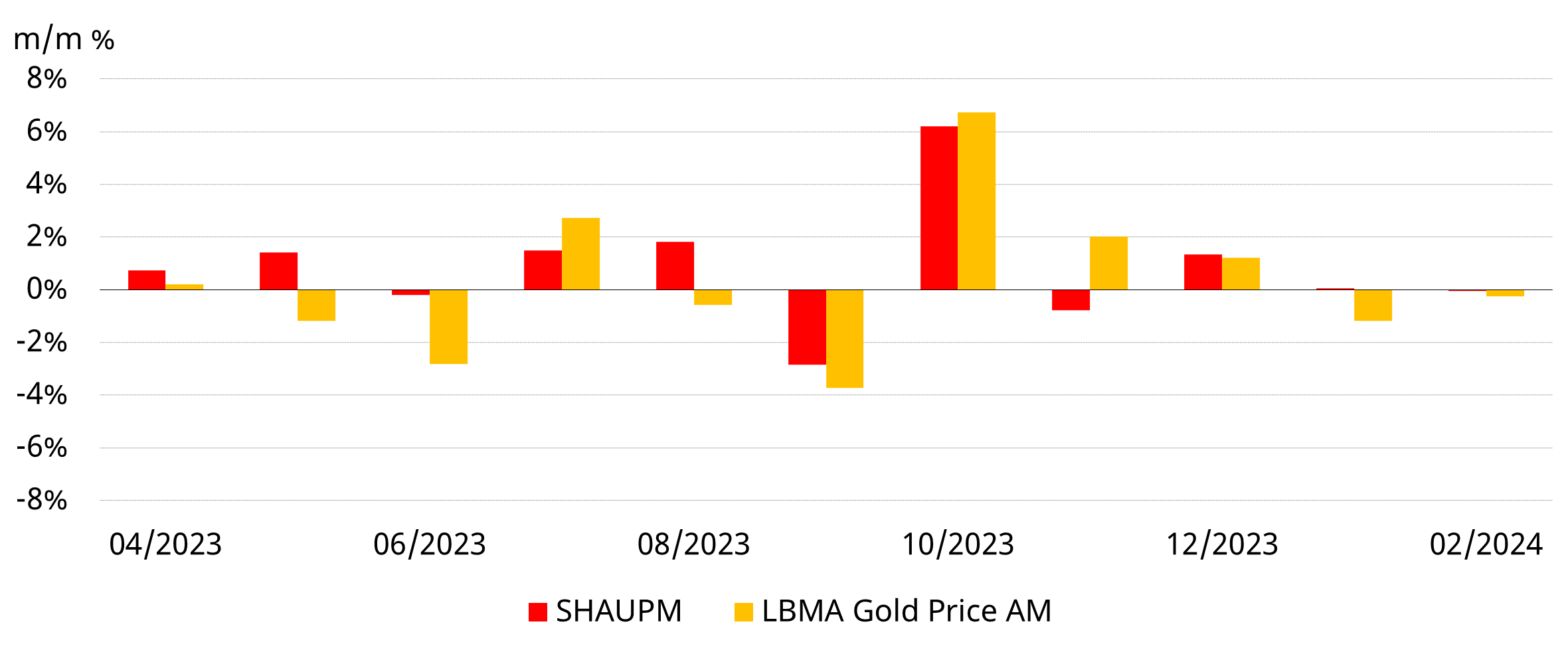

February saw limited change in the gold price

Gold prices remained stable in February (Chart 1). Both the SHAUPM in RMB (-0.04%) and the LBMA Gold Price AM in USD (-0.3%) saw mild declines as investors adjusted their bets on major central banks’ monetary policy pivots. Depreciation in the local currency against the dollar cushioned the monthly loss in the RMB gold price.

