You asked, we answered: Are we running out of gold?

12 March, 2026

Introduction

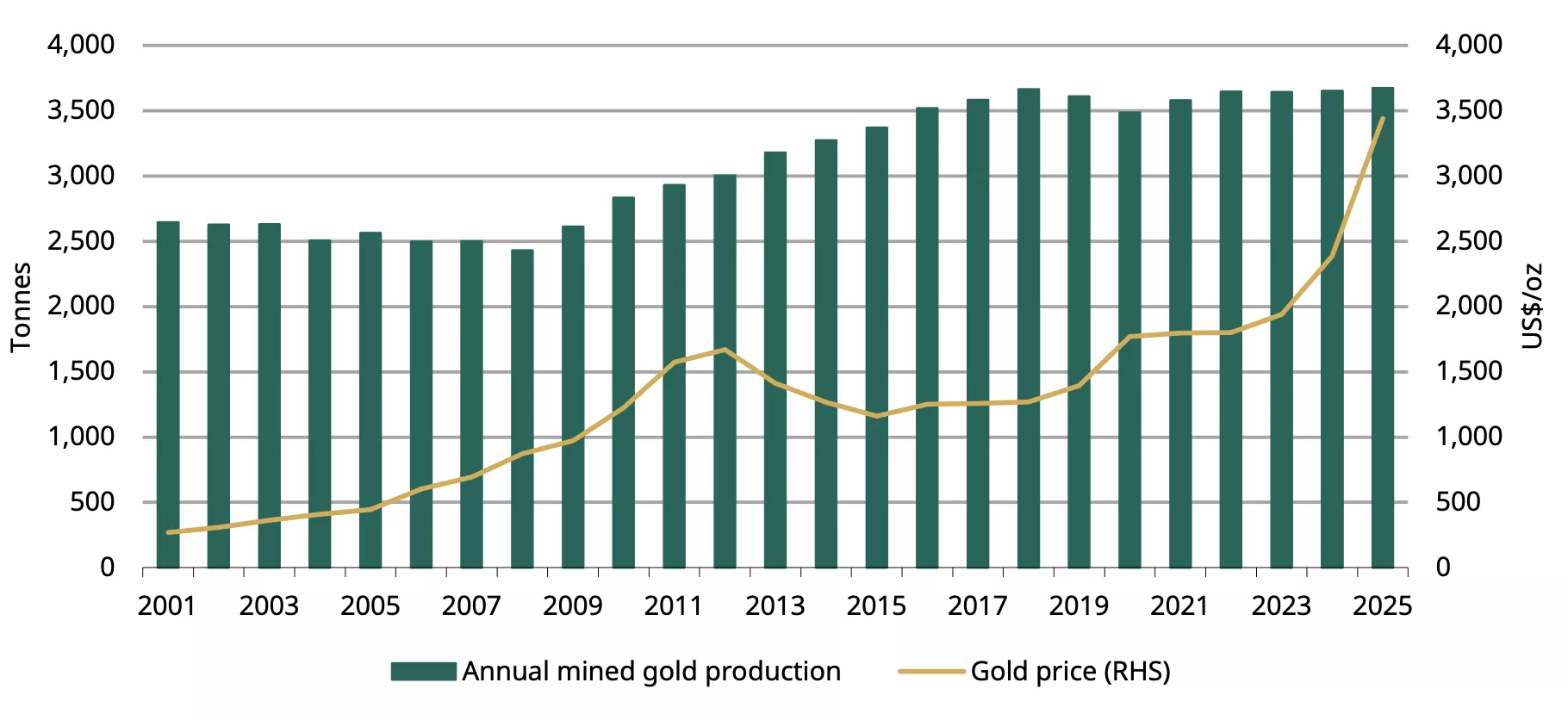

Mined gold production reached a record high in 2025, based on our 2025 Gold Demand Trends report (Chart 1). Global miners produced 3,672t of gold, a modest y/y increase of 1% and the highest in our data series – albeit this may be subject to revisions when more data becomes available.1 And we expect mined gold production to further increase in 2026 – at a mild pace – as operations resume at two major mines.

Chart 1: A modest increase took 2025 mined gold production to the highest in our data series

Source: Metals Focus, Refinitiv GFMS, World Gold Council

In our previous post, we explained why gold mine production typically lags the gold price and we discussed the possibility that production will plateau over the coming years. A key reason for this is that the new gold mining projects are getting harder to discover, due mainly to geopolitical instability in many prospective regions; lengthening development timelines amid protracted permitting processes for environmental and social licenses; rising capital costs; and complicated project financing in remote areas.

