Strong Q4 lifts full year demand 10%

Annual demand recovered across virtually all sectors – the notable exception being ETFs, which saw net annual outflows

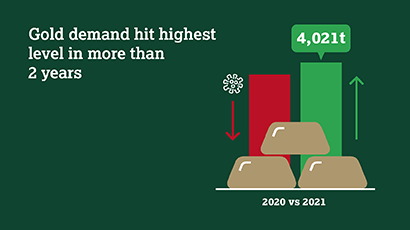

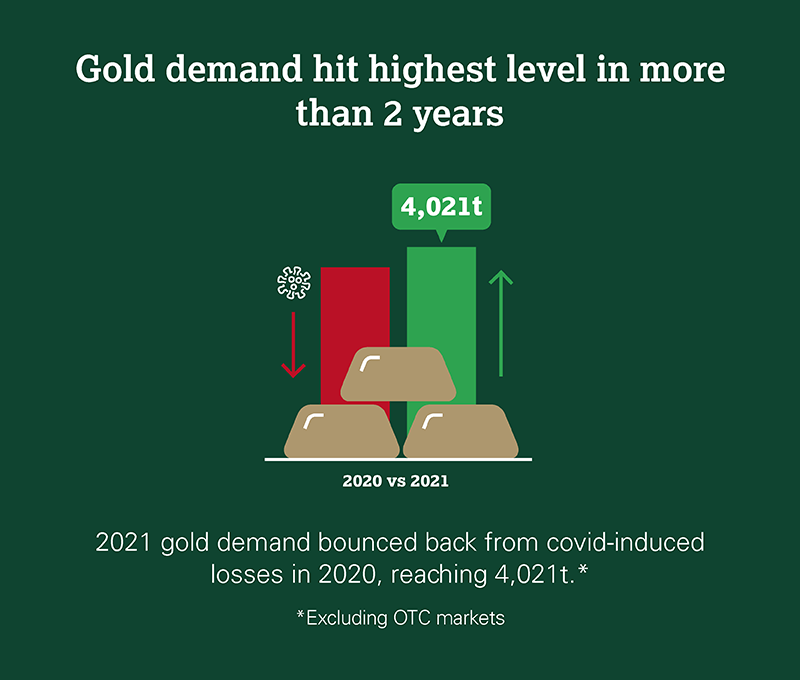

Full year 2021 gold demand (excluding OTC) increased to 4,021t, propelled by Q4 demand which jumped almost 50% to a 10-quarter high.1 Demand recouped much of the COVID-related losses sustained during 2020. Demand for gold in the consumer-driven jewellery and technology sectors recovered throughout the year in line with economic growth and sentiment, while central bank buying also far outpaced that of 2020. Investment demand was mixed in an environment of opposing forces: high inflation competed with rising yields for investors’ attention.

Jewellery fabrication staged a strong recovery in 2021. It grew 67% to 2,221t to meet the strong rebound in jewellery consumer demand, which increased 52% in 2021 to 2,124t, matching the 2019 total. This was in good part linked to Q4 demand, which – at 713t – saw the strongest quarterly jewellery consumption since Q2 2013.

Global holdings of gold ETFs fell by 173t in 2021 in sharp contrast to 2020’s record 874t increase. Q4 outflows of just 18t were a fraction of the much larger outflows seen in Q4 2020.