Chart 1: Gold prices stable in February

Monthly changes of SHAUPM and LBMA Gold Price AM*

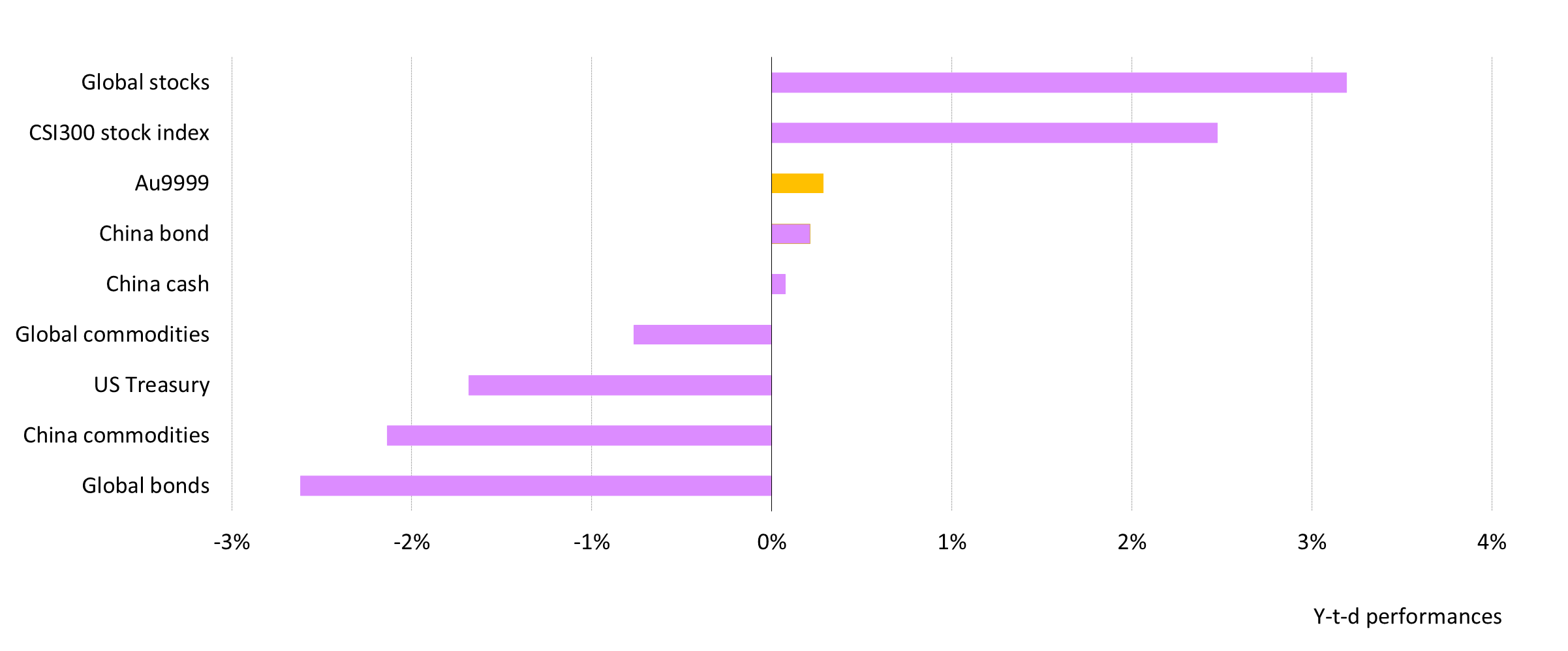

During the first two months of 2024, RMB gold has held steady, capping a mild gain of 0.3% and still outperforming other assets such as global bonds and commodities (Chart 2). Meanwhile, global equities are roaring towards new records and Chinese stocks, supported by local stimuli also improved markedly. But gold remains a popular asset in China, evidenced by continued gold ETF inflows and the recent strong demand for physical gold.

Further, the gold price has reached new record highs in early March, and the local gold price now stands above RMB500/gram for the first time in history which may continue to increase the allure to investors.