Based on the annual reports of major gold mining companies, the 2026 production outlook is generally cautious – most forecast declines compared to 2025. Without more discoveries, current reserves naturally deplete – perhaps at a faster pace should the gold price keep rising – which could possibly encourage production to accelerate. This has raised concerns from investors:

- Are we approaching a structural shortage of mineable gold?

- If not, when can a meaningful supply response be expected?

- Should any major discoveries be found, will they suppress the gold price?

- Could gold supply be manipulated?

In this update, we aim to provide some guidance for investors regarding these questions.

Will we eventually run out of gold?

There are two parts related to this question – the broader gold supply and mined production. Our answer to both is: not likely.

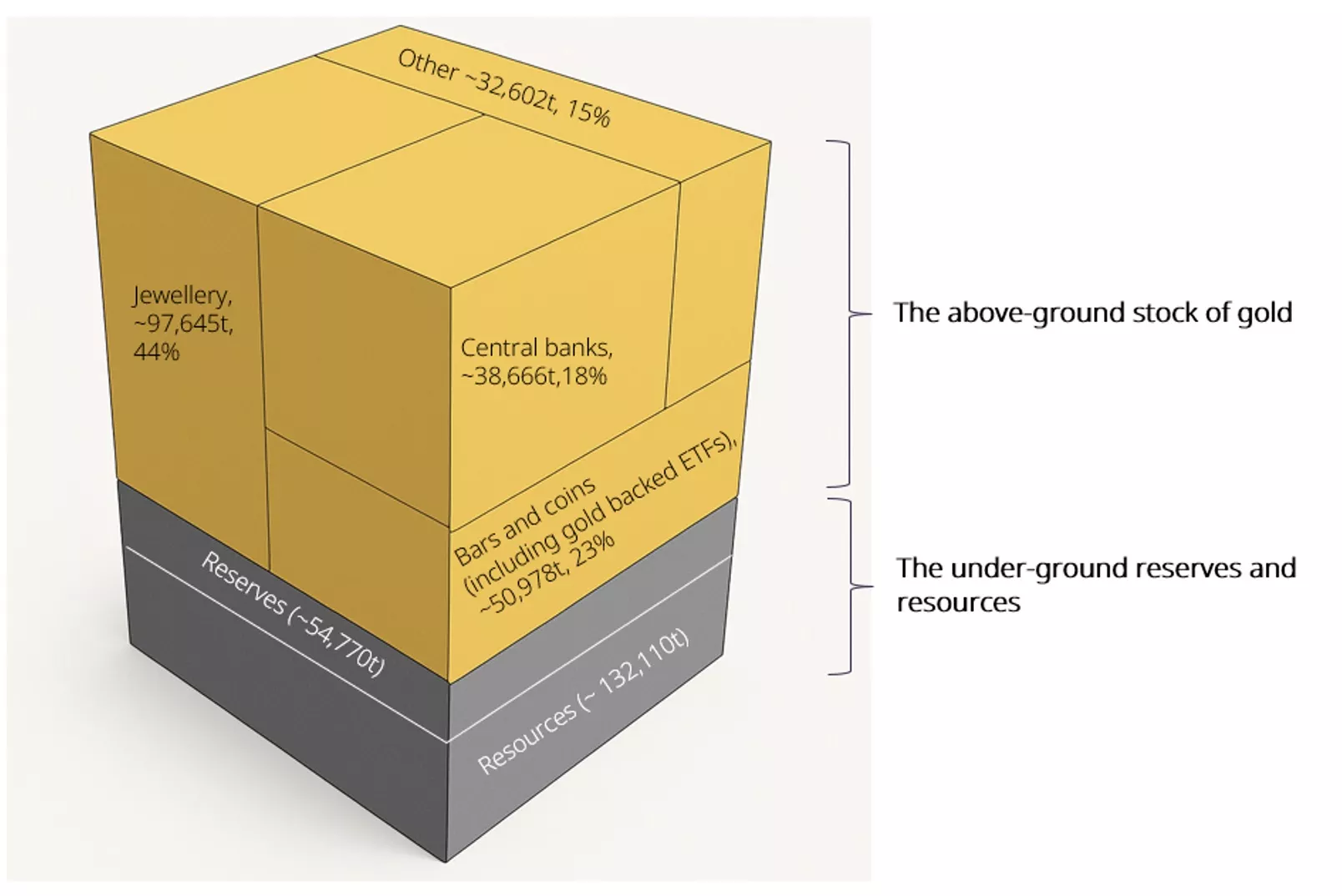

First, we are not likely to run out of gold supply. There are two major parts to supply: recycled gold and mined gold. While mined gold may be plateauing as noted previously, recycled gold supply comes from various sectors. As shown in Figure 1 below, total above-ground gold amounts to 219,891t. And because gold is virtually indestructible, almost all of it is available to come back to the market under certain market conditions. For instance, when the gold price is high, it may trigger sellbacks of gold jewellery from consumers and more industrial recycling – factors that are far more responsive to price than mined gold production.

Figure 1: The above-ground gold stock and under-ground reserves*

*End-2025 estimates from Metals Focus. Reserves are the portion of an ore deposit that can be economically extracted. For an ore deposit to be considered a reserve, numerous factors will have been assessed, such as geological, mining, processing, marketing, economic and ESG. Only once all of these have been taken into consideration and the ore is still economically viable will it be considered a reserve. Projects that have reached feasibility stage are likely to fall into this category. There are two types: proven and probable. Resources are the portion of a deposit in which companies have less geological knowledge and confidence, i.e. less drilling data and only simple economic modelling applied, or in some instances no economic modelling at all – it’s a broad category ranging from inferred, indicated to measured. Estimates for reserves and resources can vary, for example reserves are currently estimated to be ~64,000t by the US Geological Survey.