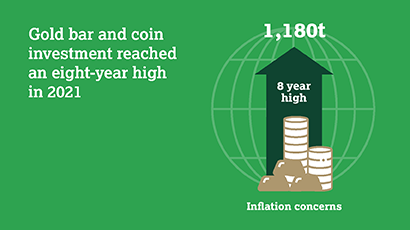

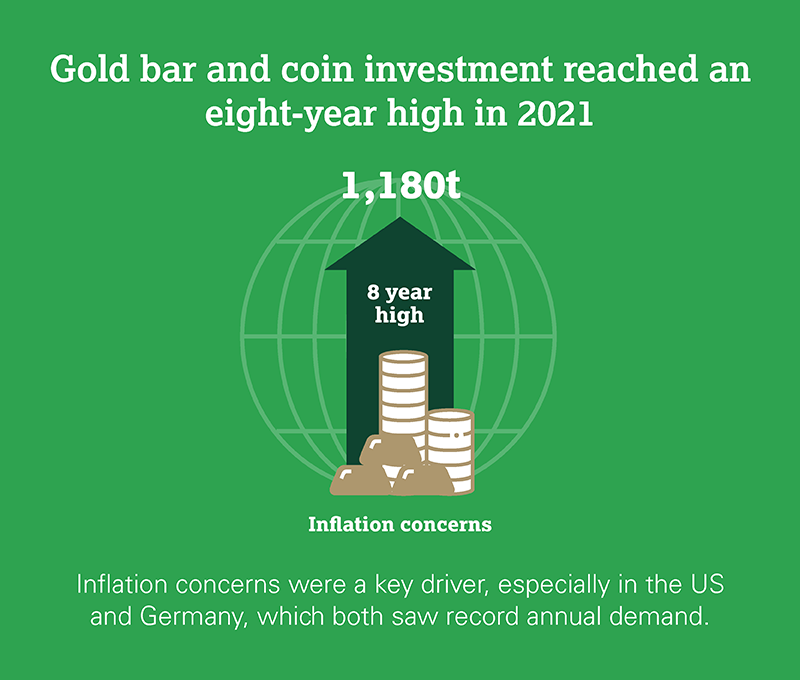

Bar and coin investment maintained its momentum, jumping 31% to an eight-year high of 1,180t. Q4 2021 demand of 318t, meanwhile, was the highest for a fourth quarter since 2016.

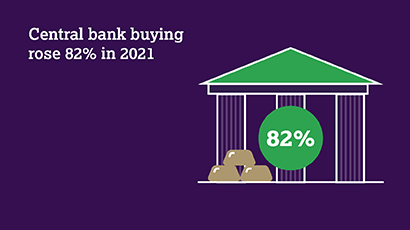

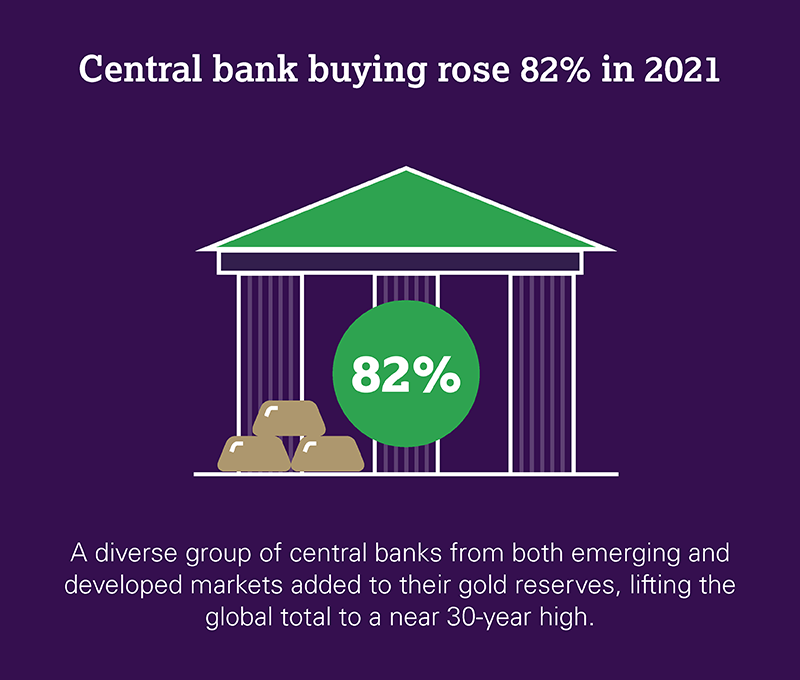

Central banks accumulated 463t of gold in 2021, 82% higher than the 2020 total and lifting global reserves to a near 30-year high. The pace of buying slowed in the second half, with a 22% y-o-y decline in Q4.

Gold used in technology grew 9% in 2021, to reach a three-year high of 330t. Y-o-y growth slowed in the most recent quarter (to 2%), highlighting the rapid recovery seen in the sector in Q4 2020.

{kind=link}

{kind=link}