Chart 2: Risk assets soared, RMB gold steady

Major asset performances so far in 2024*

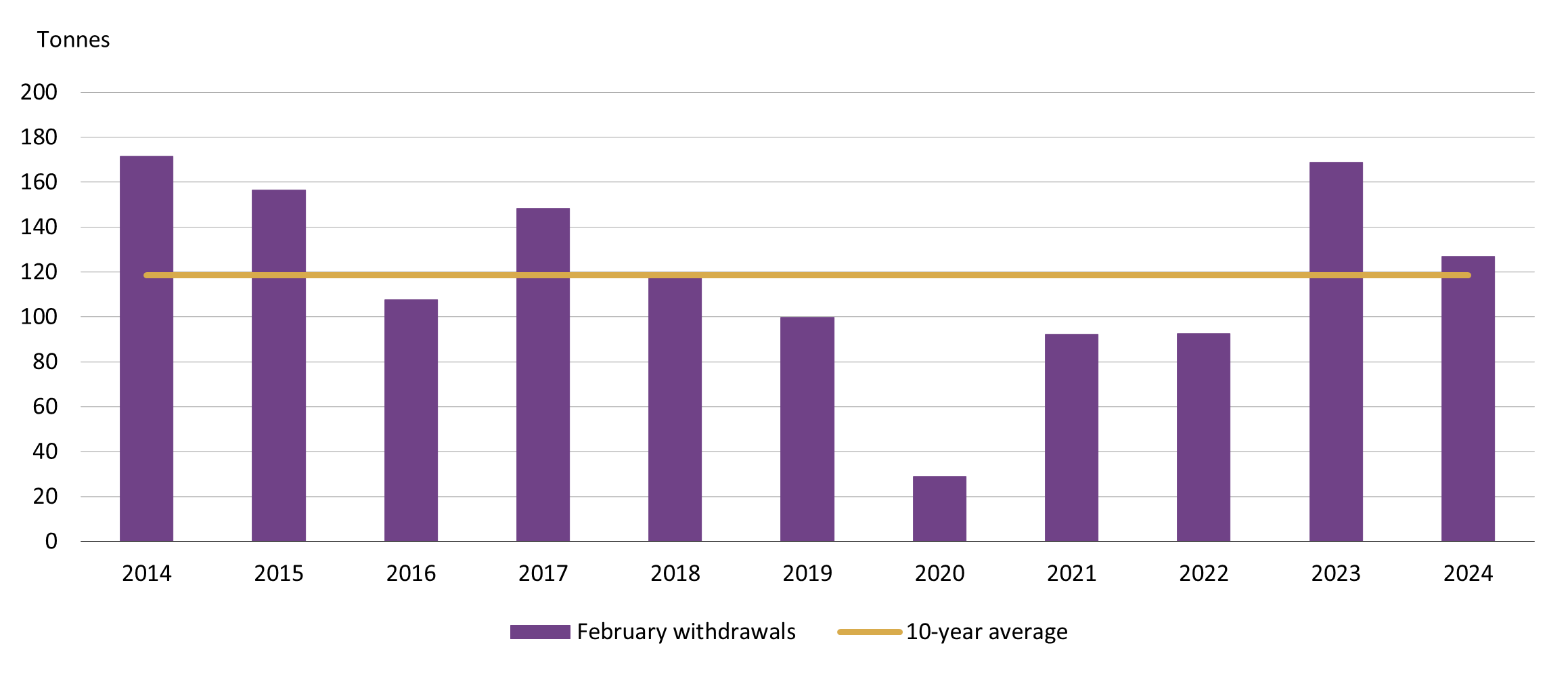

Wholesale demand remained above its long-term average

Gold withdrawals from the SGE added up to 127t in February (Chart 3), a 53% plunge m/m and a 25% fall y/y. But we cannot arbitrarily draw the conclusion that gold demand weakened. The m/m plummet was mainly due to:

- less trading days in February than in January, due to the CNY holiday (10~17 February)

- seasonally lower wholesale gold demand as manufacturers wind down inventories they stocked in preparation for the festival

- the strongest January gold withdrawals ever.

In fact, the combination of CNY and fewer trading days has produced m/m declines every February on record except in 2023, when the Spring Festival occurred unusually early. In that instance, January had fewer trading days and the start of the year was supported by pent-up demand after the fresh removal of COVID restrictions. The exceptional high base of 2023 was also the main contributor to the y/y decline in last month’s wholesale gold demand figure.

Nonetheless, 2024 saw the second highest February wholesale gold demand since 2017, remaining above its ten-year average of 118t.