Source: Metals Focus, Refinitiv GFMS, World Gold Council

Second, we are not likely to run out of gold to mine either.

Metals Focus estimates that there are 54,770t of gold reserves by the end of 2025, i.e. the portion of an ore deposit that can be economically extracted under conditions as of 2025, whereas the US Geological Survey (USGS) data estimates gold reserves to be around 64,000t.

And resources – the total potential of gold deposits based on geological evidence and sampling, including the part that is economically minable and the part that is not – are estimated to be 132,110t, based on data from Metals Focus.

There is a common misconception that proven gold reserves can only last ~15 years at the 2025 rate of production. But it is important to note that estimates of below-ground reserves have remained stable for decades even as gold is being continually mined out.

This stability is explained by several factors, which will likely continue:

- Lower-grade deposits once unprofitable become economically viable – in other words, they move from resources to reserves as the gold price increases

- More gold is discovered, albeit at a slower pace. When a gold deposit is discovered, sufficient reserves are drilled out to justify the project construction.2 But as some of the deposit depletes, further exploration often takes place, keeping total resources relatively stable.

- Often when a mine is built and brought into production, exploration geologists start to look for near-to-mine resources (often small deposits, sometimes known as satellite deposits), that can supplement reserves.

Also, with technology advancing, better geological modelling and deeper underground mining becoming more effective, making new discoveries more viable and extending current usable supply. Theorectically, gold exists deep under earth’s crust3 and even under oceans,4 although these are not currently viable due to technological constraints or cost considerations and, in some case, due to ESG concerns.5

In conclusion, while there is a slim possibility that we run out of “easy” and “cheap” gold to mine – if all discoveries stopped, technological advancement and a price that is high enough could see gold extracted from previously unfeasible supply sources.

How would sizeable changes in mined gold production impact the gold price?

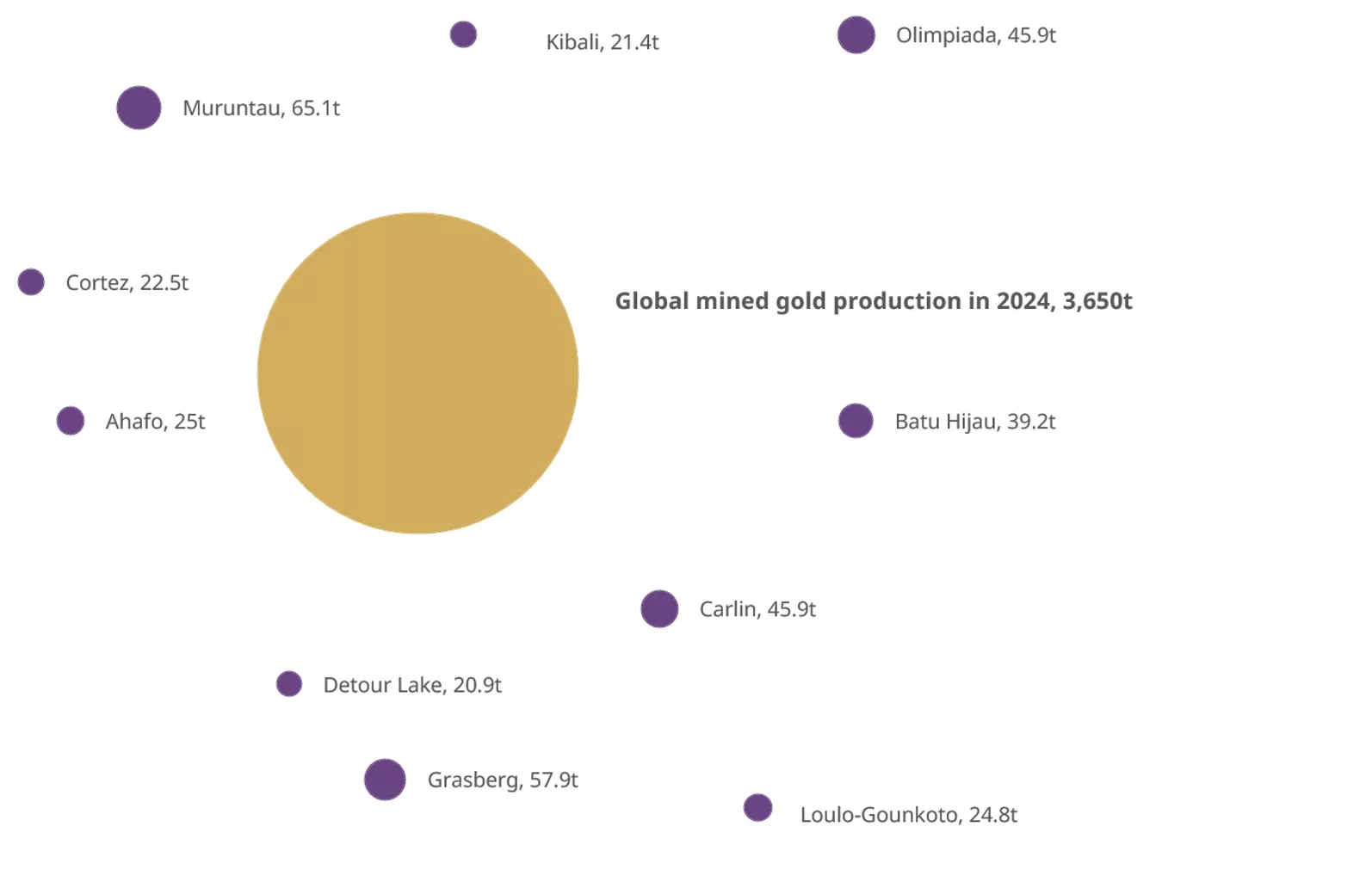

Changes to gold production are normally only reflected in changes to the price over the long term; any immediate impact will likely be mild. First, any new discovery is unlikely to be large enough to move the needle. Based on data from Metals Focus, the Muruntau mine in Uzbekistan was the largest in the world in 2024, producing 65t of gold during that year. But compared to the world total of 3,650t, it is small (Figure 2). Second, as we previously noted, any new discovery is likely to take more than a decade to be explored, permitted, built and ramped up to full production. The market will have had time to absorb the news and may gradually price in such expectations, making little impact in the short term.

Figure 2: The largest gold mine production is negligible when compared to the global total mined

Top 10 individual gold mines vs the global mined production in 2024

Source: Metals Focus, World Gold Council

From a modelling perspective, holding all else constant, QaurumSM suggests that every ~25t gold supply increase/decrease leads to a c.1% decline/rise in the gold price during the same period. But both our model and the real world function in a more complicated way. For instance, any decline in the gold price caused by a rise in mine production may lift demand for gold jewellery and industrial use, offseting the negative price impact. Furthermore, recycled gold supply may also taper off as the gold price declines, counteracting the increase in mine production. Lastly, changes that feed through each segment may not happen during the same period, further complicating the impact. It is important to note that it is the overall supply and demand conditions that collectively impact the gold price.

Is it possible for gold producers to collectively impact mined gold supply?

The answer is “probably not possible in the real world”.