Chart 3: February Wholesale gold demand remained elevated

Gold withdrawals from the SGE in February and the ten-year average*

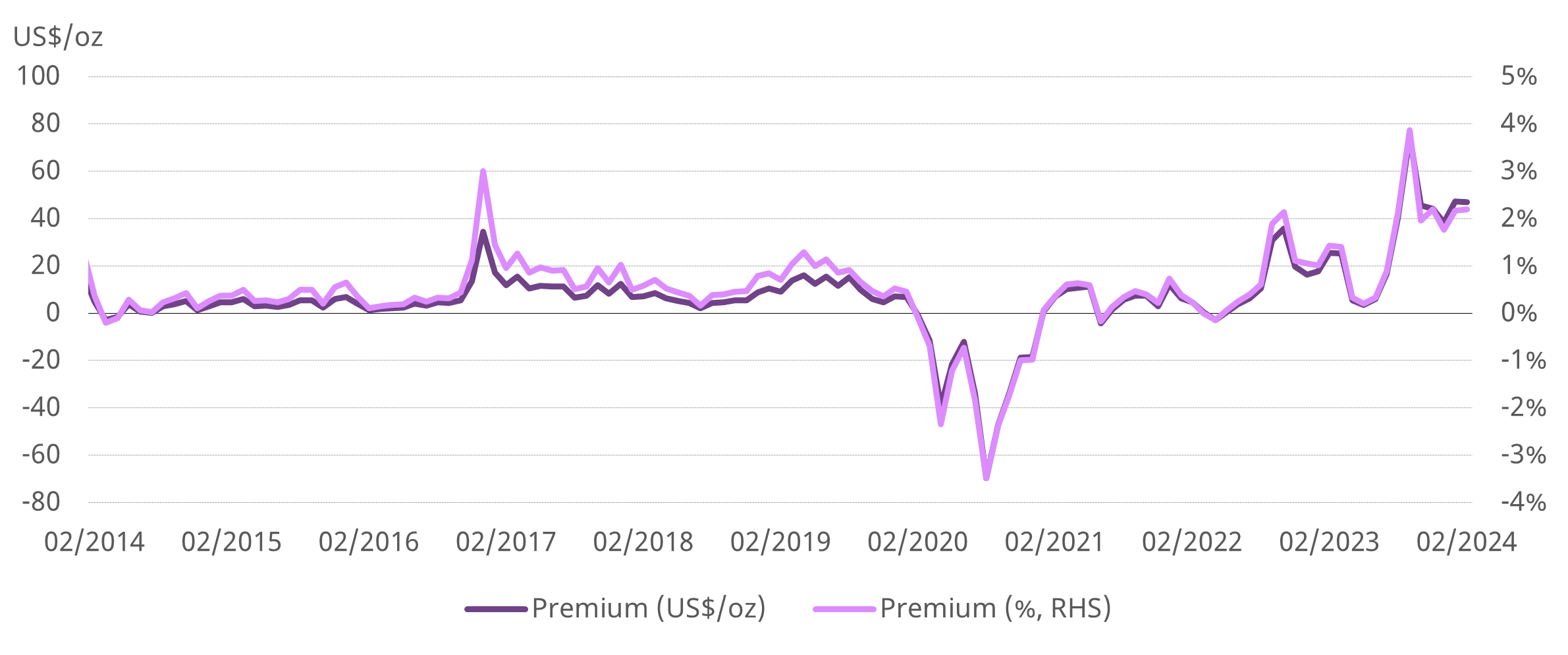

Local premium also remains elevated

The average Chinese gold price premium was unchanged at US$47/oz in February (Chart 4). This is mainly a result of strong physical gold demand during the CNY holiday as well as possibly lower imports – amid fewer working days in February.