First, gold supply comes from various sources, including mine production and recycling. If we assume that gold miners collectively limit production to drive up the price, recycled gold supply is likely to rise in response to the higher gold price as it often does, potentially inserting pressure on the price. With above-ground gold holdings at 219,891t, the potential for recycled gold supply is vast – although not all of it can be mobilised quickly – compared to mined gold supply.

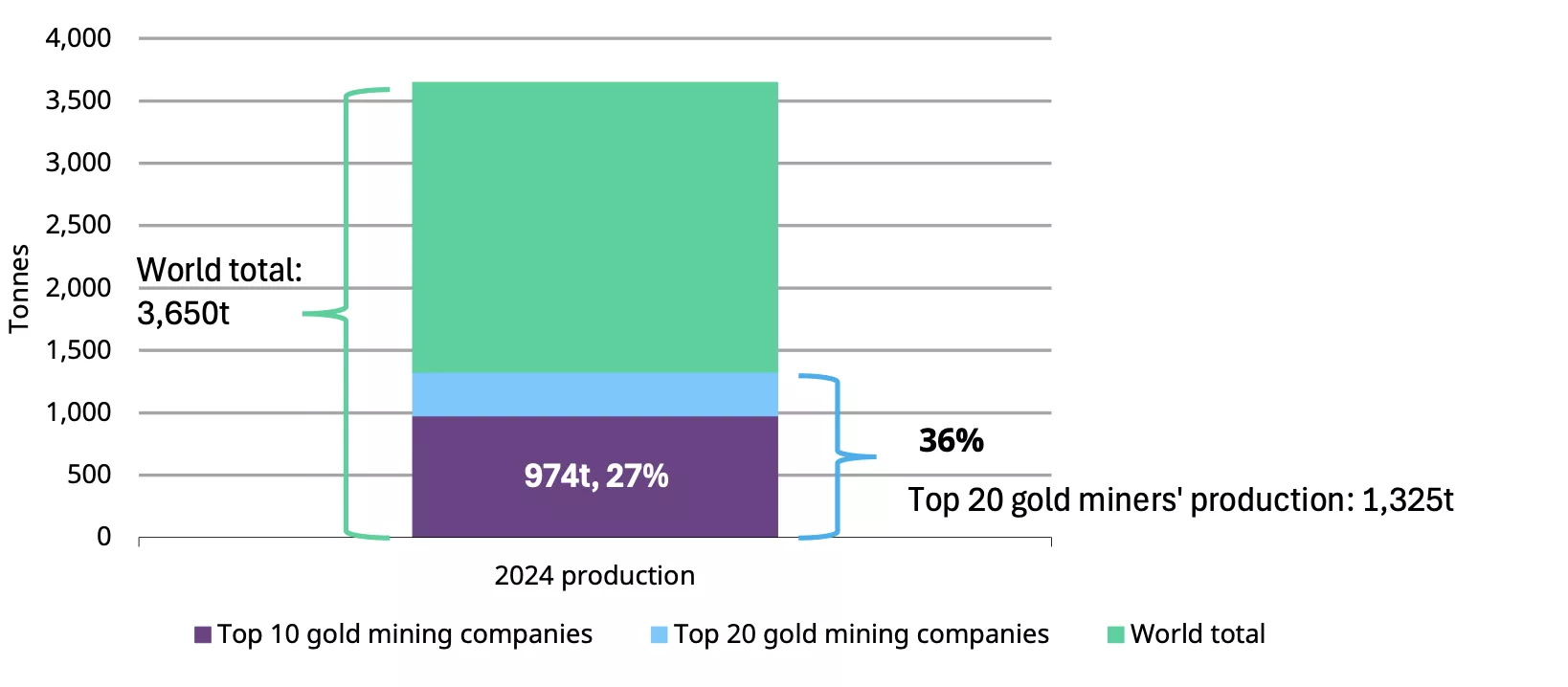

Second, the gold mining industry is globally diverse and its concentration ratio is low. The top ten gold producers accounted for 27% of total global production. It would be difficult to persuade all gold miners to act collectively, not to mention ASGM supply, which accounted for around 20% of the global total in 2024, based on our estimate6; these ASGM sources are even less likely to be responsive to attempts to constrain production. Lastly, monopolistic actions, such as co-ordinating production cuts across the gold industry, are illegal in many jurisdictions.7

Chart 2: The gold mining industry is not particularly concentrated

Top 10 and top 20 mining companies’ gold production share in the global total*

*Data as of 2024 due to data availability.