Chart 4: The local gold price premium stabilised

The monthly average spread between SHAUPM and LBMA Gold Price AM in US$/oz and %*

Chinese investors continued to add gold ETFs

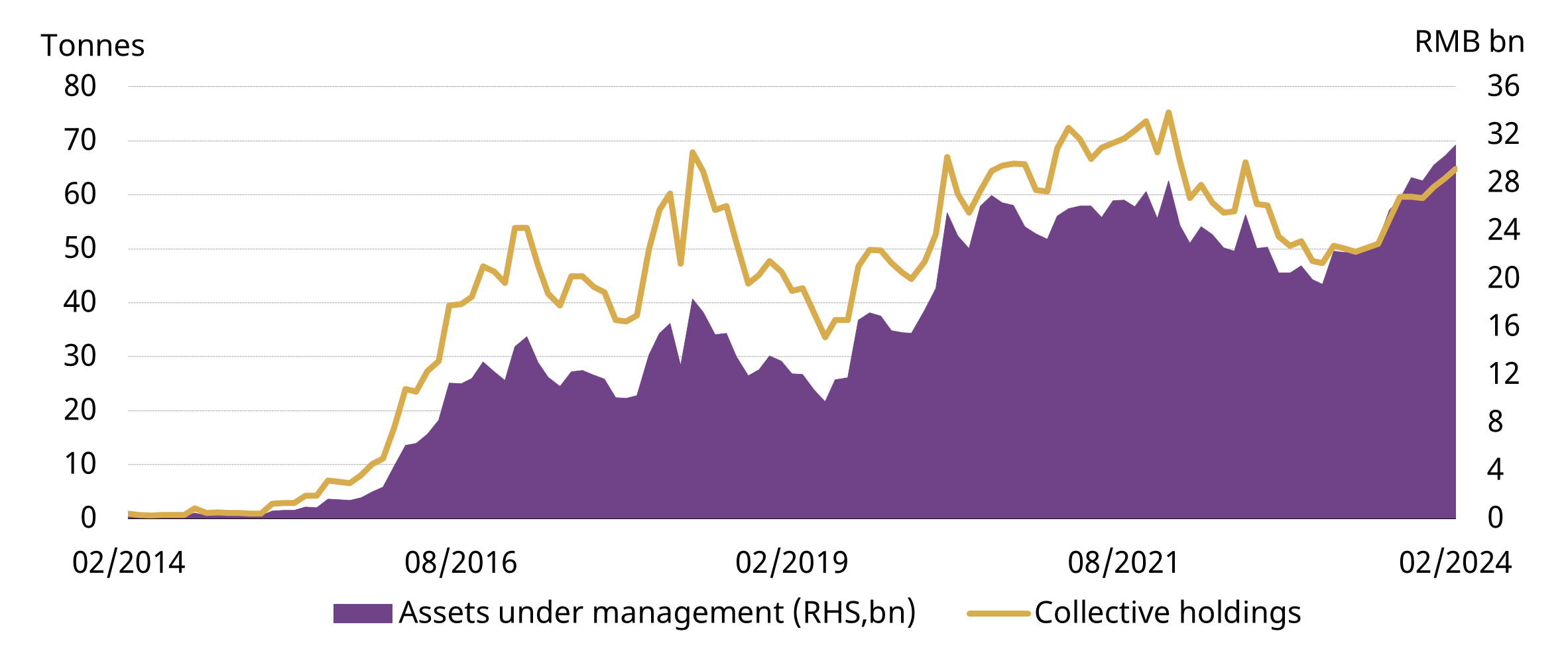

Chinese gold ETFs extended their inflow streak to three months, adding RMB778mn (US$109mn) in February (Chart 5). Their total AUM ended the month with another record high of RMB31bn (US$4.3bn) whilst collective holdings rose by 1.7t to 65t.

Even though domestic equities saw a sharp rebound in the month, non-stop declines in the six months to February kept investor safe-haven demand elevated. Meanwhile, continued depreciation in the local currency and a stable gold price attracted investors who saw further upside potential in the RMB gold price.

Chart 5: Chinese gold ETF AUM refreshed its record high in February

Monthly fund flows and Chinese gold ETF holdings

The People’s Bank of China (PBoC) reported another gold purchase

The PBoC announced a 12t gold addition in February, extending its buying spree to 16 months and lifting the total to 2,257t (Chart 6). So far in 2024, China’s gold reserves have increased by 22t. And during the past 16 months the PBoC has reported total gold purchases amounting to 309t.

At the end of February gold accounted for 4.3% of China’s total foreign exchange reserves, up from 3.4% in November 2022, the time at which the PBoC resumed its gold purchase announcements.

Chart 6: China’s gold reserves rose further