Source: Metals Focus, World Gold Council

Summary

Despite higher gold prices, mined gold production has grown only modestly, raising questions about long‑term sustainability. While the risk that we run out of “easy” reserve appears limited, technological advances and a gold price that is high enough should help unlock currently uneconomic supply. And sizeable above‑ground stocks – though not all readily accessible – can supplement mine output when conditions allow, supporting overall supply stability.

Even when large projects come online, their near‑term price impact is likely limited. Our model suggests a 25t change in supply translates into roughly a 1% price move, all else equal, but real‑world dynamics are far more complex. Lastly, fragmented production, artisanal mining, and recycled supply make coordinated supply responses unlikely, reinforcing gold’s long‑term market stability.

Footnotes

1We published our FY 2025 and Q4 data ahead of most companies’ quarterly reports, so the final numbers will differ from our estimates. Revisions to our mine supply dataset are usually concentrated in recent quarters, but revised mine production data released by the government of Indonesia saw a 7t and 5t increase in estimates for mine production as far back as 2015 and 2018, respectively.

2More exploration would incur up-front costs, and mines with reserve lives of more than about 20 years are not rewarded by the equity market.

3See: Mantle oxidation by sulfur drives the formation of giant gold deposits in subduction zones | PNAS, 19 December 2024.

4See: Gold in seawater - ScienceDirect, May 1990.

5See: Environmental, Social and Governance (ESG)

6See: Understanding ASGM: A Vital Segment of the Gold Sector | World Gold Council, 27 June 2025.

7See: The Antitrust Laws | Federal Trade Commission; International Competition Law: A Global Perspective for Multinational Corporations - Michael Edwards | Commercial Corporate Solicitor

Disclaimer

Important information and disclaimers

© 2026 World Gold Council. All rights reserved. World Gold Council and the Circle device are trademarks of the World Gold Council or its affiliates.

All references to LBMA Gold Price are used with the permission of ICE Benchmark Administration Limited and have been provided for informational purposes only. ICE Benchmark Administration Limited accepts no liability or responsibility for the accuracy of the prices or the underlying product to which the prices may be referenced. Other content is the intellectual property of the respective third party and all rights are reserved to them.

Reproduction or redistribution of any of this information is expressly prohibited without the prior written consent of World Gold Council or the appropriate copyright owners, except as specifically provided below. Information and statistics are copyright © and/or other intellectual property of the World Gold Council or its affiliates or third-party providers identified herein. All rights of the respective owners are reserved.

The use of the statistics in this information is permitted for the purposes of review and commentary (including media commentary) in line with fair industry practice, subject to the following two pre-conditions: (i) only limited extracts of data or analysis be used; and (ii) any and all use of these statistics is accompanied by a citation to World Gold Council and, where appropriate, to Metals Focus or other identified copyright owners as their source. World Gold Council is affiliated with Metals Focus.

The World Gold Council and its affiliates do not guarantee the accuracy or completeness of any information nor accept responsibility for any losses or damages arising directly or indirectly from the use of this information.

This information is for educational purposes only and by receiving this information, you agree with its intended purpose. Nothing contained herein is intended to constitute a recommendation, investment advice, or offer for the purchase or sale of gold, any gold-related products or services or any other products, services, securities or financial instruments (collectively, “Services”). This information does not take into account any investment objectives, financial situation or particular needs of any particular person.

Diversification does not guarantee any investment returns and does not eliminate the risk of loss. Past performance is not necessarily indicative of future results. The resulting performance of any investment outcomes that can be generated through allocation to gold are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. The World Gold Council and its affiliates do not guarantee or warranty any calculations and models used in any hypothetical portfolios or any outcomes resulting from any such use. Investors should discuss their individual circumstances with their appropriate investment professionals before making any decision regarding any Services or investments.

This information may contain forward-looking statements, such as statements which use the words “believes”, “expects”, “may”, or “suggests”, or similar terminology, which are based on current expectations and are subject to change. Forward-looking statements involve a number of risks and uncertainties. There can be no assurance that any forward-looking statements will be achieved. World Gold Council and its affiliates assume no responsibility for updating any forward-looking statements.

Information regarding QaurumSM and the Gold Valuation Framework

Note that the resulting performance of various investment outcomes that can be generated through use of Qaurum, the Gold Valuation Framework and other information are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. Neither World Gold Council (including its affiliates) nor Oxford Economics provides any warranty or guarantee regarding the functionality of the tool, including without limitation any projections, estimates or calculations.